Global| Jun 15 2009

Global| Jun 15 2009EMU Job Market Has Record Q1 Job Loss

Summary

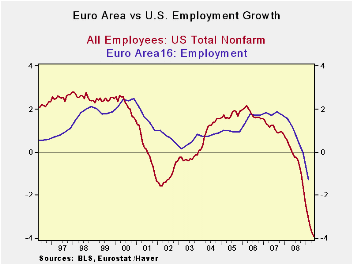

The number of people at work in the Euro Area fell by 1.2mln in Q1, the greatest quarterly drop since records began in 1995. Still, that performance is dwarfed by the huge declines in the US as the percentage calculations in the table [...]

The number of people at work in the Euro Area fell by 1.2mln

in Q1, the greatest quarterly drop since records began in 1995. Still,

that performance is dwarfed by the huge declines in the US as the

percentage calculations in the table show.

Europe has been hurt badly but it is a region with far more

labor market rigidities than the US. And those rigidities help

employment during times of economic shocks. Employment in the Euro Area

is down by just 1.3% Yr/Yr and unemployment is up by 20.9%. Compare

that to the US where employment is down by 3.1% Yr/Yr and unemployment

is up by 63% Yr/Yr. But even with those figures the ratio of the

unemployed-to-employed is greater in the Euro Area than in the US. The

fact is simply that the US unemployment rate was much lower than

Europe’s before recession and now it has ticked up to the same general

region as Europe’s rate.

Obviously the structure of the economy in Europe and in the US

is very different. Still this recession has hit Europe hard. By its own

metrics the labor market has been hit hard. The US is looking at one of

its most severe recessions in the Post-war period. EMU has not been

around long enough to make any such statement.

Through 2009-Q1 both EMU and the US are showing signs of an

increased pace of job losses and an increased pace of unemployment.

Monthly data in the US strongly support the notion that the

unemployment mess is unwinding rapidly in Q2. At this pace of unwind

the US could have job growth by August of 2009. We have no such bright

future in hand for Europe.

While there is still a debate afoot about the US and whether

it will spawn a strong or weak recovery, we can be sure that Europe’s

will be slow in part because of all the disguised unemployment its

labor force rigidities hide. Forecasts still foresee weak growth for

the rest of the year in Europe. For the US that same forecast generally

is in place but conditions in the US are shifting pretty fast and some

forecasts have simply not been recast. Europe does not shift gears fast.

We can’t judge the recession to be than much harsher in the US

than in Europe because of the jobs data and the greater US labor force

displacement. There are simply different economic structures at work.

But the figures are telling in terms of the impact on jobs in both EMU

and in the US. GDP has been hard hit in both regions. In the US the GDP

downturn simply dislodges more jobs. US GDP has fallen by about 6%

(SAAR) for two quarters a row. In EMU the drops have been more like 7%

and 10% at annual rates. Clearly jobs don’t tell the whole story of

dislocation.

| Growth rates by Quarter or period for various EU Nations | |||||||

|---|---|---|---|---|---|---|---|

| Saar: All | Q1-09 | Q4-08 | Q3-08 | Q2-08 | 2Qtr | 4Qtr | 5Yr |

| All Employed: EMU | -3.3% | -1.4% | -0.7% | 0.2% | -2.3% | -1.3% | 0.9% |

| No Unemployed | 39.9% | 26.6% | 12.0% | 7.8% | 33.0% | 20.9% | 0.5% |

| EA: Industry | -5.3% | -3.9% | -1.7% | -0.8% | -4.6% | -2.9% | -0.8% |

| EA: Agric, Forestry | -2.5% | 0.8% | -2.2% | -5.5% | -0.8% | -2.4% | -1.3% |

| EA: Construction | -8.6% | -8.7% | -5.8% | -4.6% | -8.6% | -6.9% | 0.6% |

| EA: Wholesale Retail | -3.8% | -1.5% | -0.2% | 0.3% | -2.7% | -1.3% | 1.0% |

| EA: Financial | -3.9% | -2.2% | 0.3% | 0.9% | -3.1% | -1.3% | 2.5% |

| EA: Gov't Education | 0.0% | 2.2% | 0.5% | 2.5% | 1.1% | 1.3% | 1.4% |

| Memo: Industry Employment | |||||||

| Germany | -3.8% | -0.1% | 0.2% | 1.0% | -2.0% | -0.7% | -0.2% |

| UK (MFG)* | #N/A | -6.6% | -6.3% | -2.0% | -6.5% | -4.0% | -3.4% |

| France (MFG) | -5.8% | -3.3% | -1.6% | -1.7% | -4.6% | -3.1% | -2.0% |

| UK growth rates lag by one quarter | |||||||

| US Employment | -6.7% | -3.4% | -1.9% | -0.4% | -5.1% | -3.1% | 0.4% |

| US Unemployment | 88.0% | 65.2% | 61.8% | 41.7% | 76.3% | 63.4% | 8.3% |

| US MFG Employment | -17.0% | -9.4% | -4.7% | -4.1% | -13.3% | -8.9% | -2.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief