Global| Jan 23 2014

Global| Jan 23 2014EMU PMIs Continue Higher

Summary

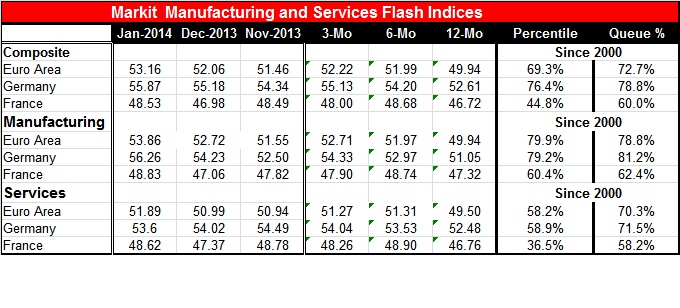

The Markit PMI data in their flash incarnation showed an increase in the composite reading for the euro area in January. The composite rose to 53.16 from December's 52.06, marking only the second increase in a row. The composite [...]

The Markit PMI data in their flash incarnation showed an increase in the composite reading for the euro area in January. The composite rose to 53.16 from December's 52.06, marking only the second increase in a row. The composite measures for Germany and France also increased. For Germany it was the third consecutive rise and for France it was the first increase after three monthly declines.

The Markit PMI data in their flash incarnation showed an increase in the composite reading for the euro area in January. The composite rose to 53.16 from December's 52.06, marking only the second increase in a row. The composite measures for Germany and France also increased. For Germany it was the third consecutive rise and for France it was the first increase after three monthly declines.

The average PMI readings for the euro zone composite show steady improvement from the 12-month to the six-month to the three-month averages; the same is true for Germany. For France, however, there is an increase in the six-month average compared to the 12-month average, but over three months the composite is backsliding compared to six months. The data continue to show France as a fly in the ointment as far as the European recovery is concerned.

The French composite measure also has stayed below 50, technically below the level that signals expansion for the French economy. France's manufacturing indicator moved up in January compared to December and its services indicator moved up as well, but each of them is below 50, the point economic neutrality.

Looking at the data for the euro zone as a whole, we see that the ranking of the manufacturing indicator in its queue history is in the 78th percentile compared to services which are in the 70th percentile. These measures are standings of each respective measure, portrayed as a percentile of its historic queue of ordered data. Thus, the manufacturing sector is approximately eight or nine percentage points better than the services sector on a percentile basis. This is quite different from comparing the raw readings as we are comparing the raw reading in each case with a historic average to create a new relative barometer. But what this process tells us is that the euro area is being led by its manufacturing sector. For Germany, the same process is in train. Germany's manufacturing sector is in the 81st percentile of its historic queue while services are in the 71st percentile; they are solid readings and again manufacturing outstrips services. For France, we see the same is true but the margin is much narrower; France has manufacturing in the 62nd percentile with services in the 58th percentile.

Overnight we also received a PMI reading for the manufacturing sector in China which slid back below the 50 mark. Although it has not been below 50 in a number of months, the increment below 50 is actually rather narrow. China slid only to a reading of 49.6 with its index at a six-month low. While markets have reacted to this, maybe they should not. China is becoming a more insular economy as it is backing off its reliance on export-led growth and trying to develop domestic demand. This transition is creating several difficulties in the Chinese economy. But since China had been a net export-led growth country, China's slowdown really does not have the same ominous implications for the rest of the global economy as it used to have. It is not the litmus test for global demand that it used to be. China is transiting to a country that relies more on some of its own domestic demand growth and develops its own services sector; it is in the process of becoming a less voracious international competitor because, in order to develop domestic demand, it will have to raise wages and that will undermine Chinese competitiveness and export prowess.

We are in a period of transition for all the world's economies and we have to be careful how we interpret some of these reports because the new context is different from the old.

Returning to the euro zone, Spain showed its second consecutive quarter of positive GDP growth. Although the growth rate once again was small, it was positive. This underlines that Spain does have a real recovery in progress even if it remains really weak. Spain also finished last year with an unemployment rate above 25%, underscoring challenges ahead despite its start to turn the corner on growth.

Importantly, the German leading economic index for November shows that Germany's expansion is still well in place and it reinforces the newer signal from the Markit PMI data.

News from today's data is that the European recovery is still in train. A recovery that seems to embrace both the goods in the services sector is making solid progress. France, which has been a troublesome economy, continues to have its issues. Although the French manufacturing and services sectors improved in January, they continue to point to sector contraction. So this underscores that there may be an overarching recovery in place in the European Monetary Union, but it is also a recovery with a great deal of variability. Although we can call that `recovery,' it is a recovery that continues to carry considerable risks.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.