Global| Aug 04 2014

Global| Aug 04 2014EMU PPI Slows Its Decline; Has It Begun a Reversal?

Summary

The EMU producer price index rose by 0.2% in June as its year-over-year drop was cut to just -0.1%. The trend for the PPI is not absolutely clear from the sequential growth rates since there is a speedup drop from 12 months to six [...]

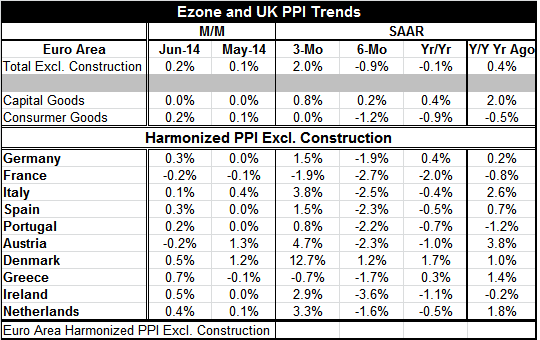

The EMU producer price index rose by 0.2% in June as its year-over-year drop was cut to just -0.1%. The trend for the PPI is not absolutely clear from the sequential growth rates since there is a speedup drop from 12 months to six months before reversing to post a gain over three months. Neither capital goods nor consumer goods show any clear pattern either.

The EMU producer price index rose by 0.2% in June as its year-over-year drop was cut to just -0.1%. The trend for the PPI is not absolutely clear from the sequential growth rates since there is a speedup drop from 12 months to six months before reversing to post a gain over three months. Neither capital goods nor consumer goods show any clear pattern either.

However, there may be good news in the chart above that shows the time-series of year-over-year percentage changes in the PPI vs. the European Central Bank's target rate, the HICP. There we see clearly that the PPI marks larger oscillations than the HICP and that the PPI cycles largely contain the HICP cycles. In that sense, the rise in PPI may be good news for the HICP. While the PPI does show some cycles that are not strictly followed by the HICP, the rise in the PPI could be foreshadowing a coming gain in the HICP. That would be good news for the HICP and for the ECB as European inflation has swung so low. The ECB has mounted a special program to spur lending to stop the HICP from decelerating further.

A grouping of 10 of the original EMU members reveals that only two show a PPI decline over three months, while all but one show declines over six months, and but two show declines over 12 months. The trends for the PPIs at the country level suggest that over three months downward pressure has abated. Even so, that is only for three months and it will take more than that to form a convincing tend, especially with European activity data so uneven.

The PPI shows only the second back-to-back monthly increases since November 2012. And the year over trends are turning up. It is thin evidence, but it is all that we have in the way of good news that the disinflation trend in Europe may be coming to an end.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief