Global| Feb 02 2017

Global| Feb 02 2017EMU PPI Turns Sharply Higher

Summary

The EMU area PPI surged by 1.1% in December, driving the three-month inflation rate to 10%, the six-month pace to 5.3% and raising the year-over-year pace to 1.6%. This is a sharp reversal from last year's 3% drop in the PPI. Price [...]

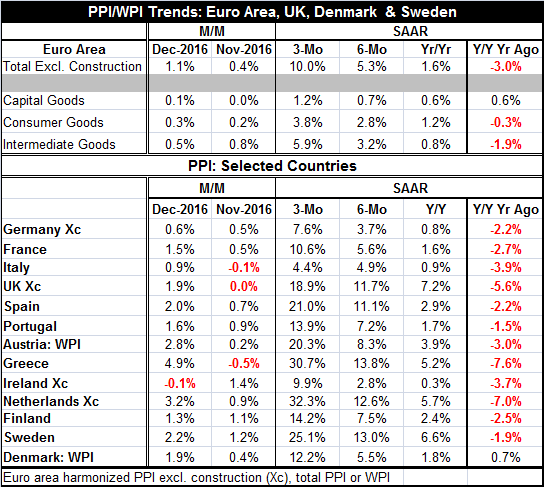

The EMU area PPI surged by 1.1% in December, driving the three-month inflation rate to 10%, the six-month pace to 5.3% and raising the year-over-year pace to 1.6%. This is a sharp reversal from last year's 3% drop in the PPI.

The EMU area PPI surged by 1.1% in December, driving the three-month inflation rate to 10%, the six-month pace to 5.3% and raising the year-over-year pace to 1.6%. This is a sharp reversal from last year's 3% drop in the PPI.

Price trends are accelerating from 12-month to six-month to three-month for all three major categories as well: capital goods, consumer goods and intermediate goods.

The table contains an assortment of 10 EMU nations and several other European nations. Only one of them, Ireland has a drop in its PPI month-to-month in December. Inflation is accelerating over six-month to three-month as well as from 12-month to six-month in each of these nations except in Italy (where the inflation rate abates from six-month to three-month).

PPI inflation is its most virulent in the Netherlands, Greece, Sweden and Spain. Each of those nations has a high ranking for inflation compared to the others over three months and six months and each of them shows strong inflation acceleration from three-month to six-month and from 12-month to six-month.

Inflation is low in Italy, Germany, France, Ireland and Denmark. Those countries show moderate inflation over three-month, six-month and 12-month compared to other members and also a low tendency for inflation to accelerate. Some countries simply have shock absorbers than keep inflation at bay, but others have a more incendiary tendency.

In the face in this inflation pressure, the ECB has released an announcement that inflation is rising on the back of rising oil prices and that does not change the outlook at all. The ECB intends to 'look through' the rise in oil prices and to keep its ultra-easy policy as long as the prices of other goods and services remains slow. The German cry for action is falling on deaf ears. This is no longer simply analysis but is admitted ECB policy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief