Global| Feb 01 2010

Global| Feb 01 2010EMU PMIs Continue To Recovery

Summary

Euro-Area recovery continues - The EU/EMU nation PMIs continue to show recovery. Greece, with its economic difficulties and huge fiscal problems, already is showing signs of an uphill battle. Greece’s MFG PMIs are lower over three [...]

Euro-Area recovery continues - The EU/EMU nation PMIs continue to show recovery. Greece, with its economic difficulties and huge fiscal problems, already is showing signs of an uphill battle. Greece’s MFG PMIs are lower over three months and over six months, only Spain, another Mediterranean country with recovery issues, is in the same boat with MFG PMIs lower over both 3- and 6-mnths. Spain however did mange a PMI increase for the month of January.

Tensions tear at the Euro-Area - The EMU MFG PMI is up for six month in a row. But signs of differences among EMU member countries are beginning to show and coupled with some very specific country-level problems questions about commitment to the zone are starting to arise – right or wrong. Greece has huge budget problems and Spain‘s construction-based ills are going to be a structural impediment to growth for some time to come.

Europe’s differences become a liability - Still, the EMU recovery is looking more and more durable… even if not strong. That some members are having trouble is not surprising. Not even a true single country is uniform in the way a downturn impacts its various industries or regions. Europe is known for its regional differences and differences in efficiencies. For that reason it did not meld its finances together when the EMU region was formed. Each member wanted to maintain its own fiscal independence while some wanted to be shielded from the practices of others. Yet some constraint was needed to keep the union members fiscally close enough for a currency union to work. EMU adopted rules for budget responsibility to constrain the budget gaps across nations. It was hoped that the rules (Maastricht criteria) would succeed in keeping finances on a reasonably similar footing so that fiscal imbalances would not tear the union apart.

Recession as Economic Cat-scan - In any event this severe recession has come suddenly and exposed creeping or hidden imbalances and revealed sharp fiscal differences. Greek government bonds are now some 400 bp in yield above those in Germany and this is for government bonds in the same union with no foreign exchange risk – except for those who think the union could be split by this sort of pressure.

The missing link in Europe - besides lacking true fiscal limitations that work – is the lack of mechanism to close regional competitiveness gaps. Sharp regional differences have endured and broadened. Without the ability to depreciate exchange rates within the region it is hard for a nation to regain when its competitiveness slips. While the growing budget gaps are a public issue the growing competiveness gaps are a bigger problem and one that is harder to solve. Cutting nominal wages or boosting productivity are both hard to do it. Yet both are easier said than done. Closing a fiscal imbalance by hiking taxes or cutting spending is comparatively much easier – simple to do in fact although hard to find the will.

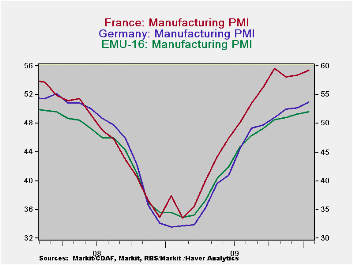

Recovery in train but not strong enough to bail out Greece - The recovery is still ongoing and that is good news since growth can cure all ills if the growth is fast enough. But the recovery in MFG is already slowing. The EMU MFG index has risen by 6.14 points over six months and by only 1.66 points over the last three months. Italy’s MFG sector is showing the best maintained ‘pace of recovery’ as it is up 6.39 point over six months and 2.51 points over three months indicating only a slight slowing in the pace of improvement. Other are growing faster over six months (France and Germany) but Italy is maintaining its pace of expansion best.

Euro laggards - Spain and Greece are down the most from their past cycle peaks; among the countries presented in the table each is down by some 12 points compared to an 8 point shortfall for EMU as a whole. Contrast this to the UK which has its MFG index back at its peak. Greece is also up by only 8 points from its cycle low point, the feeblest recovery of this group. Germany for example is up 21 points from its cycle low.

Questions for the Euro-Area - On balance Europe has some issues that are now starting to dog the euro. The dollar has regained some luster even though the US fiscal situation is not exactly rosy. No one is quite sure how deep Europe’s rift will run and what the Europeans will have to do to solve their problems. When push came to shove Iceland got bailed out and now Iceland is reluctant to undertake actions to pay back those that bailed it out. Will the Union come to Greece’s aid or will Greece be forces into an independent severe adjustment? In the end the Zone looks a lot like the global banking sector operating with a fatal flaw it thought it could circumvent with a simple rule as a fix. Is the Zone really like a bank with off balance sheet obligations that are about to be brought back on board or will Greece be left to deal with its issues alone?

The Really BIG risk - If the burden left squarely on Greece’s shoulders, does that mean that Greece would try to opt out of the Union? If that happened how would speculation spread to others? No one is quite sure and since the euro-recovery does not seem to be strong enough to save Greece on its own all these are live issues to one extent or another. Thinking about one country exiting the Zone naturally will bring pressures on some others. It is unclear if that means Europe will pitch in to help Greece and set an undesirable precedent or not. Germany already has made great sacrifice to pull the former E Germany into its economic orbit. Would Germans be willing to do more to assist Greece after the Zone was formed with a cushion to try and prevent that sort of thing from happening? These are exactly the sorts of unexpected issues that financial crises put on the table. The UK’s decision to remain part of EU but to not join EMU is looking more and more prescient. Stay tuned.

| Changes in Markit MFG Indices | ||||||||

|---|---|---|---|---|---|---|---|---|

| Changes Mo/Mo | Change on Frequency | |||||||

| Jan-10 | Dec-09 | Nov-09 | 3Mo | 6Mo | 12Mo | From Peak | From Low | |

| Euro-13 | 0.80 | 0.39 | 0.47 | 1.66 | 6.14 | 17.97 | -8.1 | 18.8 |

| Germany | 1.02 | 0.25 | 1.40 | 2.67 | 8.08 | 21.75 | -7.2 | 21.8 |

| France | 0.73 | 0.31 | -1.21 | -0.17 | 7.31 | 17.54 | -9.4 | 20.6 |

| Italy | 0.95 | 0.71 | 0.85 | 2.51 | 6.39 | 15.69 | -8.2 | 17.2 |

| Spain | 0.08 | -0.09 | -1.02 | -1.03 | -2.06 | 13.76 | -12.2 | 16.8 |

| Austria | 1.03 | 0.88 | -1.12 | 0.79 | 5.38 | 18.72 | -7.0 | 18.7 |

| Greece | -1.98 | 1.54 | -0.72 | -1.16 | -2.01 | 6.83 | -12.6 | 8.6 |

| Ireland | -0.72 | 0.02 | 0.78 | 0.08 | 4.43 | 9.15 | -8.3 | 14.9 |

| EU | ||||||||

| UK | 2.05 | 2.32 | -0.73 | 3.64 | 6.20 | 20.06 | 0.0 | 21.8 |

| percentile is over range since March 2000 | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief