Global| Dec 16 2014

Global| Dec 16 2014EMU PMI-The Sum Is Stronger Than Its Two Largest Parts; EMU Up; France & Germany Down

Summary

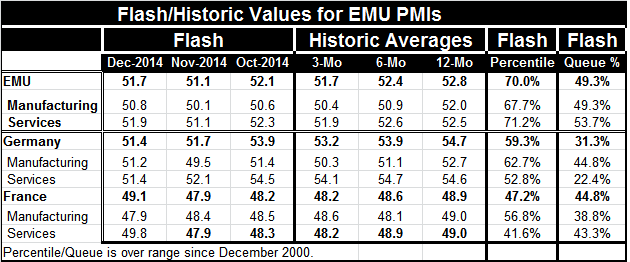

The overall EMU flash PMI rose to 51.7 in December from 51.1 in November. The EMU moving averages for 12-months to 6-months to 3-months show a steady deterioration for the total EMU PMI and the EMU manufacturing PMI. The EMU services [...]

The overall EMU flash PMI rose to 51.7 in December from 51.1 in November. The EMU moving averages for 12-months to 6-months to 3-months show a steady deterioration for the total EMU PMI and the EMU manufacturing PMI. The EMU services measure has only a technical deviation from this same deteriorating progression.

The overall EMU flash PMI rose to 51.7 in December from 51.1 in November. The EMU moving averages for 12-months to 6-months to 3-months show a steady deterioration for the total EMU PMI and the EMU manufacturing PMI. The EMU services measure has only a technical deviation from this same deteriorating progression.

Germany shows the same deteriorating progression in its moving averages for its total PMI, the manufacturing PMI and the service sector PMI. However, the German manufacturing PMI did bounce higher this month to 51.2 from 49.5 in November.

France shows continued deterioration. Its overall manufacturing and services PMIs get progressively weaker from 12-months to 6-months to 3-months. Yet, France shows an uptick in its overall PMI in December led by a bounce in its services sector.

The main message from these metrics is that the EMU and its two main economies are still on a deteriorating path. The slight rebound for France in December still leaves it in a contractionary phase. As for the month-to-month rise in the EMU PMI, we will have to see if it holds up on revision- these are the flash readings. As of mid-December geopolitical events are still going haywire. Overnight Russia has just hiked its interest rates hugely to try to stabilize the plunging ruble. Weak oil prices will help consumer countries eventually, but they are falling so fast that they are also responsible for market chaos right now.

The queue percentile standings for the EMU, France and Germany show that all the sectors are weak. Of the three sets of readings totaling nine PMI metrics overall, only the EMU services sector has a standing above its 50% mark (above its historic median). Germany has been weaker only 31% of the time and its services sector has been weaker only 22% of the time. France has been weaker 44% of the time and its manufacturing sector has been weaker only 38% of the time. The EMU is relatively stronger than its two largest members. It has been weaker overall only 49% of the time; its manufacturing sector has been weaker 49% of the time and its services sector has been weaker 53% of the time. The queue percentile readings are snapshots of where the current readings stand in their historic pantheon of values. Apart from that, we have already established that momentum is still working lower. And no PMI reading is even near `firm' let alone `strong.'

The PMI readings for December are a disappointment. Today China also reported a manufacturing reading that showed contraction for that economy. The U.S. has been one of the few bright spots in the global economy although in a different report, the German ZEW reading showed its second straight improvement in December. However, the ZEW reading stands only in its 36th percentile, not too different a placement from the overall PMI standings, just with a touch more upward momentum. So `on the other hand', there is no `other hand.' Economic conditions in Europe are weakening and global geopolitical conditions are increasingly strained.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief