Global| Jan 23 2015

Global| Jan 23 2015EMU PMI: Best in Four Months...Still Not Very Good

Summary

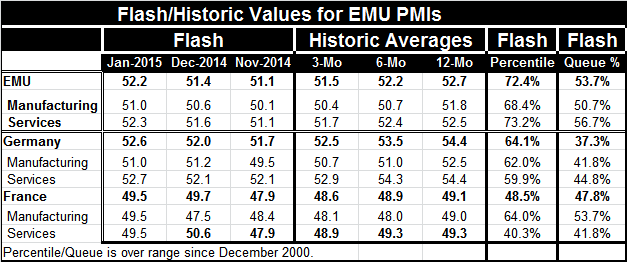

While the EMU flash-gauges rose in January from their December values, Germany saw manufacturing deteriorate while France saw deterioration month-to-month overall and in services. Despite the month's for EMU pickup- for the euro area [...]

While the EMU flash-gauges rose in January from their December values, Germany saw manufacturing deteriorate while France saw deterioration month-to-month overall and in services. Despite the month's for EMU pickup- for the euro area the strongest reading in four months- the averages over three months, six months and 12 months still show steadily declining momentum. The January reading is above the three-month average in most instances. But that is a small ray of hope.

While the EMU flash-gauges rose in January from their December values, Germany saw manufacturing deteriorate while France saw deterioration month-to-month overall and in services. Despite the month's for EMU pickup- for the euro area the strongest reading in four months- the averages over three months, six months and 12 months still show steadily declining momentum. The January reading is above the three-month average in most instances. But that is a small ray of hope.

The PMI queue standings put the overall and both sector reading for the EMU above their respective historic medians (above 50%). However, for Germany and France, all readings are below their respective medians save the French manufacturing gauge at 49.5, is showing net contraction, yet is above its historic median value. Once again we find thin gruel for good news. Three of four sector readings for France and Germany have queue standings below their respective 45th percentiles.

The chart makes it clear that the recent swoon is significant and ongoing. It also is clear that this is a slowdown and nothing like the setback seen at the time of the recession and financial crisis. Manufacturing in the EMU is showing more stability than bounce, while the services sector in the EMU is showing some real bounce. Since Germany and France are still mostly lagging, what we find is that the improvement is outside these two nations in the rest of the EMU. Maybe the weaker euro is helping, but the services sector is showing the higher queue standing and greater improvement.

The various diffusion indices stand relatively higher in their high-low ranges (percentiles) than in their respective queue standings. This is because in recession the bottom falls out and by comparison there are fewer observations in the lowest echelons. The queue standings place the diffusion index in a queue of values using all observations for the standing calculation while the percentile uses just three: the current observation, the high and the low.

The ECB's QE plan is not what you think: Yesterday the European Central Bank finally fleshed out its QE plan. It was a bit larger than expected and has an open ended feature since the end is geared to idea of getting inflation back on a correct policy path. However, the real news is in the way the bond buying will be done through the local national banks rather than by the ECB itself. This undermines European unity. The ECB will give marching orders to the regional banks who will take the risk of QE by buying their bonds locally. This stipulation is at the behest of the Bundesbank that would have opposed a plan so large that put the ECB itself at risk. This technical detail makes the ECB much less a creature of EMU and much more one which is insulated from risks at the country level. The mutualization of risk is diminished the sense of the euro area as a `single place' is further eroded. Countries can no longer say `we are all in this together' since they are 'all in this with risks isolated and contained separately.' After all this time, the EMU is moving closer to fracturing that to uniting.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief