Global| Feb 03 2014

Global| Feb 03 2014EMU Manufacturing PMI Advances Faster Than Industrial Output

Summary

The manufacturing PMI for the European Monetary Union (EMU) in January 2014 rose smartly to a level of 54.0 from 52.7 in December 2013. The index shows widespread increases for the countries in the table. Only three EMU members showed [...]

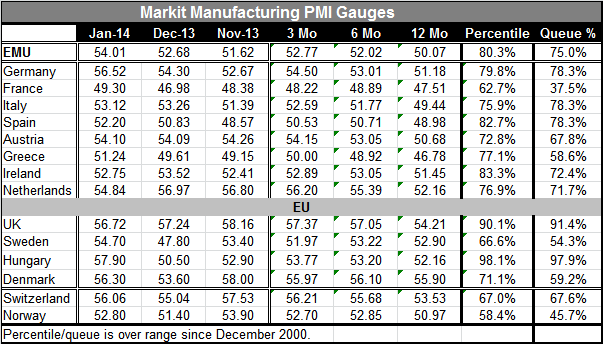

The manufacturing PMI for the European Monetary Union (EMU) in January 2014 rose smartly to a level of 54.0 from 52.7 in December 2013. The index shows widespread increases for the countries in the table. Only three EMU members showed backtracking in their respective indices in January, and only one showed that manufacturing is contracting. The one country in the EMU that is contracting in January is France, the second largest EMU economy. Both the EMU aggregate and the German index are at 32-month highs. Greece has made its first increase in manufacturing in a very long time, 53 months.

The manufacturing PMI for the European Monetary Union (EMU) in January 2014 rose smartly to a level of 54.0 from 52.7 in December 2013. The index shows widespread increases for the countries in the table. Only three EMU members showed backtracking in their respective indices in January, and only one showed that manufacturing is contracting. The one country in the EMU that is contracting in January is France, the second largest EMU economy. Both the EMU aggregate and the German index are at 32-month highs. Greece has made its first increase in manufacturing in a very long time, 53 months.

Some of the recent data from Europe have been of the halting or prevaricating nature. What we see in the January data is that December had been a very difficult month, particularly for European countries not in the monetary union. Of the countries in the table, eight of them saw index declines in December but only two EMU members saw index declines. Both of those posted increases compared to their December values in their January performance. But of the four EU members that are not in the monetary union that we track in the table, all four showed severe declines in December but only three have shown sharp increases in their respective indices in January. The exception is the UK which has now reported its manufacturing PMI lower for two months in a row; but its index level is one of the strongest in Europe. Switzerland and Norway round out our European group of countries; they are neither EU members nor in the EMU. Both of them show sharp declines in December and have showed significant rebounds in January.

Of all the countries in the table, France is the only one whose manufacturing sector is showing a backtracking. The preponderant signal from January is that countries are throwing off the weakness that emerged in December.

Looking at the standing of the current PMI gauges in their historic queues, the overall EMU standing is in its 75th percentile, telling us that it is higher only 25% of the time. Germany stands in the 78th percentile; it is higher only 22% of the time. France is now the dog of this group standing in the 37th percentile, higher 63% of the time.

Among the countries that are not party to the single currency area, experiences are hard to characterize because there is a great deal of variability. Hungry has the highest queue standing of the group as its manufacturing PMI stands in the nearly 98th percentile of its historic queue. The UK remains extremely strong at its 91st percentile. But Denmark is only in the 59th percentile of its historic queue and Sweden in the 54th percentile; both of those marks are below the mark for the EMU as a whole. Switzerland and Norway similarly are dragging behind the EMU's mark as Switzerland's standing is in the 67th percentile and Norway in the 45th percentile of their respective historic queues.

PMIs in Perspective: It is important to recognize that these PMI data derive from diffusion indices that survey companies in manufacturing and ask questions like, "is your output higher or lower or unchanged?" A series of other questions are asked to discern responses for different areas within manufacturing and to form an overall index. According to the lexicon of the diffusion index, values above 50 show expansion while values below 50 show contraction. We have in the chart plotted the overall PMI metric for the EMU against the level of industrial production. That chart shows that the manufacturing PMI is moving up much faster than is the industrial production index for all of the EMU. IP is a well-measured inflation-adjusted index of what is happening to output. Industrial production is making a mild increase, but the PMI gauge is absolutely jumping.

This divergence tells us that while output gains are becoming more widespread (that is what the PMI formally tells us) the gains themselves are not yet particularly strong (that's IP tells us). The PMI gauge, which is actually a gauge about the breadth of the change in MFG (the average change in the various metrics whose surveys makeup the overall PMI), is often taken as a gauge of strength. As you can see from the path of the industrial production level against the PMI index, there is a strong correlation between the level of the PMI and the level of industrial production. But we can see also that there is a difference. Simply put, breadth is not strength. But breadth is often a prelude to strength.

So without being too much of a nitpicker about the PMI gauge, it is still important to keep separate what the index actually tells us and what it doesn't tell us. Diffusion indexes are considered to be quite sensitive. Looking at the chart, you can see that the PMI gauge tends to act early and tends to have exaggerated swings compared to those in industrial production. The signal from the PMI gauge is often early and often correct. That is why we follow these indices, but there has been a long time that the PMI has outperformed industrial output and we know that there are lingering economic difficulties within the euro zone. It might be a good time for us to recognize that industrial production may not jump to follow the trend in the PMI diffusion index and, rather, diffusion may come back to coincide better with a rising but weaker industrial output as it has also done in the past (such as from early- 2011 to late-2011). The PMI sometimes has to `reset' itself.

At this time we don't really know how this is going to work out. But it is a good time for us to look at the divergences between the PMI signal and the measurement in industrial production and to think about what is driving each of them and to make some judgment about which of the signals is likely to be a better judge about what the economy is actually doing.

It is important remember that while the PMI signals are running up strongly, industrial production is lagging. The PMI indices themselves are not yet particularly strong in their respective historic ranges. But they still are strong relative to IP. For all of the EMU, the aggregate PMI index is still higher 75% of the time. The question really is whether manufacturing is truly building a head of steam or not. Manufacturing has been the leading sector in this economic recovery. The services sectors, both in Europe and in the United States, have lagged behind. We have some evidence that in China both manufacturing and services are beginning to lag. It may be that the cyclical forces still are not lining up to create a surge in this recovery, but that doesn't mean recovery won't last.

We urge some perspective in looking at the PMI signals under current circumstances. We also point to the divergence of performance within the euro zone that is something that is likely to continue to hold back a true gathering of strength in the euro zone. The European Central Bank held forth today with a bit more information on the stress tests it intends to run on banks. It is going to try to hold banks to the standard of keeping 5.5% capital under the risk scenarios they are given. It is clear that banks continue to be on a short leash at the ECB, and that is another factor that causes us to be wary of the notion of building acceleration for IP growth or GDP growth in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief