Global| Aug 13 2014

Global| Aug 13 2014EMU IP Weakens, Adding to Weakness Elsewhere

Summary

The worries about European growth are for good reason. Total EMU industrial production excluding construction fell by 0.3% in June after a 1.1% decline in May. In the quarter, it's rising at a 0.1% annual rate. That's pretty thin [...]

The worries about European growth are for good reason. Total EMU industrial production excluding construction fell by 0.3% in June after a 1.1% decline in May. In the quarter, it's rising at a 0.1% annual rate. That's pretty thin stuff.

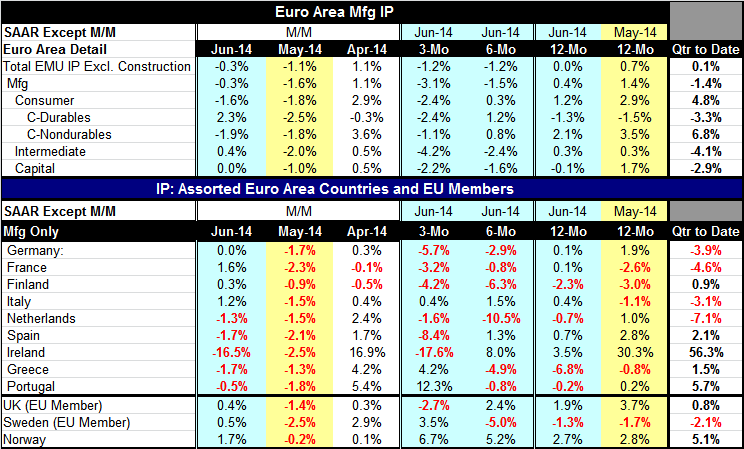

The worries about European growth are for good reason. Total EMU industrial production excluding construction fell by 0.3% in June after a 1.1% decline in May. In the quarter, it's rising at a 0.1% annual rate. That's pretty thin stuff.

Manufacturing output is doing worse; it fell by 0.3% in June after falling 1.6% in May and is declining at a 1.4% annual rate in the quarter. The strength and manufacturing in the quarter came from consumer goods and specifically from consumer nondurables output that rose at a 6.8% annual rate. Consumer durables output fell at a 3.3% annual rate. Intermediate goods output fell at a 4.1% annual rate. Capital goods fell at a 2.9% annual rate. There is a lot of weakness in manufacturing. We've seen evidence of this in the monthly PMI reports. The weakness is not a surprise.

Looking at EMU country data, we see in June declines in output for five of the nine reporting countries in the table. The declines are in Ireland, Spain, Greece, the Netherlands and Portugal. Output is increasing in Italy, France, and Finland while it is flat in Germany. This result follows May where industrial production fell in all these reporting countries.

The quarter to date result, now a full quarter's result, on a country basis shows a 7.1% decline in manufacturing output in the Netherlands, a 4.6% decline in France, a 3.9% decline in Germany, and a 3.1% decline in Italy. Ireland shows an outsized 56.3% annual rate increase; there is a 5.7% increase in Portugal, a 1.5% increase in Greece, a 2.1% increase in Spain, and a 0.9% increase in Finland. Ireland's outsized result stems from two months of outsized production increases, but output is back down to weaker levels in June. Still, the strength in the earlier months is enough to create that gigantic growth rate for Ireland in Q2.

Looking at the sequential growth rates, we have three-month declines in output in six of these nine reporting countries over three months as well as over six months. Year-over-year, only four of them show declines.

Industrial production data show substantial recent weakness in the peripheral countries of Spain, Ireland, Greece, and Portugal. Each one of these countries has a drop in industrial production for two months running. Germany, a country we are worried about due to the impact of sanctions on Russia, has flat industrial production in June and a 1.7% decline in May. Its quarter to date drop is 3.9%. All of these are very weak numbers, especially for Germany, an economy that tends to be led by its industrial sector.

There are results for a few non-EMU countries at the bottom of the table. The U.K., Sweden and Norway showed an increase in output in June after each of them showed drop in May. The U.K. shows a manufacturing output increase of 0.8% in the quarter to date. Norway's output increases 5.1% at an annual rate. Sweden is posting a 2.1% decline at an annual rate.

We can see from these data that there's a great deal of weakness spreading through the European Monetary Union and in Europe in general. The quarter-to-date data show a great deal of weakness. But total industrial production excluding construction is still up by a thin 0.1% in the quarter. From this, it looks like industrial output may be a drag on GDP growth, but it won't be dragging it into negative territory. But the same can't be said for manufacturing where the negative numbers are widespread.

Beyond European Industrial Production

It's a difficult day for economic data. Japan reported a bigger decline in its GDP in the second quarter than its increase in its first quarter in the wake of the hike of its consumption tax. The damage seems to be worse than the authorities expected. The strong 6% growth rate in the first quarter seemed to give them plenty of room to weather a weak second quarter. Yet, the second quarter has to come in so weak that it's enough to make them worry. At least in yesterday's reports, we saw some increase in consumer confidence in Japan even though it's on balance a negative reading.

In China there're reports of weaker industrial production; retail sales are weaker than had been expected. Lending trends in China are also weaker than expected. The world economy usually depends on Asia for a bump up in growth. Instead we're getting pulses of negativity from both China and Japan on reports released just today.

Further data released in the EMU show continued price weakness. Germany has reported its smallest HICP increase since 2010. One bright spot in Europe was that Greece reported a GDP result showing a decline by only 0.2%. That may be heralding the end of Greece's long recessionary nightmare. While that's a good story for Greece, Greece is a small country and that doesn't affect the EMU's fortunes very much.

Meanwhile, the geopolitical difficulties are playing out. These difficulties are not having much impact on the oil market because of surpluses that have been generated at least in part due to increased energy output in the United States. There is a coming conflict as Russia sends a convoy to help the separatists in Ukraine and Ukraine says it will not allow this convoy to enter the country. In Iraq Maliki has denounced the new leader that has been appointed, saying that the process was unconstitutional. He clings to power with his country under attack. Meanwhile, the IS is said to be spreading its control of territories within Syria.

Economic data trends are not good. The geopolitical background is pretty bad. The weakness in Japan and China is really worrisome. It's too soon to tell how worried we should be about conditions in Europe. Europe is going to have its worst growth rates in the next two quarters when the impact of sanctions on Russia hit the hardest. Since we tend to look at annualized figures, we are going to blow these impacts out of proportion compared to what they really are. But since Europe's trade with Russia is generally pretty small potatoes, the current European data are somewhat less frightening than the news out of China or Japan where pure and simple economic forces are simply decaying. However, that doesn't mean that Europe is a cakewalk. On top of the effects from the sanctions on Russia, there are ongoing difficulties in getting growth moving and prying inflation, up to more moderate levels. Right now the European Central Bank seems to be pretty stretched to try to accomplish those goals.

Meanwhile, back at the ranch, the U.S. economy is not exactly kicking up its heels. While the U.S. job market looks like it might have accelerated, the July jobs report did not build on that good news. Retail sales growth seems to have stalled too. At the Fed, there is growing discord between those who are worried about lingering high rates of unemployment versus those who are worried about some increasing pressure on inflation. The world's economies have a policy conundrum. Central banks are stretched. Fiscal policy is for the most part tethered either by political discord or remorse over past misuse. Today's reports only make things seem even worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief