Global| Dec 14 2009

Global| Dec 14 2009EMU MFG Progress Hits The Skids.... More Questions Arise In Japan Despite Improved Tankan

Summary

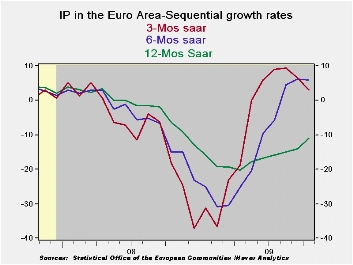

Industrial output in EMU has backtracked. The 0.3% drop in October flattens out progress in the sector and leaves manufacturing IP flat in the fourth quarter compared to its level in Q3. Consumer goods output is off sharply in the new [...]

Industrial output in EMU has backtracked. The 0.3% drop in October flattens out progress in the sector and leaves manufacturing IP flat in the fourth quarter compared to its level in Q3. Consumer goods output is off sharply in the new quarter while capital goods output is strongly higher. Intermediate goods output is up sharply.

Among the five largest EU economics only Spain saw a rise in IP month-to-month in October. Still three month growth rates are up for the zone and are strong for the Big Five except for a 1.8% annual rate drop in the UK and a horrific-looking -20.2% from Spain whose numbers are notoriously volatile (Spain’s three month growth rate for IP was UP by 28% in Sept, just one month ago).

Japan’s TankanIn Asia Japan has reported out its Tankan results for December. Its large company index rose by a solid nine points and exceeded the forecasts of economists. Still at a raw reading of -24 it clearly says that large corporate respondents are still more negative than positive in this Tankan diffusion presentation. Even if they are less negative than they were last quarter the results are far from satisfying. Firms in Japan are engaging in deeper spending cuts to stay alive in a still-tough economy. Japan has slipped back into the grip of deflation something that tends to make businessmen more defense-minded- that is not the way to mount a recovery. With the yen still so strong it is hard for Japan to export itself to prosperity. Paradoxically Japanese firms continue to engage in outsourcing with Sony making a new announcement to that effect transferring work to China. While outsourcing may solve the firm’s problems it does not help Japan out of its economic difficulties.

The global recoveryOn balance world trade is making some recovery and that is helping trade-dependent countries like Japan to do better. But Japan is still beset with problems and large block of pubic indebtedness that keeps its government from engaging in too much in the way of pump-priming expenditures. Europe is having a simple slip but its broader growth rates tell a story of slowing that transcends one monthly report. When central bankers and national leaders say that they are still concerned about the economy and that there is a risk of backsliding and that it is too soon to take away the special stimulus brought forward in the crisis… this is the sort of report that brings those concerns to life.

Treatment of the heroes of the crisisAgainst this background we have to wonder about the all the flack being shoveled onto Fed Chairman Ben Bernanke’s plate. Bernanke’s efforts bolstered not just the US, but the world economy. Do the Fed bashers on the House and Senate banking committees really have any idea what they are protesting when they go after Gentile Ben? It was the fall in standards and directions imposed on markets by the law makers who put political agendas ahead of smart business practices as much as anything that got us into this mess. Now we can see that despite huge government and central banker efforts around the world the path to recovery remains tentative. The US Congress is deeply involved in a witch hunt for scapegoats. The Fed Chairman is a more convenient a target than he is to blame. But with an angry electorate in the US and the next election cycle looming a scapegoat is a prime need for politicians.

| EURO-AREA MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Oct-09 | Sep-09 | Oct-09 | Sep-09 | Oct-09 | Sep-09 | |||

| Euro-Area Detail | Oct-09 | Sep-09 | Aug-09 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo | Q-4 |

| MFG | -0.3% | 0.3% | 0.3% | 1.3% | 2.5% | 1.4% | 0.6% | -12.1% | -13.7% | 0.0% |

| Consumer | -1.7% | 0.1% | -0.5% | -8.3% | -0.2% | -3.5% | 0.6% | -5.4% | -3.7% | -10.5% |

| C-Durables | -1.4% | -5.1% | 5.1% | -6.3% | 1.3% | -12.9% | -9.2% | -18.0% | -18.2% | -- |

| C-Non-durables | -1.6% | 0.7% | -1.2% | -8.1% | -0.6% | -2.2% | 1.9% | -3.3% | -1.5% | -- |

| Intermediate | 1.2% | 1.0% | 1.1% | 13.7% | 15.4% | 15.6% | 12.6% | -12.8% | -16.0% | 13.9% |

| Capital | 0.0% | 1.5% | 1.6% | 12.8% | 6.9% | 6.2% | 3.4% | -16.8% | -18.7% | 9.3% |

| Main Euro-Area Countries and UK IP in MFG | ||||||||||

| Mo/Mo | Oct-09 | Sep-09 | Oct-09 | Sep-09 | Oct-09 | Sep-09 | ||||

| MFG Only | Oct-09 | Sep-09 | Aug-09 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo | Q:4-Date |

| Germany: | -1.6% | 3.7% | 2.1% | 17.6% | 20.8% | 19.1% | 16.1% | -13.5% | -13.9% | 9.0% |

| France:IPxConstruct'n | -0.8% | -1.2% | 3.0% | 3.7% | 9.0% | 7.9% | 6.6% | -8.4% | -10.6% | -3.8% |

| Italy | 0.8% | -5.4% | 6.0% | 4.4% | 6.0% | 4.4% | 4.0% | -13.7% | -16.5% | -5.8% |

| Spain | -3.0% | 0.5% | -3.0% | -20.2% | 28.0% | -0.2% | 19.0% | -13.0% | -12.6% | -20.4% |

| UK: EU member | 0.0% | 1.6% | -2.0% | -1.8% | 0.5% | -0.4% | -0.4% | -7.8% | -9.8% | 2.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief