Global| Sep 10 2013

Global| Sep 10 2013EMU Members' IP Falters

Summary

Despite numerous upbeat reports including the Markit purchasing manager surveys and leading indicators from the Organization of Economic Cooperation and Development (OECD) many countries of the European Monetary Union are backsliding [...]

Despite numerous upbeat reports including the Markit purchasing manager surveys and leading indicators from the Organization of Economic Cooperation and Development (OECD) many countries of the European Monetary Union are backsliding and showing declines in industrial production in July as well as more broadly.

Despite numerous upbeat reports including the Markit purchasing manager surveys and leading indicators from the Organization of Economic Cooperation and Development (OECD) many countries of the European Monetary Union are backsliding and showing declines in industrial production in July as well as more broadly.

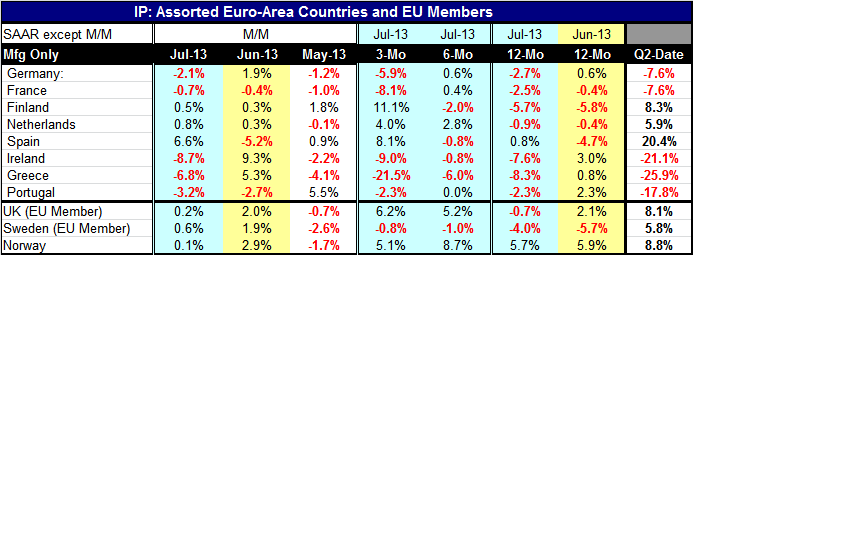

Of the eight countries reporting in July, five of them show month-to-month declines in industrial output. Five of them show declines in industrial output over three months. Four of them show declines industrial output over six months. Seven of the eight show declines in industrial production over 12 months. That is irregular and halting improvement at best.

In the unfolding quarter-to-date comparisons, five of the eight economies are showing declines in industrial production in the new quarter, as well. That calculation takes the level of the IP index in current month and calculates its growth rate over the second quarter base, annualizing it. Measured on this basis, Ireland, Greece and Portugal are putting in double-digit declines at an annual rate, early in Q3. Both France and Germany are posting declines and at a 7.6% annual rate. Spain is showing strength, but for Spain `outsized changes' are almost always do the volatility as the July growth in IP is up 6.6% following a 5.2% decline in June. It's always good to be wary when you are looking at short term growth rates for Spain. On the same Quarter-to-date horizon, Finland shows an 8.3% annual rate of growth while the Netherlands shows a 5.9% annual rate of growth.

Looking at growth progressions from 12 months to six months to three months, Germany and France show very clear deceleration (that's right, not acceleration) along with Ireland and Greece. Portugal shows lingering weakness with a -2.3% year-over-year growth rate, 0% over 6 months, and -2.3% over three months. Spain shows a sharp pop over three months but that's after 0.8% year-over-year and -0.8% over six months - possibly there is something in the making with Spain, but more likely it's just the timing of the volatility on these particular calculations. The Netherlands shows signs of really making progress as its growth rate goes from -0.9% over 12 months up to 2.8% over six months to 4% over three months. It's not an exceptionally strong progression, but it is a clear progression. Finland also shows a pretty clear progression from -5.7% over 12 months to -2% over six months to a very strong +11.1% over three months Finland is the only EMU member with industrial output increasing for three consecutive months (the Dutch come close).

The United Kingdom, which is not in the single currency area, also shows clear acceleration and growth; it logs an 8.1% annual rate increase in the quarter-to-date. Sweden shows improvement in the sense that its sequential growth rates are declining by less from 12 months to six months to three months. That trend culminates in a positive 5.8% growth rate for the current month over the previous quarter. Norway shows less in the way of acceleration but displays persistent growth. It's the only country in the table with positive growth rates over three months, six months and 12 months; it's showing an 8.8% annual rate gain over the previous quarter.

There are some rather disparate trends in the Eurozone at the moment. The tangles that we get from these growth rates offer a substantially different picture than the one that we get from the profile of their PMI manufacturing indices. Part of this is because the manufacturing PMI indices are also a mixture of indicators showing growth and declines even as most of them are moving up, to higher PMI values. One of the main messages in the PMIs is that, (1) either growth is improving or, (2) that the declines are dissipating. But even that message is muddied by the current trends in industrial output across EMU members. Diffusion indexes can only tell you so much.

Segue to Other Trends: Beyond EMU

While there are number of reports and indicators as well as emerging global trends that embrace the positive `spin du jour,' we continue to be wary of the fundamentals in the Monetary Union which still are not very good and are built on potentially still-shifting sands. The recent data reports in the US reveal a sequentially less solid looking economy there, too.

I remain somewhat more cautious about the outlook for the US/European/Chinese GLOBAL economies. Perhaps the new events in Syria will blunt the worst of the concerns over what is happening in the Middle East. Perhaps the new move to head off military action will eventually fail. I don't think that what happens in the Middle East dictates the tune for growth, but it does matter.

In the US there is some evidence - despite the slowdown from some recent economic indicators - that recovery actually might be taking root and spreading. What I have observed is this: at least in the car market, there is evidence of loans being made to a lower credit-worthy caste of borrowers. But, in the housing market with mortgage rates going up there is no evidence of that trend taking root\.

Still, US credit growth is expanding, but it doesn't seem to be accelerating. The slowdown in job growth dovetails with some recent reports on consumer attitudes that conversely raise some warning flags. Is the US re-entering the woods?

After this extended and anemic economic recovery, we continue to have central banks playing very large roles in various national economies and, for the most part, the fiscal authorities haven't figured out what they can do. Or, if they have figured it out, they have also figured out that doing the right thing is not going to be good for their political careers. The right fiscal actions continue to lag behind needs, but the various economies have still been able to show growth. In the US the Fed is still poised to pull the trigger to start pulling back on its program of quantitative easing -even in this fragile environment. We would be foolish not to wonder what happens next.

Putting aside the prospects for international growth, we have to be worried about what's going on with international relations. When an evil leader whose country signed the Geneva Convention can gas people in his own country and come away from it without any international condemnation that's not exactly a step forward for global governance. The world economy is becoming increasingly interrelated. If our common values don't include abhorrence of the use of chemical weapons, what are we ever going to be able to agree on in the economic and geopolitical areas where we have common interests combined with plenty of conflict?

The fact that the US and Russia were not able to figure out a way to solve their differences over this clear breach of the Geneva Convention does not bode well for the future. The new proposal to allow Syria (which means Assad) to cash-in and get a `get-out-of-jail-free' card for putting his chemical weapons in the hands of an international agency is not really an answer. It may reduce the likelihood that Assad can ever do this again; but since we don't know what he really has, we will never really know if he has turned it all over or not. Secondly, so far as we know, this approach lets Assad off scot-free for what he did. Those are significant drawbacks to the current proposal that apparently was launched inadvertently by the US President himself and has been put forward as an actual proposal by the French and is now endorsed by Russia, China and Iran and apparently accepted by Syria (in some form). The devil is always in the details, but on the face of it, this proposal leaves a lot undone. There should be a lesson in that. I hope that we can see it before we have to learn it firsthand.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief