Global| Jul 01 2014

Global| Jul 01 2014EMU Manufacturing PMIs Turn Lower in June

Summary

The chart on the left makes it quite clear that manufacturing in the euro area has turned lower, according to the Markit manufacturing PMIs. France, after lingering behind Germany and the EMU totals, surged to its cycle high two [...]

The chart on the left makes it quite clear that manufacturing in the euro area has turned lower, according to the Markit manufacturing PMIs. France, after lingering behind Germany and the EMU totals, surged to its cycle high two months ago but has fallen from that very sharply and now shows the weakest PMI reading of this group. France has been struggling throughout the recovery. It continues to struggle more than the average EMU member.

The chart on the left makes it quite clear that manufacturing in the euro area has turned lower, according to the Markit manufacturing PMIs. France, after lingering behind Germany and the EMU totals, surged to its cycle high two months ago but has fallen from that very sharply and now shows the weakest PMI reading of this group. France has been struggling throughout the recovery. It continues to struggle more than the average EMU member.

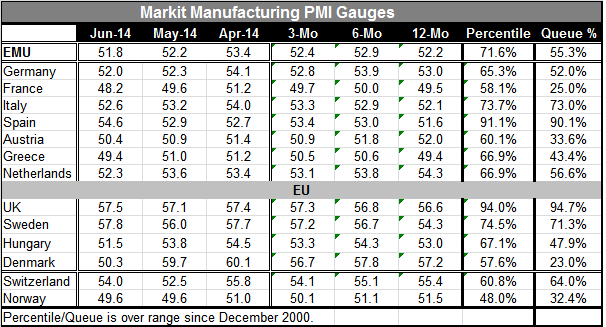

The EMU manufacturing measure slipped from its preliminary reading and now sits at a level of 51.8 in June. At that level the EMU manufacturing gauge sits in the 55th percentile of its historic queue, not a very strong reading. The raw PMI reading shows EMU is only 1.8 points above being neutral. While the queue percentile reading shows us that the queue standing is only 5.3 percentage points above its historic median. In this case, these are equivalent characterizations of how poorly the EMU is doing: barely expanding and only 5% above its median.

The German PMI slipped to 52 in June from 52.3 in May, marking its lowest reading in seven months. German manufacturing is not only of moderate valuation compared to other PMI measures in June, but in the queue sense it is the fourth weakest reading for the EMU members in the table. The German queue standing is in the 52nd percentile, the same value as its raw diffusion reading of 52. However, Italy's raw reading of 52.6 is just above the German raw reading; yet it sits in the 73rd percentile of its historic queue, a much higher standing than for Germany. Remember that the percentile standings are relative measures. What this difference between Italy and Germany tells us is that the German manufacturing PMI is used to being much higher so that at a level of 52, it's considered weak against its historic metrics. But Italy's manufacturing sector is not usually so strong. The level of 52.6 is much stronger when compared with its historic queue.

The strongest queue reading from the EMU countries in the table comes from Spain in the 90.1 percentile of its historic queue. That's followed by Italy in the 73rd percentile and the Netherlands in the 56.6 percentile. Below the Netherlands comes Germany at the 52nd percentile, then Greece at its 43rd percentile, Austria in the 33.6 percentile, and France in the 25th percentile. The French PMI for manufacturing is weaker than its current level of 48.2 only 25% of the time. Clearly France continues to struggle mightily.

Outside of the EMU area, but inside the European Union, we list for members with the UK being the strongest on a manufacturing queue percentile standing in the 94th percentile. It's followed by Sweden in the 71st percentile, Hungary in the 47th percentile, and Denmark in the 23rd percentile.

Returning to the EMU members, eight of the 10 reporting members saw their PMI values reduced in June. Clearly momentum in the euro area has hit a wall of some sort around midyear. We have seen in some of the individual country statistics erode, with the German ZEW and Ifo indices backing off; still, the German consumer confidence gauge from GfK has continued to be elevated.

Europe's labor market data are up to date only through May. The EU shows some further step down in the unemployment rate from 10.4% in April to 10.3% in May. The EMU rate of 11.6% has held for two months in a row. The number unemployed has fallen in May in both the EU and in the EMU areas by 0.2% in each case. Of 11 EMU countries that have reported topical unemployment rates, eight of them show net declines in unemployment over the last three months. Seven of them show unemployment declines over six months and five of them show unemployment declines over 12 months. On a trend basis, unemployment is still falling in the euro area. But the pace of the decline has tapered off. In Germany this month, there's been a slight increase in a number of unemployed even though the German unemployment rate has remained the same at 5.1% for two months running.

One of things that the euro area is trying to deal with is a tremendous degree of variation among its member countries' economic circumstances. Among a group of the 12 oldest EMU members, we find that the standard deviation among the levels of unemployment rates is hovering near an all-time high since the euro area was formed. This measure of disparity within the EU peaked in June of last year and has edged down slightly but not by much. For example, before the financial crisis hit the dispersion among these 12 countries had gotten down to two percentage points while currently it sits above 7.25 percentage points. This is just one measure what the European Central Bank is trying to deal with as it looks across the euro area and tries to set a one-size fits all policy.

So far, the evidence is that the EMU continues to make its progress. Most the labor market information shows that labor market progress continues although it has slowed. However, other indicators don't show such continuing improvement. Moreover, as revealed by the unemployment rate dispersion gauge, the variability of conditions around the union creates the largest headache for the ECB, which is the only agency with overarching macroeconomic abilities to affect conditions in the euro area. Simply put, monetary policy is trying to make progress under the most adverse conditions.

The manufacturing PMIs this month show that progress in the euro area has slowed and even backtracked for a majority of the members. However, the euro area itself still has a manufacturing PMI whose value is 18.2 points higher than its low and only 7.2 points below its past cycle peak. For the four largest economies, it's also true that for all of them, including France, they are higher from their cycle low than they are down from their cycle peak. In most cases, this is a two to one difference although it's much less than that for France.

It has now become a continuing theme to dwell over the weakness in France and to wonder how the euro area is going to move ahead and deal with one of its largest economies that is struggling so greatly. However, even Germany with the best all-around performance has showed some tendency to slow down in the last month or so and to backtrack from its highs. Whatever specific country problems exist, there also seems to be a euro area-wide problem that has been slowing growth. Yet, the IMF is urging central banks to get their base interest rates back to `normal' while the ECB has only just launched a policy meant to provide credit stimulus. Europe is not yet out of the woods.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief