Global| Jul 02 2019

Global| Jul 02 2019EMU PPI Eases-What's Next?

Summary

The EMU PPI fell by 0.2% in May, dropping for the second month in a row. The year-over-year rate dropped sharply to 1.7% from 2.6% largely because May of one year ago had seen the PPI rise by 0.7% month-to-month. Comparisons are going [...]

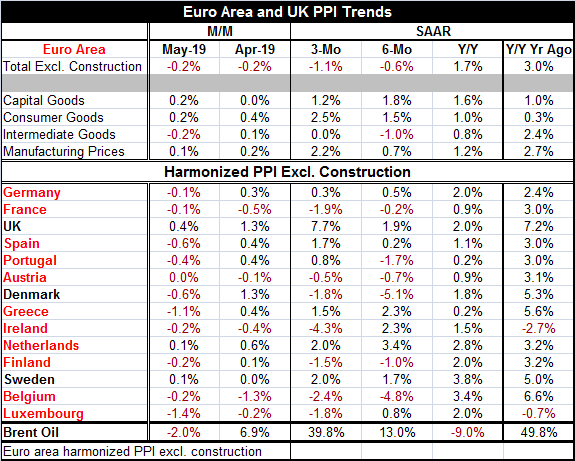

The EMU PPI fell by 0.2% in May, dropping for the second month in a row. The year-over-year rate dropped sharply to 1.7% from 2.6% largely because May of one year ago had seen the PPI rise by 0.7% month-to-month. Comparisons are going to be easy for the next five months as well as there is one 0.3% gain over that span, three 0.5% gains, and then one 0.6% gain in the year-ago period. In other words, if the next six months bring in increase less than that sequence, the year-on-year pace for the PPI will fall. That seems to be an excellent bet at the moment. A year ago oil prices had been rising into that May-August period. Oil peaked in August at over $80/barrel for Brent. Oil had been as cheap as $51.85/barrel in August 2017. That put a substantial inflation impulse in train for last year. In contrast, oil prices seem to be easing now after a period of firming. If oil prices do deflate, the PPI could ease considerably in the months ahead.

The EMU PPI fell by 0.2% in May, dropping for the second month in a row. The year-over-year rate dropped sharply to 1.7% from 2.6% largely because May of one year ago had seen the PPI rise by 0.7% month-to-month. Comparisons are going to be easy for the next five months as well as there is one 0.3% gain over that span, three 0.5% gains, and then one 0.6% gain in the year-ago period. In other words, if the next six months bring in increase less than that sequence, the year-on-year pace for the PPI will fall. That seems to be an excellent bet at the moment. A year ago oil prices had been rising into that May-August period. Oil peaked in August at over $80/barrel for Brent. Oil had been as cheap as $51.85/barrel in August 2017. That put a substantial inflation impulse in train for last year. In contrast, oil prices seem to be easing now after a period of firming. If oil prices do deflate, the PPI could ease considerably in the months ahead.

Current trends

Current PPI trends show the headline pace of inflation at 1.7% over 12 months, falling to a -0.6% pace over six months and to a -1.1% pace over three months. However, manufacturing prices show a tendency to acceleration with prices at a 1.2% gain over 12 months, a 0.7% pace over six months, and a rise to a 2.2% pace over three months. The legacy comparison of manufactures prices is not as strong as for the PPI-excluding construction headline, but there is a large PPI gain in May 2018 and another in June 2018 that the PPI will match up against next month. Having a high PPI gain month-to-month in the year-ago period tends to depress the year-on-year inflation measure in the current period, especially when data are seasonally adjusted as these are,

The breadth of price trends

Price weakness is prevalent across the EMU and in Europe with the PPI rising in May in only two of the 14 countries in the table. That compares to only five declines posted in April. Seven of fourteen show declines over three months. Six show declines over six months and none show declines over 12 months. But over 12 months, 12 of 14 countries show lower inflation than for the comparable 12-month period of 12-months ago.

Oil

Oil prices have been tending to push the PPI higher. Even though they fall by 9% over 12 months, they gain at a 13% pace over six months and at a nearly 40% pace over three months. However, oil has fallen month-to-month in May. And despite geopolitical tensions in the Middle East and around the oil shipment lanes, oil prices are softening although OPEC is making plans to try to support oil prices.

On balance, inflation in the EMU appears to be extremely well contained. Nothing seems to speak of an inflation risk on the horizon unless the oil market is turned upside down overnight. And something like that remains a possibility. But inflation tends far and wide to remain favorable, which is to say that inflation will likely continue to fall short of the ECB's objectives. These, of course, are set for consumer prices and the HICP format.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief