Global| Jun 02 2008

Global| Jun 02 2008EMU MFG Weakens but Pace of Decline Slows

Summary

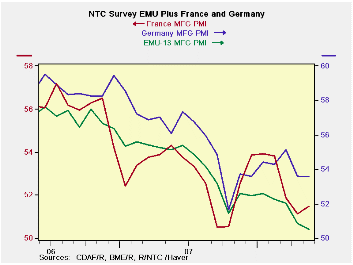

Manufacturing output weakened slightly in the Euro Area in May but the pace of decline is slowing. Among reporting countries the MFG PMIs mostly slipped in May. France and the Netherlands were exceptions, the Netherlands in the most [...]

Manufacturing output weakened slightly in the Euro Area in May but the pace of decline is slowing. Among reporting countries the MFG PMIs mostly slipped in May. France and the Netherlands were exceptions, the Netherlands in the most trivial of ways.

Spain remains the mostly serious impacted of EMU countries with its MFG PMI in the bottom 2.5% of range constructed from early 2000 on. The overall EMU PMI is below breakeven at the 43.7 range percentile. France, Italy and Austria, too, are below their respective range midpoints. Germany’s standing at the 61.2 percentile of its range is astonishing. The UK, an EU only member, stands in the 42 percentile of its range.

For the most part these rankings reflect inflation rankings and therefore reflect competitiveness rankings within the EMU area. Greece, however, is performing in terms of its MFG PMI much better than its inflation ranking would have you believe it would. The rest fall more or less into line. (see inflation chart below for cumulative inflation on the national HICPs since July 2000).

The table shows that German inflation has risen by 4.4 percentage points less than EMU inflation during their period. Greece’s HICP has risen by 11.5% more than the EMU average. Spain is also an inflation leader and as expected it is an output laggard in this cycle as the euro has risen.>

On balance there is a great deal of irregularity within the

Euro Area involving inflation performance and output results. Still

there is only one monetary policy, making things difficult. The ECB is

looking only at group inflation (EMU-wide) to make policy and holding

to a firm path. Cracks in the Euro Area are beginning to form.

| NTC MFG Indices | |||||||

|---|---|---|---|---|---|---|---|

| May-08 | Apr-08 | Mar-08 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 50.60 | 50.74 | 52.03 | 51.12 | 51.84 | 52.78 | 43.7% |

| Germany | 53.57 | 53.62 | 55.14 | 54.11 | 54.11 | 54.58 | 61.2% |

| France | 51.48 | 51.12 | 51.88 | 51.49 | 52.68 | 52.44 | 41.5% |

| Italy | 48.05 | 48.24 | 49.41 | 48.57 | 49.65 | 51.16 | 29.5% |

| Spain | 43.79 | 45.19 | 46.42 | 45.13 | 46.90 | 49.41 | 2.5% |

| Austria | 49.76 | 49.83 | 53.39 | 50.99 | 52.11 | 53.14 | 41.4% |

| Greece | 53.77 | 54.38 | 52.73 | 53.63 | 52.89 | 53.48 | 52.7% |

| Netherlands | 51.46 | 51.45 | 53.15 | 52.02 | 52.58 | 54.64 | 51.7% |

| EU | |||||||

| UK | 50.03 | 50.81 | 51.14 | 50.66 | 51.02 | 52.76 | 42.1% |

| Percentile is over range since March 2000 | |||||||

| Trouble in the Zone? | ||

|---|---|---|

| Jul-00 | Gap | |

| HICP | Apr-08 | W/EMU |

| Austria | 17.1% | -2.4% |

| France | 17.7% | -1.8% |

| Germany | 15.1% | -4.4% |

| Greece | 31.0% | 11.5% |

| Italy | 20.8% | 1.3% |

| The Netherlands | 20.3% | 0.8% |

| Spain | 28.3% | 8.8% |

| EMU Total | 19.5% | |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief