Global| Aug 04 2015

Global| Aug 04 2015EMU PPI Drops But It Also Decelerates

Summary

The PPI headline in June fell by 0.2%, its first month-to-month decline since January. The headline rate shows a pattern of deceleration in its drop from12-month to six-month to three-month. But none of the components show clear [...]

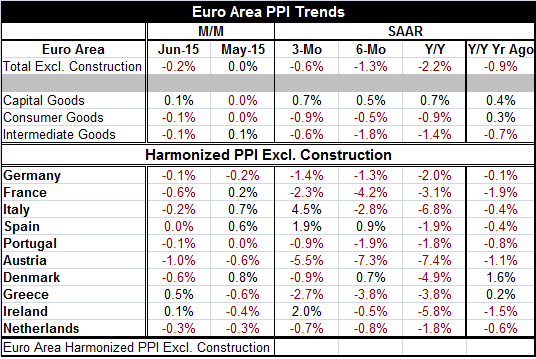

The PPI headline in June fell by 0.2%, its first month-to-month decline since January. The headline rate shows a pattern of deceleration in its drop from12-month to six-month to three-month. But none of the components show clear decelerations. Among the 10 member countries whose PPIs we list in the table, six show a pattern of either decelerating declines or accelerating increases. Despite the proliferation of negative numbers for the PPI, the trend seems headed higher.

The PPI headline in June fell by 0.2%, its first month-to-month decline since January. The headline rate shows a pattern of deceleration in its drop from12-month to six-month to three-month. But none of the components show clear decelerations. Among the 10 member countries whose PPIs we list in the table, six show a pattern of either decelerating declines or accelerating increases. Despite the proliferation of negative numbers for the PPI, the trend seems headed higher.

Italy, Spain and Ireland each have three-month changes that have turned positive. Italy shows the strongest turnaround in inflation with Ireland in second place.

While the ECB sets its inflation objective (of slightly less than 2%) in terms of the HICP rate, the chart at the top shows a clear relationship between the PPI and the CPI. They basically run the same cycles with the PPI changes coming a bit sooner and with higher peaks and lower troughs. The PPI is a good double check at least on the performance of the HICP. Right now the PPI is saying that the HICP is set to start heading higher.

Even so, the current HICP pace is extremely low and well off the ECB's price objective. The turn apparent in the pattern of the PPI is still rather mild and not a cause of concern- if anything perhaps it's something to cause a sense of relief. But as yet inflation remains low and price declines are rampant throughout euro area members. The sense of that changing is still incipient. And with world energy prices still in an unstable mode, we would judge this move to lesser price decreases or leading to a period of price increases as not simply incipient but as not yet firmly established as a trend. Ireland and Italy may be making strong strides toward inflation, but a great deal of price weakness lingers elsewhere.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief