Global| Jun 28 2017

Global| Jun 28 2017EMU Money and Credit Growth Inspire Little Confidence; Global Trends Show Some Improvement But Offer Little [...]

Summary

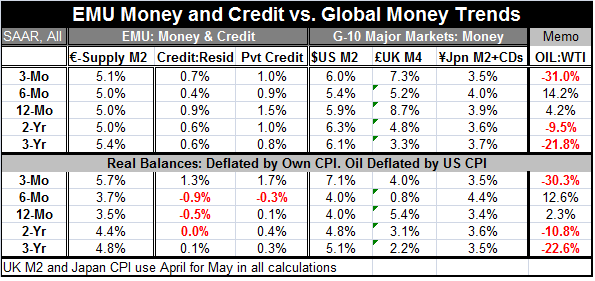

The year-on-year growth rates of money and credit in the EMU (loans to the private sector) show a leveling off of money growth at the 4.5% to 5% mark with recent growth perhaps creeping up at a pace of 1 to 1.5%. Mario Draghi has [...]

The year-on-year growth rates of money and credit in the EMU (loans to the private sector) show a leveling off of money growth at the 4.5% to 5% mark with recent growth perhaps creeping up at a pace of 1 to 1.5%.

Mario Draghi has recently described the situation in the EMU as one in which the forces of deflation have been replaced by forces accentuating growth. But Draghi has also maintained that accommodative policies will still be needed. Today European Central Bank Vice President Vitor Constancio noted that there may be more slack in the economy than the ECB thinks and that policy should pay close attention to the development of inflation relative to its target.

Globally, U.K. money supply is surging; elsewhere, money supplies show flat or fading growth clustered around the 5% mark. And that would be more than plenty of monetary fuel to allow 2% growth and 2% inflation, except that monetary velocity is pulling back meaning that that kind of money growth is barely sufficient...for now in this environment. CPI growth shows inflation at 1.4% (as of May) in the EMU, at a 2.9% pace in the U.K., at 1.9% in the U.S., and at 0.4% in Japan. Inflation is accelerating over 12 months compared to the previous 12 months in all of these regions. The acceleration is around 1% in the U.S. and Japan and 1.4% in the EMU and 2.6% in the U.K. Of course, this comes in the wake of the oil price crash, recovery and relapse into weakness. All bets are now off in terms of where inflation is or where it goes next and how fast, until OPEC gets its ducks in order. Inflation forecasting is for now a game of chance.

In the EMU, there is the question of getting durable growth started even though the central bank mandate is only about inflation. The EMU HICP was last at or above 2% in January 2013, marking a long period of inflation undershooting. As oil prices rise, Draghi has talked more of looking at the performance of core inflation to see if underlying inflation is really being boosted to target, a sensible tilt given the circumstances.

In Japan, inflation is simply undershooting as it has for so long. For much of last year, from March through September 2016, the price level was still dropping, but that was after a period of some price increases. Japan's experience with true deflation ended early in 2013, but Japan has been unable to instill an environment of steady inflation at its policy target of around 2% against a background of policy shocks and a now-shrinking population.

In the U.K., the weak pound and a jolt of post Brexit vote monetary stimulus has boosted inflation and money growth. The Bank of England is split on what to do but has held off reducing its stimulus. Governor Mark Carney asserts that the time is not right to hike rates. That sentiment was endorsed today by Deputy Governor Jon Cunliffe. While monetary stimulus seems excessive in the U.K. as fast growing money supply, rising and too-strong inflation and a weak pound all attest to. But Brexit is bringing a negative real shock to the table. Carney front-loaded stimulus with that in mind. High-paying financial firms have been announcing moves out of London for various segments of their staff. The question is whether it makes sense to micro manage monetary policy ahead of the real shock to deal with a temporary inflation overshoot that is about to be overwhelmed by a negative shock especially in an environment where wages are not following prices higher. The BOE is holding its ground for now, but monetary policy committee members are of two minds on this issue with apparently strong sentiments on either side of the argument. The clash of minds at the BOE is not going to go away quickly.

In the U.S., inflation is falling again after rising and it is even lower on the central bank's targeted inflation gauge (PCE). Clearly oil has been responsible for most of the inflation increases we have seen recently. With oil prices swooning again, the outlook for inflation and policy has become murky.

The ECB seems to be preparing to dismantle some of its easing mechanisms. The BOE has infighting over whether to shift gears or not. Even in Japan without much real success on meeting its inflation goal, there is some unrest with the long period of deep stimulus. In the U.S., the Fed is already down the road and tightening and also is planning to shrink its balance sheet to withdraw some of its 'unconventional stimulus.' The IMF today cuts its outlook for growth in the U.S., citing new uncertainties over the implementation of U.S. fiscal policy measures. The path to normalcy remains a treacherous one with little that can be taken for granted. I would compare the way forward to the way one would very carefully walk through a mine field- no running, no rushing, plenty of looking before taking the 'next step.'

On balance, the situation for global growth and monetary policy is in a 'better place' than it was a year ago, but Draghi's warning seems fully apropos to the global situation. There is no strength here, but the outright negative forces seem to have abated. Yet, inflation expectations are still tightly corralled and may even be too-tightly corralled. The various monetary jurisdictions will have to make the right choices for their countries or regions. Monetary policy still seems to be on a high wire. While central bankers are schooled to protect against inflation, it is still not clear that inflation is the greater risk here.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief