Global| Jun 26 2015

Global| Jun 26 2015EMU Money Growth Slows...So?

Summary

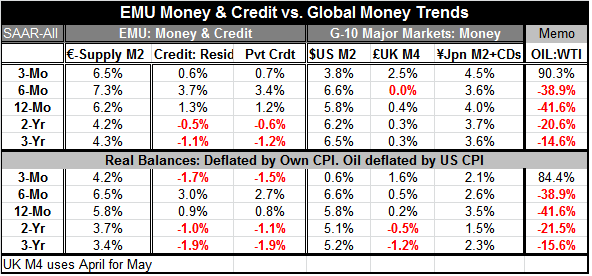

Money growth in the EMU has slowed in May and over three months, but its three-month growth rate is still above its 12-month pace. Money growing at 6.5% in the low-growth slow-inflation EMU represents an improvement of sorts in [...]

Money growth in the EMU has slowed in May and over three months, but its three-month growth rate is still above its 12-month pace. Money growing at 6.5% in the low-growth slow-inflation EMU represents an improvement of sorts in economic conditions, but it's not an improvement to be exaggerated. Annual money growth in the EMU is at its fasted pace since 2009. It is now part of a process that has pulled credit growth up into positive territory even if credit growth is weak. Weak credit growth is far superior to contracting credit growth. These two financial variables make it look as though the EMU may finally be headed for a true recovery. But money growth comes about either as preferences for liquidity improve, as growth takes hold, or as the process of loan creation gets in gear and causes more bank deposits to be created. To some extent, the EMU rise in money growth is due to changing liquidity preferences and money hoarding. But as the credit line shows, there is also real credit creation in gear.

We know that Greece has been a source of money hoarding recently as its economic circumstances have deteriorated and its position in the EMU hangs in the balance. Even as the final deadline approaches in negotiations with the EU, Greece has not been able to cobble together a deal to preserve its creditworthiness and its status as an EMU member. And the result has been a run on banks in Greece and money hoarding by Greek citizens so much so that the ECB has been constantly upping its emerging reserve provision to help Greek banks meet the deposit drain so customers can withdraw euros while they still can. Some Greeks fear that if the negotiations with the EU fail, their domestic deposits could be converted to a new drachma with much less purchasing power. Obviously, money growth that comes from this sort of shift in liquidity preference is not good for growth.

Despite these sorts of distortions, there is some evidence of ongoing EMU-wide improvement. We see it in economic indicators and we see it in the gradual expansion of private sector credit. Money growth has stepped up more that credit growth, but both are on a better trajectory.

Money growth globally in the major money center countries is expanding with the exception of the United Kingdom. U.K. money growth has been slightly negative but has progressed to zero growth. In Japan, M2-plus CDs is expanding slightly more rapidly. In the U.S., M2 growth has generally stabilized but has turned weaker over the last three months. Monetary accommodation is still the name of the game in terms of money growth and the level of interest rates. The U.S. and the U.K. are pondering making a switch to a less accommodative posture. Despite those plans, the IMF has urged the Fed in the U.S. to put off hiking rates for the sake of the global economy. Just yesterday the IMF staff expanded its criticism urging the Fed to abandon its program of releasing `the dots' or year-end point forecasts of where individual FOMC members think rates will be in the future.

While the Fed prides itself on openness and strives for clarity and transparency, the IMF has pointed out that giving the market many forecasts to contend with is confusing and offering one would be superior. The Fed has perhaps overstepped the bounds of credibility in trying to give markets guidance and inform them of its plans in recent years. But in the end even the Fed's Chair, Janet Yellen, has warned observers about drawing conclusions from the Fed's dots.

Central banks remain challenged in trying to start growth especially in a weak economic environment of deleveraging and fiscal austerity. Perhaps communication and transparency are not the central banks' biggest problems these days? Perhaps- just perhaps- we are learning of the limitations of monetary policy. It's not snake oil after all.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief