Global| Feb 02 2015

Global| Feb 02 2015EMU Mfg PMIs Rise in January on 'Small Country' Strength

Summary

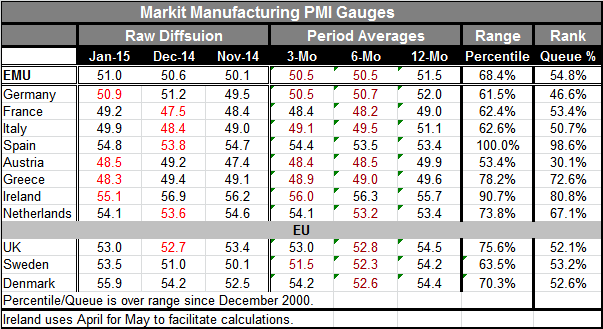

Even with the manufacturing PMI rebound for the EMU in January, the broad brush shows PMI averages over shorter periods are still declining. France is a minor exception. Spain is accelerating and is a major exception (fourth largest [...]

Even with the manufacturing PMI rebound for the EMU in January, the broad brush shows PMI averages over shorter periods are still declining. France is a minor exception. Spain is accelerating and is a major exception (fourth largest EMU member!). The Netherlands is an exception. Ireland is net weaker over three months compared to six months. Greece, Austria, Italy France, Germany and the overall EMU each show three-month averages below their 12-month averages. Only Spain is stronger over its three-month than over its 12-month average by one point or more. Relative strength is a low hurdle in the EMU.

Even with the manufacturing PMI rebound for the EMU in January, the broad brush shows PMI averages over shorter periods are still declining. France is a minor exception. Spain is accelerating and is a major exception (fourth largest EMU member!). The Netherlands is an exception. Ireland is net weaker over three months compared to six months. Greece, Austria, Italy France, Germany and the overall EMU each show three-month averages below their 12-month averages. Only Spain is stronger over its three-month than over its 12-month average by one point or more. Relative strength is a low hurdle in the EMU.

The queue standings show Spain at a raw score of 54.8 in its 98th queue percentile. Ireland at a raw score of 55.1 has a standing in its 80th percentile. Greece with a raw score showing a decline at 48.3, nonetheless, shows a queue standing in its 72nd percentile. Perhaps Greece is an example of the expression, "Been down so long it looks like up to me."

The Big Three EMU members are disappointing one way or another as the German raw manufacturing score of 50.9 has a weak 46.6 queue percentile standing. France and Italy each have raw diffusion scores, showing shrinkage with France's standing in its 53rd queue percentile and Italy's in its 50th queue percentile. This month whatever strength there is resides outside the three biggest members.

Outside the EMU space, Sweden is decelerating while the UK and Denmark are prevaricating. All three have 12-month PMI averages in the 54th percentile range, however.

China's official manufacturing PMI slipped below the breakeven 50 mark in January. That adds to some of the gloom over economic prospects. Not surprisingly, Russia's PMI also fell and is quite weak as sanctions are weighing it down. Its renewed activities (which it denies) in Ukraine do not make the Russian outlook any better.

However, the plot of EMU and U.K. PMIs shows that there is stabilization taking place. This could be a very important development ahead of the start of QE. If QE can launch in a stable environment, instead of one that is deteriorating, its chances of success are better. Of course, there is still price deterioration and yield deterioration and growth, while stable in some aggregates, is still quite uneven and distinctive by EMU members. But at least there are some ways of looking at Europe in which its ills do not look uniformly bad.

The euro exchange rate continues to weaken and has dropped below its `equilibrium' or PPP value on my assessment of that metric. This means it is now undervalued based on EMU averages. Member by member there will be differences on this score because members have had unique inflation experiences. At this exchange rate, Germany will be exceptionally competitive while countries in Southern Europe where inflation has been much higher may not benefit as much. Having said that, Spain is faring quite well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief