Global| Oct 02 2015

Global| Oct 02 2015EMU PPI Collapses as HICP Turns to Show Deflation

Summary

The ECB's targeted HICP already has dipped below zero in its year-over-year change. In August the PPI shows another sharp drop in headline PPI prices. Are the forces of deflation gathering steam? The August PPI in the EMU fell by 0.9% [...]

The ECB's targeted HICP already has dipped below zero in its year-over-year change. In August the PPI shows another sharp drop in headline PPI prices. Are the forces of deflation gathering steam?

The ECB's targeted HICP already has dipped below zero in its year-over-year change. In August the PPI shows another sharp drop in headline PPI prices. Are the forces of deflation gathering steam?

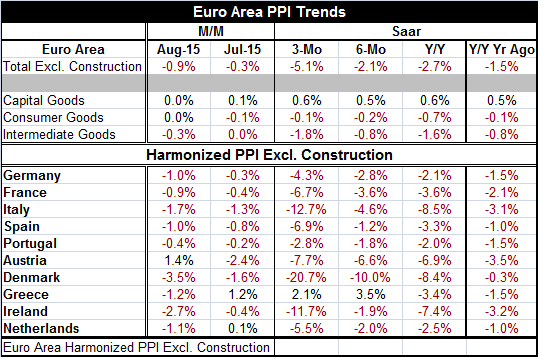

The August PPI in the EMU fell by 0.9% after falling by 0.3% in July. The PPI (ex-construction) is falling faster over three months (-5.1% annualized pace) than it is over 12 months (-2.1%). Price weakness is spreading again.

Looking at PPI sectors, prices are flat for capital goods and consumer goods in August but intermediate goods prices are falling by 0.3%. Capital goods prices, in fact, are rising and show steady inflation in the 0.5% to 0.6% range from 12 months to six months to three months. But for consumer goods and intermediate goods prices, we see weakness. Consumer goods prices are declining on all horizons, but the pace of decline is actually slowing. For intermediate goods deflation has stepped up a bit with prices falling 1.6% over 12 months and now falling at a 1.8% pace over three months. Moreover, overall PPI prices are now lower for the last two years -and three years- running.

Looking at a group of early EMU members, we find that negative inflation rates across all horizons predominate. And prices are falling more rapidly over six months than over 12 months in Germany, France, Italy, Spain, Portugal Austria, Denmark, Ireland and the Netherlands. Oddly, Greece is the exceptions, showing positive inflation over three months and six months.

The surprise weakness in U.S. employment growth reported today has shocked markets. Meanwhile, inflation worldwide remains low and is moving lower. Europe is experiencing deflation in its HICP. Japan's core CPI is falling year-over-year. Japanese firms have cut their expectations for inflation. Oil prices have been oscillating in a narrow band recent weeks, but oil is still in vast excess supply. Oil's price stability is on thin ground. While today Mario Draghi tried to argue that the ground work has been laid for growth to build upon, but the news of weaker employment growth in the U.S. begs the question of whether the U.S., the last zone of economic stability in the global economy, has been made to bear too much weight for the rest of the world and whether it can sustain enough growth. Globally, forecasts continue to be cut. In the U.S., Federal Reserve officials seem unable to come to grips with what the economy is doing frustrating their attempts to get out in front of events.

There is nothing encouraging from the recent weakness in prices. The day's weak U.S. employment weakness has undermined the dollar's rise and has put some uptrend into precious metals that are priced in dollar terms. But there is nothing there that suggests that the new bout of deflation, or risk of it spreading, is being diminished.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief