Global| Aug 21 2014

Global| Aug 21 2014EMU PMIs Wither Again in August- It Isn't the Heat

Summary

The flash PMI for the European Monetary Union in August slipped once again to 52.8 from 54.0 in July. The index is back to where was in June. The manufacturing index, which had been stable at 51.9 in June and July, has dropped to 50.8 [...]

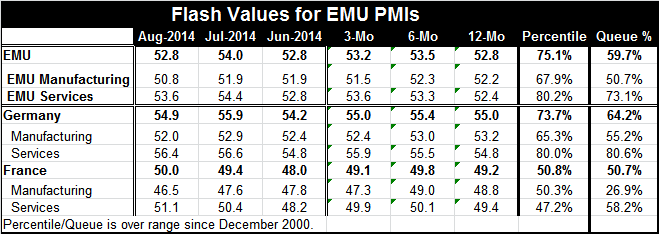

The flash PMI for the European Monetary Union in August slipped once again to 52.8 from 54.0 in July. The index is back to where was in June. The manufacturing index, which had been stable at 51.9 in June and July, has dropped to 50.8 in August. The services sector metric dropped to 53.6 in August from 54.4 but is still above its June value of 52.8. The manufacturing PMI appears to be in a state of steady slippage, while the services PMI appears to be somewhat erratically moving higher despite the setback this month. But the services/manufacturing divergence is marked (see Chart). It's the largest manufacturing index-services index gap since 2009.

The flash PMI for the European Monetary Union in August slipped once again to 52.8 from 54.0 in July. The index is back to where was in June. The manufacturing index, which had been stable at 51.9 in June and July, has dropped to 50.8 in August. The services sector metric dropped to 53.6 in August from 54.4 but is still above its June value of 52.8. The manufacturing PMI appears to be in a state of steady slippage, while the services PMI appears to be somewhat erratically moving higher despite the setback this month. But the services/manufacturing divergence is marked (see Chart). It's the largest manufacturing index-services index gap since 2009.

The flash PMI data provide country detail for Germany and for France only. Germany saw a setback in its overall PMI in August to 54.9 from 55.9 in July; at 54.9. Germany is still ahead in August of its value in June. For France, the overall PMI edged higher to 50.0 in August from 49.4 in July. The French index is at or above 50 for the first time since April 2014.

The details for Germany show its manufacturing sector that moved up in July to 52.9 from 52.4 in June. But it slid back to 52.0 in August and is below its June reading. German services are steadier; they rose to 56.6 in July from 54.8 in June and now have slipped to 56.4, a level that still above its June value.

France's manufacturing slipped in July to 47.6 from 47.8 and it slipped again in August, this time more sharply to 46.5. The services sector is improving; it rose to 50.4 in July from 48.2 in June and rose again to 51.1 in August. The service sector has been strong enough to compensate for weakness in manufacturing and has dragged the overall French PMI to a neutral 50.0 reading this month.

In terms of the absolute standing of these metrics, for the EMU total private sector gauge stands in the 59.7 percentile of its historic queue; that means it's higher a little bit more than 40% of the time. The German reading is in the 64.2 percentile, meaning it's higher about 36% of the time. The French reading is in the 50.7 percentile, meaning that it's just about its midpoint and it's higher about half the time; it's lower about half the time. This is supposed to be an advanced stage of a business cycle recovery. That's a very weak reading for France at this point in the cycle.

Turning to component readings, the EMU manufacturing sector has a standing in the 50.7 percentile of its historic queue. Germany's manufacturing is in the 55.2 percentile while France's manufacturing is extremely weak, in the 26.9 percentile, just barely above its lower quartile.

The component reading for services in the EMU is at a 73.1 percentile standing and is even stronger at an 80.6 percentile standing for services in Germany. France is at a 58.2 standing which is certainly a lot better than its manufacturing standing but it's way below what we are seeing in Germany and even in the EMU as a whole.

The EMU continues to show us this waffling behavior. We know that there was weakness before the situation in Ukraine began to deteriorate. But since then, we are seeing knock-on effects that are adversely affecting growth in the monetary union. Russia, that has been the target of sanctions, has started to become more aggressive. It immediately struck at some fruit and vegetable exports to it out of Europe, but has now shifted its gaze to the branches of US multinational corporations operating in Russia. It has been closing down McDonald's restaurants. I don't really suppose that the closure of four restaurants in the McDonald's universe is going to affect McDonald's stock very much nor do I think it's going to create much backlash in the United States. But Russia appears to be desperate to do something to strike back and we should be brace that it might find something that actually is harmful.

The Fed's Jackson Hole conference is set to start and we are interested in this event since not only is Fed Chair Janet Yellen going to give the keynote speech, but we will have a presentation from European Central Bank President Mario Draghi who may tell us a bit more about strategies for recovery in the EMU. The ECB has mounted a program to stimulate lending in the region. We will be watching to see if in the wake of Russian sanctions it is willing to do anymore.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief