Global| Jan 24 2017

Global| Jan 24 2017EMU PMIs Ease on Weaker Services As Manufacturing Continues Stronger

Summary

It's a split decision on the EMU this month as services are weaker and manufacturing is stronger. However, the relatively greater services weight has the tiebreaker in terms of the impact on the overall PMI which is slightly lower in [...]

It's a split decision on the EMU this month as services are weaker and manufacturing is stronger. However, the relatively greater services weight has the tiebreaker in terms of the impact on the overall PMI which is slightly lower in January at least on a flash PMI basis.

It's a split decision on the EMU this month as services are weaker and manufacturing is stronger. However, the relatively greater services weight has the tiebreaker in terms of the impact on the overall PMI which is slightly lower in January at least on a flash PMI basis.

The overall assessments

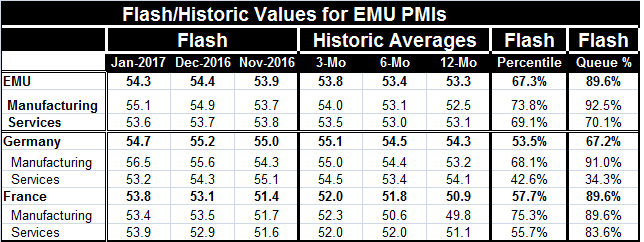

The three-, six- and 12-month averages are calculated in the table above excluding the current month or 'flash' observation. They are for the periods ended in December 2016. For the EMU, the averages show steady strengthening of the shorter horizons, a clear indicator of improving momentum. That is led by manufacturing where the three-month average is 1.5 points higher than the 12-month average. In services, the three-month average is higher than the 12-month average by just 0.4 points. Despite the small walk-back in the services gauge in January (compared to December), the January services gauge is still above its three-month average. This is true for both manufacturing and services; it appears that the expansion is continuing, but for services there is more evidence of a slowing. Manufacturing has accelerated but shows some signs of slowing as well this month (see chart).

Some similarities/some differences

Both Germany and France see improvement in their respective sequential averages for their overall private sector gauges. However, in January the German index takes a step back on a service sector stumble. France continues to show powerful advances in its monthly overall indicator. However, France also logs a weaker manufacturing reading in January coupled with a stronger service sector reading, a flip of the German and EMU results. France's manufacturing sequential averages have continued to advance, but its service sector index flattened out with its three-month and six-month readings dead even. Even so, the January French service sector reading signals that strengthening has continued after this pause.

Overall PMI

We only measure PMI values since January 2011. But on this six-year timeline, the EMU private sector gauge has been higher only 11% of the time. The French gauge has been higher only 11% of the time, but the German overall gauge has been higher 33% of the time. The EMU and France are relatively stronger than Germany even though the absolute reading on the Germany total PMI index is stronger.

Manufacturing

There is a great deal of conformity on manufacturing where the EMU standing for the sector is higher less than 8% of the time, the German standing is higher less than 9% of the time, and the French sector is higher only 11% of the time. Still, in absolute terms, the German PMI reading is much stronger than the EMU diffusion reading (56.5>55.1) and the French manufacturing reading lags both of those (53.4). It is their recent momentum and relative performance that is so similar.

Services sector

The service sector results show a lot more differences. The EMU service sector reading has a 70th percentile standing while France's sector stands in its 83rd percentile. Germany's sector is anemic with a 34th percentile standing; Germany's services sector is weaker than this only about one-third of the time.

What's in train

This month the chart rather than the table tells the clearest story of what is in train for the EMU. The manufacturing sector after languishing has gone on a tear and in January its pace of improvement finally has slowed. Still, the level of the diffusion index is now quite high by recent standards. Services, which have been slowing and have picked up their pace a bit more recently than manufacturing, also have started to break out of their weak patch, but the break-out is less than complete, or to put it another way, less clearly underway and sustainable.

Inflation...

One thing that is quite different is the evolution of inflation. In the EMU, inflation is afoot and deflation is no clear or present danger. But this is mostly because of headline inflation on rising energy prices. So far, ECB President Mario Draghi has failed to acknowledge rising inflation as a factor, calling it transitory. But in Germany, where inflation is a verboten word and a hair-trigger issue, there is much more concern about prices rising partly because inflation is in fact rising faster in Germany than it is in the EMU. Because of the relatively large German weight in EMU data, the German inflation rate will not be able to run wild before it will have a policy-changing impact on the ECB. But for now ECB President Draghi judges that it is 'only energy price inflation' and only a transient issue. That assessment does not sit well with Germany or with the Bundesbank. To them, inflation is inflation and its eradication and control is the sole objective of the central bank.

Snit at the ECB

The ECB was bound to have a snit over this issue sooner or later especially given the way Germany fought against providing stimulus when the European economies needed it so badly. Germany's delaying tactics made ECB monetary policy much less effective than it might have been and now the European economy is still struggling (it is in much worse shape than the PMI data and queue rankings suggest after all). Unemployment rates in the EMU show that most of the original EMU members have rates of unemployment that stand above their respective medians since the EMU was formed. Few of them see this as a time to withdraw stimulus. Germany alone has an unemployment rate on its all-time (since reunification) low. But the German contingent wants all attention paid to inflation- that is the ECB's mandate. For now Draghi fails to see it. While I have no doubt that the Germans will win the argument in the end, they will not be satisfied and will not win it on their preferred timeline. Obstreperousness breeds obstreperousness.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief