Global| Jan 05 2017

Global| Jan 05 2017EMU PPI Shows Widespread Gains; Is It Inflation or a Dog Quacking?

Summary

PPI, CPI, 'X'PI- you name the 'X' factor- just about any kind of price indexes is on the rise these days. Oil prices now have a nice head of steam and price increases over horizons from X to Y (again, you fill in the blanks) are on [...]

PPI, CPI, 'X'PI- you name the 'X' factor- just about any kind of price indexes is on the rise these days. Oil prices now have a nice head of steam and price increases over horizons from X to Y (again, you fill in the blanks) are on the rise.

PPI, CPI, 'X'PI- you name the 'X' factor- just about any kind of price indexes is on the rise these days. Oil prices now have a nice head of steam and price increases over horizons from X to Y (again, you fill in the blanks) are on the rise.

But here is the question: Is it really inflation?

Now we can apply the duck test to it. Does it look like a duck? Does it quack like a duck? Does it walk like a duck? If it does, then It's a duck! DUCK! But what if it is an imposter?

Inflation is just a bit more difficult to categorize than a duck (although I make no claims to expertise in ornithology).

Inflation assessment

Inflation is a generalized and ongoing increase in prices. And the rub there is two-fold. If the inflation cause is mainly one item like oil, is the rise in the price level still to be construed as inflation? And if the price level is rising, how do we know that (or if) it will continue to rise? Inflation assessment requires an element of forecasting or of making it up. And that is, of course, always somewhat unsatisfactory, but it is the truth.

Two practical issues

There are two elements here that make inflation assessment difficult. One is that oil has inelastic demand in the short run. That means that consumption of oil and oil products will not shift (much) to avoid the pain of oil price increases. Price indices will show the full strength of the oil price increase passing through to inflation measures even if they have variable weights. In the short run, people will be inconvenienced by higher oil prices and might avoid making hard-choice tradeoffs by running up debt, running down savings or reducing their savings rate. But in the longer run, they will make adjustments and some of those might involve resetting their spending patterns to buy less nonoil stuff to make room for the more expensive oil-related purchases or even making investments into energy-savings like buying a high mileage car or adding insulation to a house. But imagine having a fixed budget constraint with no wiggle room: no money in the bank, no room to alter your savings rate, and oil prices rise. What do you do? If energy prices double, driving the car half way to work and walking the rest of the way will not cut it. You could car pool. You might cut back spending on other items. In that way, the rise in oil prices might put downward pressure on nonoil prices and that would buffer the overall impact of oil on the price level and on inflation. Because the transmission of that mitigating effect might take time, the initial impact of an oil shock on the price level might overstate the eventual inflation pass-through. As we have seen in the past, oil price changes can also be deflationary by spreading negative feedback to other sectors, as in these examples. This is an important reason why a rising oil price is not necessarily as inflationary as it looks. Rising oil prices mark a change in the relative price of oil and do send an inflation impulse, but it's one that the economy might wrestle with and dissipate. The second thing that makes the inflationary assessment of oil price difficult is that this impact on 'inflation' occurs only as long as oil prices are rising. If oil rises from $40/barrel to $50/barrel, there would be a one-time shock to the prices LEVEL and that would LOOK LIKE inflation (a duck) for a while, but eventually the impact on the price level and on inflation would fade and disappear (the duck would stop quacking). Of course, even that is complicated because oil does not simply move once and settle. We are continually trying to evaluate where the oil price-level is and if will stay or if it has any directional drift. The real world is terribly complex place. Even simple ideas have a complicated framework.

Oil's impact in EMU

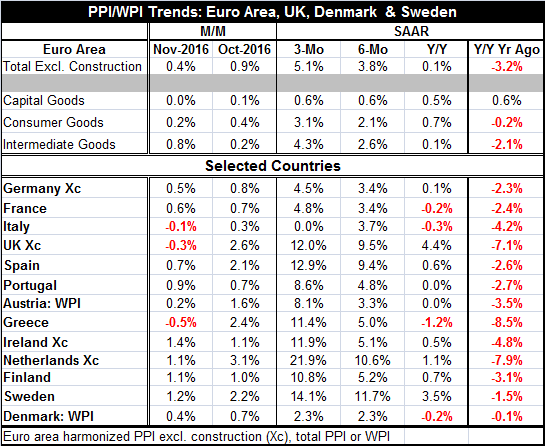

Oil prices have their largest impact on producer prices where there is no service sector present in the index. In the PPI table below, we see consumer goods prices moving up at the producer price level from a 0.7% pace over 12 month to a 3.1% (annualized) pace over three months. Consumers are paying more for their energy needs. And intermediate goods where oil appears more directly shows inflation is up from a 0.1% pace over 12 months to a 4.3% pace over three months. But for capital goods where the energy effect is miniscule, inflation has only ticked up from 0.5% over 12 months to a pace of 0.6% over three months.

The illusion of inflation

While on one hand we seem to see inflation everywhere, what we are seeing is the illusion, confusion, or a minor contusion being caused by rising energy goods prices and their impact on the price level that is then magnified by the miracle of compounding spread over various time horizons. For all these reason, I caution on the conclusion that inflation is here or is even a threat. Energy is not in short supply even under the new artificial OPEC scheme. Globally the second part of that assessment is that we do not even know if the OPEC price changes will stick. What if oil prices back down after rising because OPEC members cheat on their quotas as they always have in the past?

Barking up the wrong tree

In short, what we may have is an OPEC ventriloquist effectively making a dog's bark sound like a duck's quack. In this case, what might look like or sound like a 'duck' maybe nothing of the kind. And if oil prices unwind, we may find that the volatility in oil price actually weaken economic activity because of the impact of uncertainty.

Diamonds are forever-not oil prices

It is also true that the change in oil prices can seem 'lasting' even while it is only temporary. The question is how long need an oil-price rise (or fall) last to affect behavior? Well, that is a 'how many angels can stand on the head of a pin' sort of question, isn't it? The 1973-74 oil price shock spawned other sets of increases and while they ultimately were their own demise, the end result even after oil prices collapsed in the 1980s was that oil prices were higher than they had been in the early 1970s. The Saudis have oil for the long run and it is in their interest to keep oil prices from becoming too high so that alternative sources cannot be so easily tapped. But ahead of the financial crisis, the Saudis took their eye off that ball and as it flew by them oil prices spurted toward $150/barrel. New sources were developed helter-skelter and eventually technology has made those processes even more cost effective and now they are a problem for OPEC. Around the $50/barrel mark, a lot of new-production-method oil is viable again. That should provide a more or less natural market-generated cap on oil prices for a while.

Beware the quacking dog

So the impact of oil on inflation is much more complicated than asking what is the price of spot oil today? Even the trend for prices can be misleading. In the oil patch dogs can quack but only for a while. So now you know why the saying is that the 'cure' for high oil prices is high oil prices, and the solution for low oil prices is low oil prices. The dynamics of a free market will restore some sort of equilibrium. OPEC is using 'the cartel and friends' to try to speed up and to control the process. History tells us that that is not usually very successful, but it still can be very disruptive. And these are disruptive times if nothing else.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief