Global| Apr 28 2017

Global| Apr 28 2017EMU Money and Credit Perk Up; Financial Indicators Join the Optimism Parade

Summary

There is nothing here to knock your socks off. So you needn't be wearing sandals to read this. But the financial signals are glowing brighter. There is some noticeable acceleration in EMU money and credit growth. And those are good [...]

There is nothing here to knock your socks off. So you needn't be wearing sandals to read this. But the financial signals are glowing brighter. There is some noticeable acceleration in EMU money and credit growth. And those are good developments along with indicators of growth elsewhere.

There is nothing here to knock your socks off. So you needn't be wearing sandals to read this. But the financial signals are glowing brighter. There is some noticeable acceleration in EMU money and credit growth. And those are good developments along with indicators of growth elsewhere.

In the ECB meeting this week, ECB President Mario Draghi said two somewhat conflicting things: (1) he did admit to conditions improving but (2) he also cautioned that the stimulus program was likely to be needed for some time to come.

To sum up, the EMU is doing better and that is the good news. The financial indicators echo that sentiment this month for the first time in a while. But there is still quite a ways to go to put things right in the EMU and that may take ongoing stimulus. This message is highly similar to the one delivered by Mr. Kuroda at the Bank of Japan also on Thursday of this same week. The similarity in the message from two very distant economics each plugged into the same global framework may tell us more about the nature of global growth than any other single report.

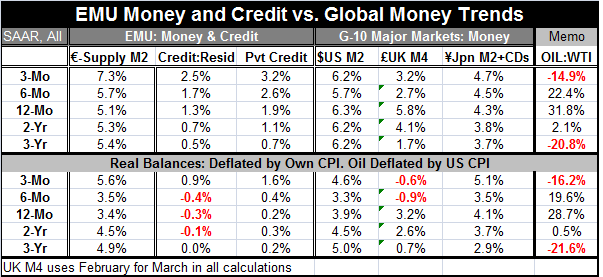

Let's turn to the ECB's numbers. Three-month M2 growth in EMU is up to a 7.3% pace. This is up from growth rates of 5% to 5.5% over the past three years and of 5.7% over six months. This is a significant and noticeable acceleration. Real balance growth (money growth adjusted for the effects of inflation) is up to a three-month pace of 5.6% and that is up from 3.5% to 4.9% over the previous three years and previous six months.

Credit to residents has accelerated to 2.5% over three months, up from 0.5% to 1.3% over the previous three years and up from 1.7% over six months. This is still a pretty weak number, but historically it is a 'break out' development if it can endure and progress. Real credit growth has been flat or negative on all horizons; that has flipped to a 0.9% growth rate over three months. Again it's a clear improvement from recent past trends, but still a weak number.

For private credit, the nominal gain is up to 2.6% over six months and 3.2% over three months and those metrics compare to annual growth in the range of 0.7% and 1.9% over the previous three years. In inflation-adjusted terms, credit growth is up to a 1.6% pace over three months but only 04% over six months compared to a marginal gain of 0.2% to 0.3% over annual periods in the previous three years.

What we have are some still very fresh, nascent, but hopeful trends. The chart shows year-on-year growth rates and on that basis that private sector loan volume is continuing to accelerate mildly while money growth has arrested its weakening trend and is moving higher.

Elsewhere in money center countries, money growth is flat to slightly better. In real terms, there is slightly better growth in the U.S. and in Japan, but the UK shows credit weakness. Today one of the U.K. housing surveys, Nationwide, showed house prices at a four-year low.

It was a day of many economic reports. Euro area flash inflation stepped up in April with headline inflation up to a 1.8% gain and core prices up by 1.1% over 12 months. Headline inflation is gaining at a 0.4% annual rate over three months while the core is rising at a 1.5% annual rate over three months as oil continues to largely call the tune on inflation changes. Among the four largest euro area economies, year-over-year inflation is up at a 1.4% pace in France, at a 1.8% pace in Germany, at a 2% pace in Italy, and at a 2.2% pace in Spain.

Spain and the U.K. reported Q1 growth with the U.K. posting the slowest quarterly growth in a year and Spain showing a slight step up in growth at a 0.8% quarterly gain.

In Germany, retail sales climbed out of the hole they fell into last month more or less reversing the drop of one month ago.

In Asia, Korean IP gained 1% on the month in March. In Taiwan, GDP slowed to a 2.6% gain, down from 2.9% in the previous quarter. In Japan, there were some mixed trends. Housing ticked higher in Japan in March but after a much weaker previous month. Japan's retail sales rose by a small 0.2%, but household spending in Japan fell by 1.3% year-on-year in March. Japan's IP fell by 2.1% in the month but after a previous monthly gain of 3.2%. Japan's IP is still up by 3.3% over 12 months. Both core and headline inflation in Japan rose by 0.2% on the month as the jobless rate remained steady and job-to-applicant ratio rose of 1.45. Despite the volatility and mixed nature of these signals, the balance of Japan's news is upbeat.

There is always variability in economic data and we see that in the day's reports from Europe to Asia. But conditions remain overwhelmingly pro-growth conditions. Once again there is not much here to scream acceleration, but there is growth and not backsliding and that is good news enough for now. Central banks can put those six-shooters back in their holsters; it's growth, not a stampede. It is on balance, not a bad set of data to take into the weekend with some peace of mind about economic growth even if the U.S. government shut down threat is still looming. Hey, it's always something.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief