Global| Nov 05 2014

Global| Nov 05 2014EMU PMIs Edge Higher

Summary

The finalized PMI reading for the EMU private sector in October is at 52.1, marginally lower than the flash reading of 52.2 but slightly higher than September's 52.0. The October result still represents a flat-to-weakening profile [...]

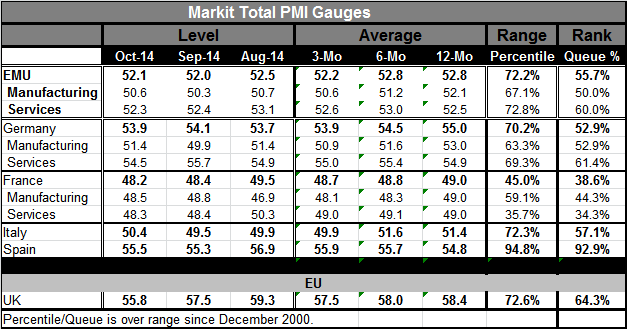

The finalized PMI reading for the EMU private sector in October is at 52.1, marginally lower than the flash reading of 52.2 but slightly higher than September's 52.0. The October result still represents a flat-to-weakening profile over the past 12 months. The 12- and six-month averages of the PMI hold at 52.8. The three-month average is at 52.2 and the October number has slipped below that at 52.1. The index at 52.1 stands in the 55.7 percentile of its historic queue, a moderate reading.

The finalized PMI reading for the EMU private sector in October is at 52.1, marginally lower than the flash reading of 52.2 but slightly higher than September's 52.0. The October result still represents a flat-to-weakening profile over the past 12 months. The 12- and six-month averages of the PMI hold at 52.8. The three-month average is at 52.2 and the October number has slipped below that at 52.1. The index at 52.1 stands in the 55.7 percentile of its historic queue, a moderate reading.

As for the sector indices, manufacturing stands right at its 50th percentile on top of its historic median. It's pattern. However, from 12 months to six months to three months, the moving averages have been moving lower; the October level comes in right on top of its decayed three-month average. The euro area is being supported by its services sector which fell slightly in October to 52.3 from 52.4, a sector that does not have a clear trend in place over 12 months, but has deteriorated steadily from August. The services sector sits in the 60th percentile of its historic queue, a moderately firm reading. The queue standing of 60 means that the index is higher 40% of the time and lower 60% of the time. So the services reading at 60 is moderately firm. The manufacturing index is simply in the middle of its historic range of experience. On balance, there's nothing especially impressive about the October reading for the EMU.

Germany is no longer the strong economy in Europe, at least according to the PMI readings and the percentile standings. Germany's reading slipped in October to 53.9 from 54.1 in September. The German PMI has been slipping steadily from 12 months to six months to three months. Its manufacturing gauge has been slipping as well but that gauge improved to 51.4 in October from 49.9 in September, a level that had indicated some very moderate technical contraction. German services show steady but slow erosion as that sector fell again in October to 54.5 from 55.7 in September. The German sector standings are much like those for overall EMU with manufacturing nearly at its 53rd historic percentile and services in the 61st percentile.

France also provides full sector specifications and they simply confirm the sorry state of the economy. France's sequential averages have been eroding and also have been below 50 for 12 months, six months and three months. In addition, France has eroded in September from August and in October from September. Both the manufacturing and services sectors indicate erosion. Manufacturing shows continued erosion while the services sector is substantially stable at a reading of 49 in terms of the moving averages over the past 12 months. Over the last three months, however, the services sector has been steadily losing some ground. Percentile standings of both French sectors are extremely weak. Unlike Germany and the euro area, the French manufacturing sector is relatively stronger than its services sector standing in its 44th percentile while services stand in their 34th percentile.

Italy and Spain provide overall readings. Italy had been slipping; it steadied in October. Spain has had the same circumstance. Looking at their sequential averages, Italy's have had an irregular erosion from 12 months to six months to three months while Spain's readings have consistently become slightly stronger from 12 months to six months to three months. Spain has a hugely high percentile standing in its 92nd historic percentile, but Italy's standing is in its 57th percentile.

U.K. growth has been slipping; it is not in the single currency area. But over last three months, it has slipped from 59.3 in August to 57.5 in September to 55.8 in October, a quite steady erosion. U.K. moving averages from 12 months to six months to three months have slipped steadily as well. Still, the October U.K. reading sits in the 64th percentile of its historic range.

The PMI readings do not change the story from the flash estimates. We do get a little bit more information about the sectors and what we see still is not very reassuring. In another report released today, euro area retail sales were weaker than expected, falling by 1.3% year-over-year.

The consistent message from economic data is that conditions are weak and that there is not much sign of acceleration. The euro area seems to have flirted with further deceleration, but for the time being, growth is still the order of the day. However, the euro area continues to face challenges. Slipping oil prices are going to put both the European Central Bank and the Federal Reserve behind the eight-ball in terms of their attempts to target prices. Both of these institutions have substantially run out of ammunition that might allow them to reach the targets to which they committed.

The last bad news on the day (so far) comes in Ukraine with the rebels saying that the actions of the Ukraine government have nullified the ceasefire and apparently Ukraine and its renegade republics are technical back to armed conflict. If so, that would be an extremely bad development and will be harmful to European growth and its prospects.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief