Global| Jul 24 2013

Global| Jul 24 2013EMU PMIs Turn Up- But Not Yet the Right Stuff?

Summary

Today is a red-letter day of some sort. China reported out a weakening in its manufacturing sector survey at the same time that Europe reported out improved economic numbers…and markets chose to react positively to the numbers [...]

Today is a red-letter day of some sort. China reported out a weakening in its manufacturing sector survey at the same time that Europe reported out improved economic numbers…and markets chose to react positively to the numbers released in Europe. It's clearly a good sign about market psychology. Can it be that attention is shifting away from China? Or is it that the China news that some stimulus is planned after all causing markets to discount numbers that have basically been created under a policy regime that is no longer in effect? Are either of these bona fide reasons to rejoice?

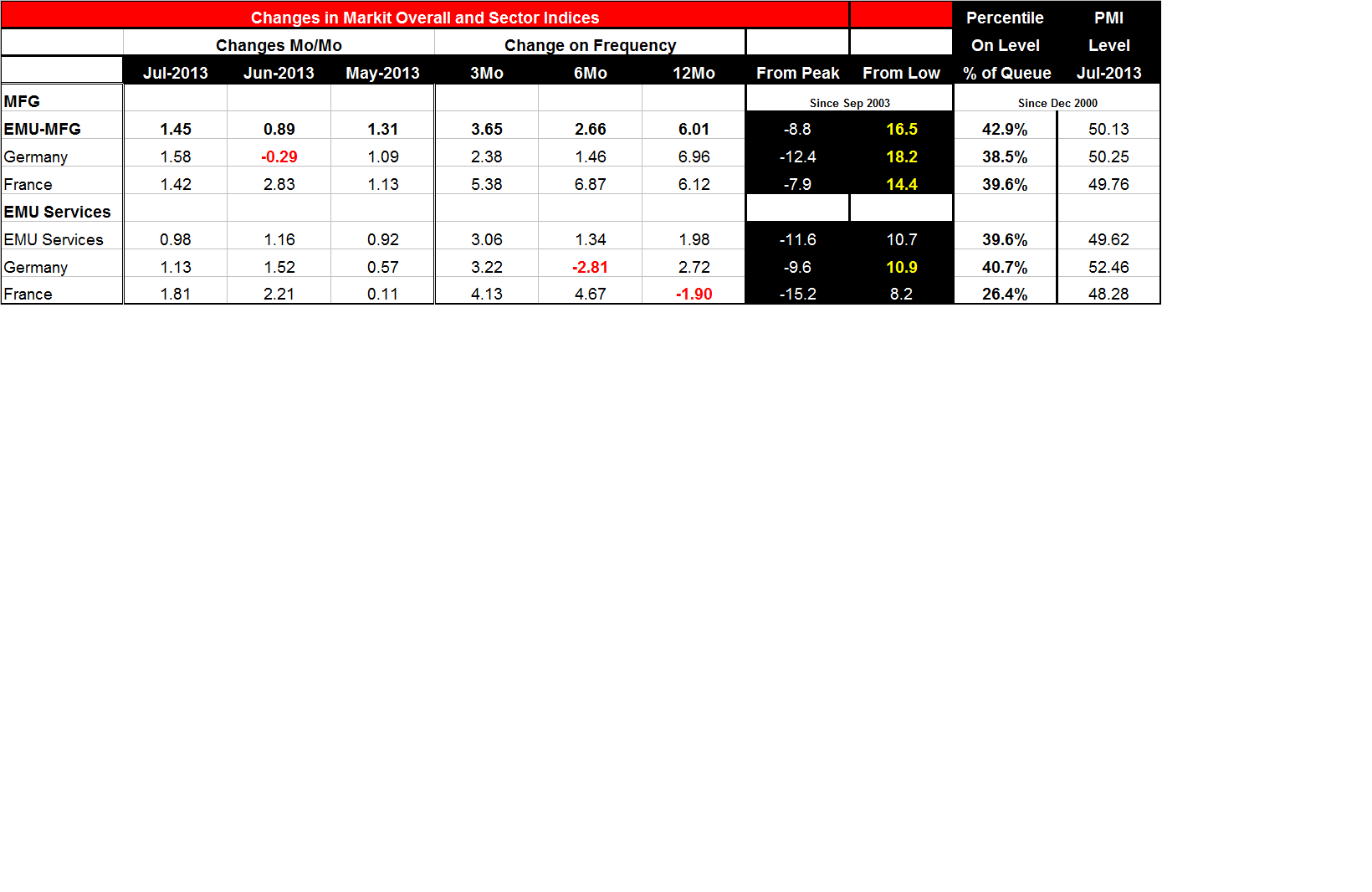

The manufacturing index for EMU jumped from 48.82 in June to 50.13 in July a top 11 percentile monthly jump. The services sector index continues to show contraction at 49.62 in July but the sector improved its metric sharply from 48.26 in June- a monthly rise that is exceeded only 23% of the time. As a result of these two upward shifts, the composite index for the European Monetary Union has crossed the threshold to show a positive reading of 50.13 in July up from 48.89 in June, ending the string of 17 straight months during which the composite index lingered below 50- alas it is only just barely in expansion territory by 0.13 points. But it's something.

On the face of it the news is good; it's not clear that the news is great, however.

Looking at the details for Germany and France we can see that the manufacturing sectors for each of these countries have progressed much more from their respective recent cycle lows that they have fallen from their respective recent cycle highs. That's at least one indication the substantial amount of repair that has been accomplished in the recovery by manufacturers. The same is true for the overarching European Monetary Union reading for manufacturing, where for the entire union the distance from the lowest reading the where the index sits today is twice as large as the distance from where the index sits today to the past peak reading.

However, for services the degree of repair is nowhere as strong: for EMU as a whole the distance from where the current services index sits to its past cycle peak is greater than the distance from where it sat at its past trough. For German services there is slightly more rebound from the past trough but the numbers are pretty close to parity leaving a service sector with much less repair than what has been accomplished by its manufacturing sector. For France the results are dismal. The current French services reading is approximately 8 points off of its low while the current reading is still approximately 15 points from its past cycle peak. France has a great deal of repair yet to do in the services sector.

These statistics remind us of how much the problems in the Eurozone actually are homegrown. The service sector is principally about domestic economic activity. Services, substantially, are nontradeables. As such the revival of the services sector speaks much more what's going on in the domestic economy that to international competitive conditions or demand conditions. Although very clearly the goods sector, or tradable goods sector of the economy, is connected to the services sector, and, when trade troubles affect manufacturing, they will be transmitted to services. However, if that's the main channel of weakness transmitted to services we would certainly expect to see manufacturing as relatively weaker as it would be the cause of that transmission and the service sector would represent the knock-on effect. That's not the case in the European Monetary Union.

While austerity has vastly weakened domestic demand in various domestic economic structures, countries in EMU continue to compete with one another in international trade albeit within a single currency area. Each country also competes with its fellow EMU members and against other foreign competitors in its trade outside of the country and outside of the union. The international environment for trade remains hostile. Growth in the global economy has been weak. There is s a great deal of economic slack and that means, manufacturing faces intense pressure. Even so the recovery of the manufacturing sector for the monetary union is more fully accomplished than the recovery in domestic services.

If we look at the table entitled changes in Markit overall and sector indices we get further indications of what's really going on. Germany a country that has had no real austerity push sees its manufacturing index in the 38.5th percentile of its queue of values measured since December 2000. Its service sector is in almost the same relative position in the 39.6 percentile over that same period. In fact Germany services sector actually is doing slightly better than manufacturing. Germany is experiencing balanced recovery in its manufacturing and services sector. Compare that to France, where the manufacturing index is in the 39.6 percentile of its queue while it services sector languishes far behind, in the 26.4th percentile of its historic queue since December 2000. The overall figures for EMU show that manufacturing has recovered slightly better than services with the manufacturing metric in the 42.9th percentile of its historic queue compares to the 39.6 percentile for services.

As always we try to put the day's news in perspective. The PMI news from Europe is not the only good news today. The European central bank reports that the credit standards for loans in the euro-Area for consumers eased for the first time in nearly 6 years in the second quarter of 2013. This is good news indeed and it reinforces the news from Markit on the PMI recovery. The UK's CBI survey (Confederation of British industry) reinforces the results of a survey on UK exports released yesterday that was very upbeat. The CBI survey finds strength in British order books. However, Spain is raiding a reserve fund or piggy bank intended to backstop pension payments. That's not a good sign for Spanish finances. Therefore it's not a good thing for prospects for European development and growth. Italian retail sales edged ahead (by 0.1% month-to-month) but only on an increase in food sales-that's thin gruel for progress.

More fundamentally I worry about the outlook released several days ago by the Bundesbank which admitted that Germany had put in strong growth in Q2 but attributed that to a bounce back based on improved weather (remember that Germany and other parts of Europe experience some severe flooding this year). Looking ahead the Bundesbank was not as optimistic for growth in the rest of the year. Notwithstanding that, Germany has put in a strong reading for July. But rather than get too carried away with enthusiasm about the new PMI readings, we should be somewhat mindful and wary of the warnings from the Bundesbank and the reasons that improved growth has emerged. As the chart above reminds us, the Baltic Dry Index maybe stirring but this closely-watched barometer of world trade is not exactly pointing to any kind of a rocket trajectory for global growth or trade expansion. While we are seeing some improvement in Europe, we need to be mindful of the challenges that exist and the continuing risk of backsliding that exists in Europe, in Japan, in China, and in the United States. If the global economy or if these various economic areas were rockets, we might be happy with their current trajectory and thrust but we would not yet have escaped the pull of gravity from the planet recession. There may be reason to be optimistic or hopeful but there's no point in getting carried away with optimism. The positive news is not yet good enough.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief