Global| Jul 27 2017

Global| Jul 27 2017EMU Money and Credit Growth Rates Remain Listless

Summary

Globally only the UK growth rate for money is accelerating; Central bank communication requires a code book EMU M2 money supply growth ticked higher in June as the year-on-year growth rate moved up to 5.1% from 4.9% where it has [...]

Globally only the UK growth rate for money is accelerating; Central bank communication requires a code book

Globally only the UK growth rate for money is accelerating; Central bank communication requires a code book

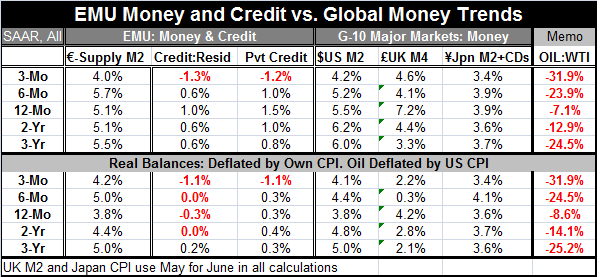

EMU M2 money supply growth ticked higher in June as the year-on-year growth rate moved up to 5.1% from 4.9% where it has slipped. The 5.1% pace is still even with growth rates logged in April and May. One year ago EMU M2 was growing by 5.1% in June. Total credit growth over 12 months has been stuck at or near a growth rate of 1% for 10 straight months except for a one month uptick in March when it grew at a 1.3% year-on-year pace. Private credit was growing at 0.5% annual rate around the middle of last year. It picked up and saw a peak rate of growth at 1.9% in March of this year. However, the growth rate has since decelerated in March and again in April. In May and June, it logged a growth rate of 1.5%, a full percentage point faster than its pace of one year ago, but still an unimpressive detectable only on an electron microscope.

No real acceleration

The chart makes it clear that there is no real sense of acceleration in EMU money or credit growth in terms of year-over-year growth rates. Shorter period growth rates from 12-month to six-month to three-month (presented in the table) show a steady deceleration in credit growth with private sector credit falling from a 12-month pace of 1.5% to -1.2% (annualized) over three months. Money growth waffles on that sequential timeline, but its 5.1% 12-month pace turns to a 4% annualized pace over three months. If the ECB is looking for signs of revival, it is better off looking up an old play on Broadway that ferreting through these data.

Real balances offer little hope

Real balances (the same aggregates deflated by the HICP) show that credit has slowed and is contracting over three months in real terms. Price-deflated money supply shows steadier growth with a slightly higher three-month growth rate of 4% compared to its 12-month pace of 3.8%. Still, this is very thin gruel for good news.

Moderate steady growth in most monetary centers

Globally money growth is mostly stable

Globally money growth is mostly stable

Money growth in the United States, the EMU, Japan and the U.K. is for the most part moderate and trendless. The clear exception is the U.K. where post-Brexit vote stimulus is still in train and has led to a much weaker sterling exchange rate and a ramp up of money growth. U.K. inflation is up too but mostly on import prices. U.K. real money balances actually show weakening growth over three months (2.2% pace) compared to 12 months (4.2% pace). In the U.S., real balances are growing marginally faster over three months than over 12 months; in Japan, real M2 plus CDs is slightly weaker. Nominal money growth is weaker over three months than 12 months everywhere.

The chart on year-over-year money growth gives a slightly different and much longer perspective. U.S. money growth has been and continues to be broadly stable at pace around and just above 5% and has been like that since late 2013. EMU money growth has risen in the recovery period but peaked in 2015 and since then has decelerated to flatten out at a pace centering on 5%. Japan's M2 plus CDs measure shows the gradual and consistent pick up with an acceleration that is so mild I hesitate to call it 'acceleration.' U.K. money supply has had wild fluctuations. It was the most erratic and fastest growing money supply before the global recession and it became the weakest and still the most volatile in the recovery period as well. The added BOE stimulus post-Brexit vote has sent U.K. money supply on yet another adventure. It is showing some signs of slowing but nothing that is terribly reliable.

The same old global scenery is still on stage

On balance, the global money supply data do not point to any real changes in progress in the monetary sector. In EMU both money and credit display benign growth rates. Central banks are eager to hike rates as though their business cycle alarm clocks are buzzing. And the Fed's business cycle alarm clock is buzzing so loud it is waking up Mario Draghi! Meanwhile, these are the same bankers that caution us that business cycles don't simply die because of old age. These very same central bankers that seem to be getting restless like children in the back seat of car asking "Mommy, when are we going to get there?" No one knows when we are going to 'get there.' Neither are bankers even sure where 'there' is located. But they are as nervous as a cat on a hot tin roof about how long they have kept rates this low. And even though inflation is not rising, central banks are either looking (plotting, scheming) to hike rates or are already doing it as the Fed in the U.S. is. The Federal Reserve in its meeting yesterday even gave clearer language (but still manage an obscure reference) to its timing by saying it would begin to shrink its balance sheet 'relatively soon' replacing language from the previous meeting that referred to 'this year.' The Fed continues to play the game of horseshoes and hand-grenades with its verbiage. It wants us to know that it is now committed to balance sheet shrinkage but not committed to a specific time, but hey, it has a cohort of time corralled -depending on circumstances, of course. Does that sort of communication really help?

The great (or not-so-great) transition

Language-fiddling by the Fed is unproductive. And the ECB is being drawn into the same trap. If you have planned an event and have something to say, then say it. The Fed always tells us it is data dependent; even its balance sheet communication refers to how its actions depend on the economy. If so, what is the point of this titillating over-staged yet hedged balance sheet 'promise?' Does the Fed think it is keeping congressional critics off its back by letting them know that it is going to get 'there?' I certainly 'don't get it.' As a policy I don't like it; nor do I agree with it. Balance sheet reduction was supposed to wait until Fed funds normalization was well under way (see the Fed's May FOMC statement). Is it? Is it 'well under way' or, well, is it underway? Now the balance sheet 'action phrasing' that once was conditioned by the path of the fed funds rate is replaced by this language of 'subjunctive certainty' on the event with boxed in prevarication over the timing. No that's not a 'typo.' I do mean 'subjunctive certainty' and 'boxed in prevarication.' What a mess. We are definitely transitioning out of the period when central banks are giving us leadership. Are we transitioning into a period in which they will try their darnedest to confuse the heck out of us? What ever happened to the revered 'one if by land, two if by sea?' At least that was easy to understand.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief