Global| Jul 03 2014

Global| Jul 03 2014EMU PMIs Show Growth Slowdown

Summary

The market diffusion indicators for the euro area show backing off of the composite index in June. The composite index fell to 52.8 in June from 53.5 in May while May itself reflected a deterioration from April's level of 54.0. It's [...]

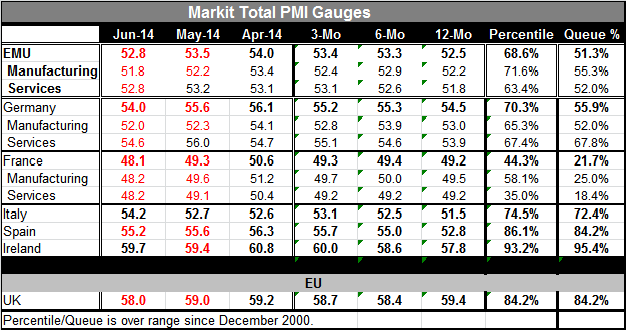

The market diffusion indicators for the euro area show backing off of the composite index in June. The composite index fell to 52.8 in June from 53.5 in May while May itself reflected a deterioration from April's level of 54.0. It's official now that the European Monetary Union's private sector has taken a step back in June. There's a step back taken for manufacturing for two months running and there's a step back for one month for services in June compared to May.

The market diffusion indicators for the euro area show backing off of the composite index in June. The composite index fell to 52.8 in June from 53.5 in May while May itself reflected a deterioration from April's level of 54.0. It's official now that the European Monetary Union's private sector has taken a step back in June. There's a step back taken for manufacturing for two months running and there's a step back for one month for services in June compared to May.

The overall EMU diffusion index at a level of 52.8 stands in the 51st percentile of its historic queue. That queue ranking reflects the fact that the EMU index is higher about 49% of the time and lower about 51% of the time. That's an extremely moderate reading for the overarching private sector index. Manufacturing is only slightly stronger than that, with its 55th queue percentile; services are trailing behind at the 52nd percentile. Notice that the overall EMU percentile standing is slightly lower than either the manufacturing or services in isolation. That means that this degree of weakness together is unusual for the EMU.

For Germany, the total index back slid for two months in a row with the recent June reading at 54.0 compared to May's 55.6. There is a two-month step back for Germany's manufacturing sector and a one-month step backward for the services sector. The level of 54.0, the German private sector composite is in its 55th queue standing, a moderate reading but slightly stronger than for EMU as a whole. Germany's manufacturing queue standing in the 52nd percentile, weaker than manufacturing for the EMU as a whole, but its services reading at 54.6 stands at the 67th percentile and is quite a firm reading for Germany and much stronger than for the EMU as a whole. By now it would appear the German services sector is responsible for much of the good performance of its economy.

France shows extremely low readings for the overall private sector composite as well as for its components. The overall French reading at 48.1 is an outright decline in private sector activity for the second month in a row. And the June reading slump compared to May reading. Manufacturing shows contractions for two consecutive months and slightly lower readings for two months in a row. Services show contracting readings for two months in a row and slightly lower readings for two months in a row. The queue standing of the French indicators is quite depressing. The composite private index is in its 21st percentile. The manufacturing index is at the 25th percentile while the services index is at its 18th percentile. These are extraordinary week indices for the second largest economy that is part of a union that is supposed to be in its recovery phase.

Italy sees continuing improvement in its composite private sector index which moved up to 54.2 in June from 52.7 in May. While showing a higher raw reading than Italy's, Spain's PMI fell to 55.2 in June from 55.6 in May. Ireland shows an increase in its composite PMI after a setback in May. But Italy, Spain and Ireland all have extremely high PMI standings for the composite indices. Ireland leads the pack with the 95th percent standing. Spain is next at the 84th percent standing. That's followed by Italy at the 72nd percent standing. The (slightly) smaller economies appear to be leading the euro area higher (Italy and Spain, respectively, are the third and fourth largest EMU members).

The United Kingdom, not part of the single currency mechanism, has shown a slump in its composites private sector PMI index to 58 in June from 59 in May. May also had seen a slight slippage in the UK reading. However, the composite private-sector UK overall rating is still very strong. The queue standing is in the 84th percentile.

Overall the EMU seems to be in pretty good shape although right now it's lacking for some momentum. The European Central Bank is engaged in a policy of trying to stimulate credit growth and on this day, the ECB held its policy interest rate to the low level that it had set at its previous meeting. Of the countries in the table that report composite PMI indices, we see expansion in place everywhere but in France. Both France's manufacturing and services sectors are struggling mightily. The ECB would have an easier time trying to resuscitate one of the smaller peripheral economies that trying to revive the second largest economy in the euro area.

While the euro area's Economic Commission is allowing some slack and in some cases extra time to reach the debt-to-income metrics for countries that are behaving but still struggling in their growth, France is still pretty played out in terms of the extra time it has been accorded. France is an interesting case because according to the official statistics France is one of the EMU countries that never lost that much price competitiveness to Germany as it causes its inflation rate to track closely with the German inflation rate. However, France has other problems in its economy, especially a number of economic rigidities that seem to still be holding it back. For the moment it would appear that France is the biggest problem that the EMU has to worry about. However, we can't ignore the fact that geopolitical risks are still pretty intense in an economy that's right around the block from the euro area. European heads of state are taking a lead to try to pressure Russian President Vladimir Putin to control his rogue elements in Ukraine and to try to create some kind of a lasting peace and equilibrium situation. The EMU has problems to watch on several fronts.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief