Global| Dec 03 2013

Global| Dec 03 2013EMU PPI Is Still Losing Steam- and Faster

Summary

PPI prices in EMU continue to be weak. Prices fell in October and they are lower year over year. The table, featuring 10 EMU members plus the UK, shows producer prices lower across the board in October except for Ireland where prices [...]

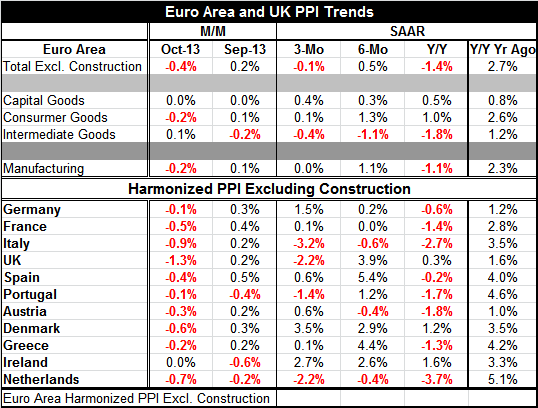

PPI prices in EMU continue to be weak. Prices fell in October and they are lower year over year. The table, featuring 10 EMU members plus the UK, shows producer prices lower across the board in October except for Ireland where prices are flat in October.

PPI prices in EMU continue to be weak. Prices fell in October and they are lower year over year. The table, featuring 10 EMU members plus the UK, shows producer prices lower across the board in October except for Ireland where prices are flat in October.

Year over year, only three of the countries fail to have dropping producer prices. Over six months only three have falling prices. Over three months four have dropping producer prices and overall PPI prices in the euro zone also are falling.

Intermediate goods prices lead the weakness. But capital goods prices are up by only 0.5% year over year. Yet consumer price inflation is falling faster than prices for capital goods. Intermediate goods price inflation is falling by 3 percentage points faster over the last 12-months than over the previous 12-months. For consumer goods, the deceleration is 1.7 percentage points over the last year. For capital goods, it is 0.3 percentage points.

It is not just that the inflation rate is negative overall, but that it is lower than it was a year ago across all three main PPI categories. Clearly, the strong negative impulse is coming from intermediate goods where raw materials like oil have an outsized impact. But the other two sectors, while still showing year over year price gains, are showing smaller gains and that marks the spread of disinflationary forces. This kind of price weakness is an indicator of still very weak demand. With intermediate prices falling, there is actually more room for other prices to rise under a steady monetary policy. Yet that is not happening. Other prices are slowing their pace as well.

While the manufacturing indicators show some pick-up, the PPI is a reminder that conditions are still very weak in Europe. There may be some pick-up in activity, but it is not enough to put any firmness into prices. For now the weak PPI is the dog that didn't bark. It is continuing evidence that the economy lacks something to vault itself into a sustainable gear.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief