Global| Sep 10 2019

Global| Sep 10 2019EMU Member IP Declines Become Rarer in July- Does That Mean Something?

Summary

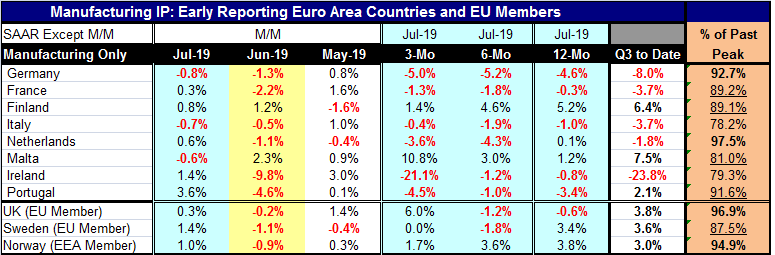

Manufacturing industrial production shows limited declines in July with only three of the early European reports showing drops (Germany, Italy and tiny Malta). However, there is not enough here to suggest that the period of weakness [...]

Manufacturing industrial production shows limited declines in July with only three of the early European reports showing drops (Germany, Italy and tiny Malta). However, there is not enough here to suggest that the period of weakness is over or even that conditions are not getting worse. Economic data simply unfold in a manner that is too stochastic to tell from monthly data.

Manufacturing industrial production shows limited declines in July with only three of the early European reports showing drops (Germany, Italy and tiny Malta). However, there is not enough here to suggest that the period of weakness is over or even that conditions are not getting worse. Economic data simply unfold in a manner that is too stochastic to tell from monthly data.

As you know, any two points determine a trend and with only one point the sky is the limit. However, one reason for a better-behaved July might be that June was so poorly behaved with output declining in 9 of the 11 countries’ IP listed in the table.

Over three months, there are declines is six of eight EMU reporters. The same is true for six months with year-over-year changes showing five declines for the group. The three non-EMU countries in the table (the United Kingdom, Sweden, and Norway) show no declines over three months, two declines over six months and only one output decline over 12 months.

All in all manufacturing is still struggling. Five of eight EMU nations show IP is a declining phase early in Q3 (see Q3-to-date column in the table for the progress of growth on a quarter-to-date basis). The Q3-to-date column analyzes growth in the unfolding quarter by positioning the output index and compounding the growth in July relative to the Q2 base value for each country. This method involves no projections; it just looks at topical momentum. The early Q3 growth rates are all over the map with some very large declining tends and also some quite strong increasing tends. The non-EMU countries are showing consistent solid gains on growth rates ranking from 3% to 3.8%.

Looking at output levels as a percentage of past output peaks shows the least slack in the Netherlands at a ratio of 97.5%. Of course, there has been a long expansion here and plenty of time for new investment to have been made so these calculations are only rough assessments of performance. Still, nowhere does capacity seem under any strain. Among EU members only Germany and Portugal have readings below 90% and 95%. France and Finland are just outside the 90% standing. Italy, Malta and Ireland are in the 78% to 80% range that would still suggest a lot of slack available. Clearly, these three countries are lagging behind the recovery of the rest of the EMU.

Non-EMU countries have done better in general than EMU members in terms of recovering to past peak levels of industrial performance. The U.K. and Norway have IP levels close to or above the 95% mark while Sweden has an 87% ratio to past peak output for current IP. While some clubs like to brag that membership has its privileges, for this club it looks more like membership has had its costs.

Are Italy and France struggling to achieve growth or will there be a relapse of weakness?

Road ahead

All of Europe is looking to the ECB to see what sort of rabbit it can pull out its hat as it prepares to announce its stimulus plan this week. There is also some focus on Japan with the view being that with the U.S. started on an easing program and Europe joining in Japan may feel pressure to join that club. Beyond doing ‘something’ there is still considerable skepticism that whatever is done will not have much effect. Mario Draghi is not pledging ‘whatever it takes’ for this round. In fact, ‘this round’ finds a lot more skeptics about doing it let alone about what to do. In the U.S., a number of FOMC members think that no further stimulus is the right move while there is at least one new advocate for a 50-bp rate cut. The Fed is like the story of the blind men feeling the elephant then trying to describe it. Some think that the economy needs a boost, some think it does not, some want to boost inflation to target, some want the Fed to bring the fed funds rate in line with market rates and others think that an insurance cut might be appropriate. It’s a carnival of reasons step right up and make your choice.

In Europe, options are more limited than in the U.S. with negative rates already prevailing. Interestingly, the German 30-year today briefly skipped above a positive yield level as the Germans are considering a work around their very strict debt laws. Some in Germany see these very low rates as an opportunity to fund infrastructure projects and to engage in some environmental investment. They are considering a back door for stimulus to pursue those long-run objectives and lock up some very favorable financing rates. More debt would helpful too, since the ECB finds adequate collateral for funds injections limited. The ECB is expected to launch a new lending program. In short, everyone is focused on this even though few think it is really be a game changer.

Such are the circumstances of central bankers. Once these all powerful denizens of money roamed the markets with impunity. Bond trades that spoke their language were deemed ‘masters of the universe.’ Now bond trading units globally are being eviscerated and masters of the universe are becoming more universally unemployed. Low inflation is doing its job to reallocate resources globally. Hopefully this does not mean YOU. Hopefully the ECB will find some niche in which its policies can be effective. And hopefully the Fed will choose the correct next policy step. As always, hope springs eternal and infernal. Be careful what you hope for. Central banks got their wish for price stability and now it is nearly killing them.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief