Global| Jun 26 2020

Global| Jun 26 2020EMU Money and Credit Finally Accelerate But So Does Corona...

Summary

Stimulus polices in the EMU have finally taken hold among financial variables and both money and credit measures are growing faster- much faster. Will actual economic stimulus result from this? EMU money supply (M2) has progressed [...]

Stimulus polices in the EMU have finally taken hold among financial variables and both money and credit measures are growing faster- much faster. Will actual economic stimulus result from this?

Stimulus polices in the EMU have finally taken hold among financial variables and both money and credit measures are growing faster- much faster. Will actual economic stimulus result from this?

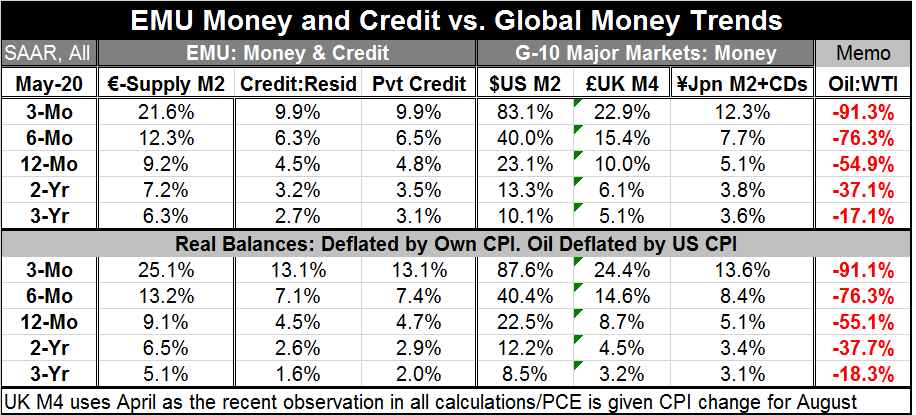

EMU money supply (M2) has progressed from average growth of 6.3% over three years to 7.2% over two years to 9.2% over 12 months; M2 is growing at an annualized pace of 21.6% over three months. Similarly, the growth in real money balances has progressed and expanded sharply as well.

Residential and private growth rates for credit to residents and to the private sector also have stepped up. Nominal credit growth is on the verge of double-digit growth rates when annualized over three months. Year-on-year credit growth is just under 5%, but it has moved up sharply (see graphic).

Globally money supply growth has been strong as well. The U.S., the U.K. and Japan have been doling out heavy servings of monetary stimulus. Yes, interest rates everywhere are near zero and annualized money growth over three months is at 83% in the U.S., 23% in the U.K. and 12% in Japan. Over three months, oil prices are falling at a 91% annual rate. The exceptional growth in the U.S. money supply gives you some idea of how great the demand for dollar financing has been.

And economies that had been in a lockdown mode are beginning to come back on stream. That will breathe more life into economic data and at least for a while make credit stimulus look like it worked. But did it really? Will it really?

This has been an usual economic time. The economic lockdowns have destroyed economic activity and income growth. In the absence of the normal channels of economic and financial activity, the State stepped in with various stimulus in various countries. There has been fiscal as well as monetary action and a much smaller contribution to income generation for the private sector. And increases in debt have been inevitable. The bulge in money supply was predictable after all these actions. However, the effectiveness of the actions is still unclear.

Countries are still in the grip of the coronavirus. And as long as that is true, the prospect of economic growth is going to depend on the state of the spread of the virus, the actions of the local public health officials and the confidence of the public. Putting bank reserves and fiscal spending and lending into an economy that is under lockdown protocol is only going to keep things on an even keel at best and only for a while. Unless the virus is controlled and the private sector is opened up, the prospects for growth will remain poor.

Of course, the global economy is right now in the midst of an unlocking, but the unlocking is coming with a new surge in infections in China, Europe and the U.S. WHO has issues another set of warnings. In the U.S., some states are seeing local lockdowns re-imposed. Europe is also seeing backsliding.

There is no viable strategy to deal with the virus. 'Science' offers two alternatives: one is to gain herd immunity the other is to pray for a viable, safe vaccine. Only herd immunity offers a sure solution, but globally only Sweden has opted for a path that might take it there. Everyone else uses lockdowns when the virus flares and they work to slow its progression but at great economic costs. And then when there is a reopening, the infection rate and derived immunity of the local community is scant and the community is again vulnerable to reinfection. The cycle of infection, lockdown, reopening and reinfection...etc could go on and on. This strategy is not a long-run solution and it is a protocol that will prove to be economically very damaging.

Since we have only completed the first lockdown and are only seeing our first experience of a second wave, or a relapse, or reinfection, or whatever you want to call it, the futility of this process is not yet widely appreciated. But the lockdown strategy is only make-shift and it does not save lives in the long run unless it is paired with a real workable vaccine- and the development of vaccine is wholly speculative.

Economic policy and stimulus can only take us so far. And in the economy whatever is done on the fiscal and monetary fronts will have consequences that will have to be dealt with later. Of course, in an emergency, you do what you can. But this is a case in which a real long-term solution is being left to the speculative vagaries of discovering a vaccine. And no one should be reassured by that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief