Global| Nov 23 2015

Global| Nov 23 2015EMU PMI Climbs - Much Ado about Very Little

Summary

The Markit private sector PMI flash gauge rose by 0.4 points in November the 25th largest one month gain in the last 70 months. However, even that small gain brought the level up to its highest value since May 2011 bringing the index [...]

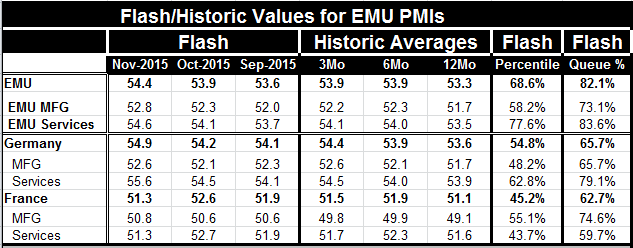

The Markit private sector PMI flash gauge rose by 0.4 points in November the 25th largest one month gain in the last 70 months. However, even that small gain brought the level up to its highest value since May 2011 bringing the index to the 82nd percentile of its historic queue of values since January of 2010. That is a relatively high standing per se but it is for a period in which growth has remained sub-par. The manufacturing gauge moved up by 0.5 point to its highest level since April 2014. Services improved by 0.4 points to stand at their highest level since August 2014. The services sector sits in the 83rd percentile of its historic queue of values while the manufacturing sector is in its 73rd percentile.

The Markit private sector PMI flash gauge rose by 0.4 points in November the 25th largest one month gain in the last 70 months. However, even that small gain brought the level up to its highest value since May 2011 bringing the index to the 82nd percentile of its historic queue of values since January of 2010. That is a relatively high standing per se but it is for a period in which growth has remained sub-par. The manufacturing gauge moved up by 0.5 point to its highest level since April 2014. Services improved by 0.4 points to stand at their highest level since August 2014. The services sector sits in the 83rd percentile of its historic queue of values while the manufacturing sector is in its 73rd percentile.

However, Europe is now beset with a full blown refugee crises intensified by a terrorist attack in Paris and an ongoing manhunt that has put Brussels under a lock down all weekend long and extended into Monday. The impact of these two related events still casts a pall over the outlook despite the recent bump up in the EMU PMI gauges. Believe those indices in isolation at your own risk

Several other trends are in play. The first of which is another weakening in oil prices which are hanging just off near term lows. Both Brent and WTI oil prices are sagging while gasoline prices in the U.S. are at 10-month lows. The energy surplus is still in full force although perhaps tempered by reports that frackers and other producers in the US finally are struggling and some are under pressure to shut down with oil in the $40-$50/barrel range. Still, there is weaker growth abroad and little evidence of a demand pick up.

In Germany the IW think-tank has projected growth in Germany of 1.5% into 2016, slower than its 1.75% outlook for 2015. It looks for a slowing of private consumption to 1.5% from 2%. Clearly this kind of slowing will not be good for EMU growth and will not help to underpin sagging oil prices.

Despite an outlook for slower growth, Germany is doing well for now - excellent by the standards of fellow EMU members - and its inflation rate is one of the higher ones in EMU, rising especially strongly over three-months. It is not surprising that Bundesbank President Weidmann is urging the ECB to give past efforts more time to work and trying to block current plans to increase monetary stimulus that Mario Draghi has all but pledged to undertake in December. Germany has become the high inflation country in EMU and does not like it.

As the position of the U.S. monetary authorities has clarified the U.S. dollar has come under more pressure. The euro has withstood an attack this morning at $1.06 level but the dollar is rising again and commodity prices are being pressured lower by this move. These trends will continue as U.S. monetary policy continues to press rates up and deflation will be spread through commodity prices although the Fed tries to deny, ignore, or minimize this channel.

Meanwhile, everyone will be putting a positive spin on today's evidence of the great strides made by the Markit PMIs in EMU. But I would offer a word of caution. While Germany, a manufacturing center economy, its PMI improved in November, but its gains were small and its MFG index is only on top of its 3-month average- not much momentum there. Moreover, the index stands only in the top one-third of its historic queue of values. As noted above the IW institute looks for weaker German growth in 2016. Germany's service sector is holding the economy up, but consumer spending is projected to weaken in 2016...

France, the second largest EMU economy saw its PMI index fall and reside below its three-month average. Its MFG sector though stands nearly in the top quarter of its historic queue of values and yet is barely signaling an expansion at all (at 50.8). The French services index sank in November and has only a 59th percentile standing.

The fact that for all of EMU, and in Germany, services have higher standings than manufacturing is a testament to the importation of weakness from abroad. After all the euro exchange rate is a weak one and EMU exporters should be highly effective in competition outside of the region. Yet manufacturing is weaker than services, not stronger. Of course, for competitiveness to work, a country needs growth in export markets since being highly competitive in a shrinking market will not count for much export growth. The further problem with growth in services is that it is growth in the least productive low growth sector. It is the sector of lower wages. It is a sector which will add only to a nation's trade deficit since services are rarely exported yet workers employed in service sectors will spend their incomes on goods imports.

My assessment of this month's Markit indices for EMU is that they may be a last hurrah of strength. Nothing in EMU has improved to account to this pick up. The refugee crisis and terrorism will be clear negatives for normal growth although they may promote spending of a different and low-multiplier variety such as spending on refugee welfare and on security. I would still caution about the future and the risks from the likely internal discord from the ECB's attempt to deliver more stimulus and the schism in the policy paths between the ECB and the Fed. There are too many dangerous trends in play to be optimistic. And, of course, geopolitical risks are too entangled to fully sort out and handicap. Many of these threads will create some great investment opportunities, but only for those who are willing to see the flaws and to bet on the fallout.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief