Global| Aug 23 2017

Global| Aug 23 2017EMU PMI Ticks Higher As Manufacturing and Services Diverge

Summary

In the EMU, manufacturing carries the day to move the sticks higher for the overall PMI gain as the service sector reading steps backward in August. The EMU manufacturing gauge gained 0.8 points in August while the services gauge lost [...]

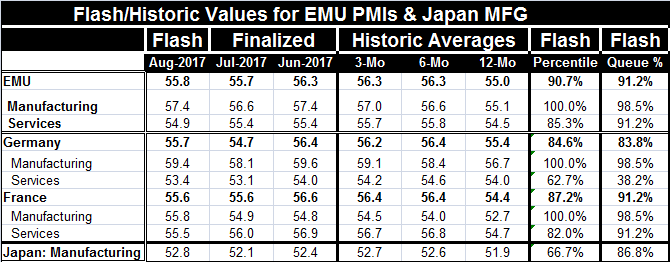

In the EMU, manufacturing carries the day to move the sticks higher for the overall PMI gain as the service sector reading steps backward in August. The EMU manufacturing gauge gained 0.8 points in August while the services gauge lost 0.5 points. Manufacturing sits above its three-month average as its 12-month to six-month to three-month progression of averages shows steady increases. The services gauge in August sits below its three-month average. In terms of progressions, the three-month average for services is below the six-month average; conditions are losing momentum there and have been for some time.

In the EMU, manufacturing carries the day to move the sticks higher for the overall PMI gain as the service sector reading steps backward in August. The EMU manufacturing gauge gained 0.8 points in August while the services gauge lost 0.5 points. Manufacturing sits above its three-month average as its 12-month to six-month to three-month progression of averages shows steady increases. The services gauge in August sits below its three-month average. In terms of progressions, the three-month average for services is below the six-month average; conditions are losing momentum there and have been for some time.

Evaluated over the last five and one-half years, the PMI levels in August show the overall EMU PMI standing is among its top 10% highest readings with the manufacturing sector readings strong (98.4 percentile standing- at its top reading in the last 5.5 years) and with another strong 90.3 percentile standing for services. The levels of the sector readings are still very high, but manufacturing is carrying solid momentum while the service sector is not. This is well depicted on the graph.

Germany mirrors the EMU result with a stronger manufacturing reading in August and with a rising profile of the sequential averages of its manufacturing gauge. Germany's services reading in August also advances-unlike the EMU, but the three-month average for services is below its six-month average as is the case in the EMU overall.

Germany also has a much weaker services sector than does the EMU. Rated over the last five and one-half years, the current German service sector standing is only in its 33rd percentile, a very low position. This contrasts sharply with the manufacturing standing which is at the 98.4 queue percentile standing and is the highest reading in the last five and one-half years.

The French PMI gauge sits unchanged for the month on a level that is slightly below its three-month average. France's three-month and six-month averages for its overall PMI are the same as momentum has stalled. French manufacturing showed another advance in August and has the same relative position as Germany and the overall EMU manufacturing reading as the highest reading in the last five and one-half years with manufacturing on a clear rising profile. Services, on the other hand, stepped back in August and France's three-month average is below its six-month average for services. Still, French services have a 90th percentile queue standing.

Japan also reported out a PMI reading for August. Its gauge rose to 52.8 from July's 52.1. Japanese averages for manufacturing show a rising progression from 12-month to six-month to three-month with the current reading above its three-month value. Japan's reading stands in the 85th queue percentile, a relatively strong reading.

On balance, the Markit 'flash' or preliminary gauges show expanding activity in both manufacturing as well as in services. The manufacturing readings are more consistently strong and on rising profiles while services are off peak and seem to have lost some momentum. And that is important because the services sector is the main source of job and income growth. Revival in manufacturing is important because that is the sector that mainly connects one economy to another in global commerce. If manufacturing can revive in Europe, it is probably reviving everywhere; that is the nature of that global beast. The same cannot be said of services which retain local distinctiveness.

Still, the underlying thrust is for growth and the day's reports are mostly reassuring in that respect. In Europe, Mario Draghi was making remarks ahead of his Jackson Hole, WY appearance and reminding us that in his view QE has been effective but also admonishing us to realize that there is a lot about the new modern economy we do not yet understand. This seems to be another classic Draghi observation about why policy should be patient and move slowly.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief