Global| Oct 03 2013

Global| Oct 03 2013EMU PMIs Continue to Advance in Services

Summary

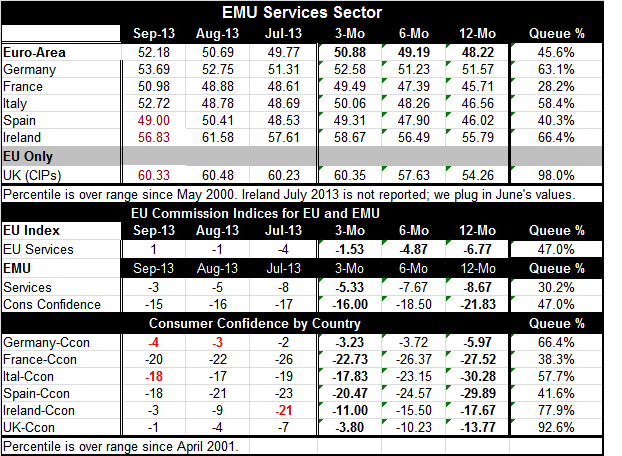

The EMU services PMI rose to 52.18 in September from 50.69 in August. This marks only the second month in a row that the EMU service sector is expanding. Previously January 2012 was the last observation above 50. At this level the EMU [...]

The EMU services PMI rose to 52.18 in September from 50.69 in August. This marks only the second month in a row that the EMU service sector is expanding. Previously January 2012 was the last observation above 50.

The EMU services PMI rose to 52.18 in September from 50.69 in August. This marks only the second month in a row that the EMU service sector is expanding. Previously January 2012 was the last observation above 50.

At this level the EMU reading stands in the 45.6 percentile of tis ordered queue of historic values. It has been higher 55% of the time and lower about 45% of the time. That's not a great reading.

Germany imparts a strong positive bias to the EMU reading because of its heavy weighting. Germany's index stands at 53.69 and resides in the 63rd percentile of its historic queue a relatively more solid standing. Germany's service sector reading averages above 50 for 3-months, 6-months and 12-months. Only tiny Ireland and the UK can match that.

The UK service sector edged slightly lower on the month but still resides at an incredible 98th percentile of tis historic queue.

The EU commission readings for the service sector in EMU are weak as that reading stands only in the 30th percentile of its historic queue (we evaluate its net EU Commission readings using the queue method for compatibility between the two methods diffusion methods).

Consumer confidence percentile standings are generally the same as service sector readings or a bit higher.

The monthly report on services shows gain for EMU but still great differences within the Zone. Every country in the table shows improvement over three-months compared to six months. All but the UK and Spain are better off in Sept than their respective 3-mo averages. Only Germany fails to show a better 6-mo average than 12-mo average.

So progress continues in the Zone and in these member countries' services sectors. Progress however is slow and the stratification among members continues to be a dividing point.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief