Global| Apr 16 2020

Global| Apr 16 2020EMU IP Ticks Lower in February; The Worst Still Lies Ahead

Summary

The only sure things in life are death, taxes and the fact that the coronavirus will haunt you if not stalk you down. The February IP accounting from the EMU is the last report from the EMU on IP before the abject weakness from the [...]

The only sure things in life are death, taxes and the fact that the coronavirus will haunt you if not stalk you down. The February IP accounting from the EMU is the last report from the EMU on IP before the abject weakness from the virus will strike next month. It is stalking the data…

The only sure things in life are death, taxes and the fact that the coronavirus will haunt you if not stalk you down. The February IP accounting from the EMU is the last report from the EMU on IP before the abject weakness from the virus will strike next month. It is stalking the data…

In that sense, we do not have much to 'take away from this report' other than to note the pre-existing strength ahead of the coming virus incapacitation.

A voluntary collapse…ashes, ashes, all fall DOWN!

Let's ALWAYS remember that the virus incapacitation is the result of policy directives and industries shutting down under orders and not from the 'natural' transmission of economic weakness through normal channels. There is nothing normal about what is going on and that is why the economic data transit from trend to trash so quickly. In a normal economic environment different firms and regions would discover the developing weakness in a more random or uneven pattern causing some to react quickly and others to respond later, flattening out the decline in the IP curve. But since this recession is weakness 'by decree' the hammer blow is swift, sudden and syncopated. In February, that hammer was still in its backswing, but the compression of the hammer on the anvil lies ahead.

Sector stories

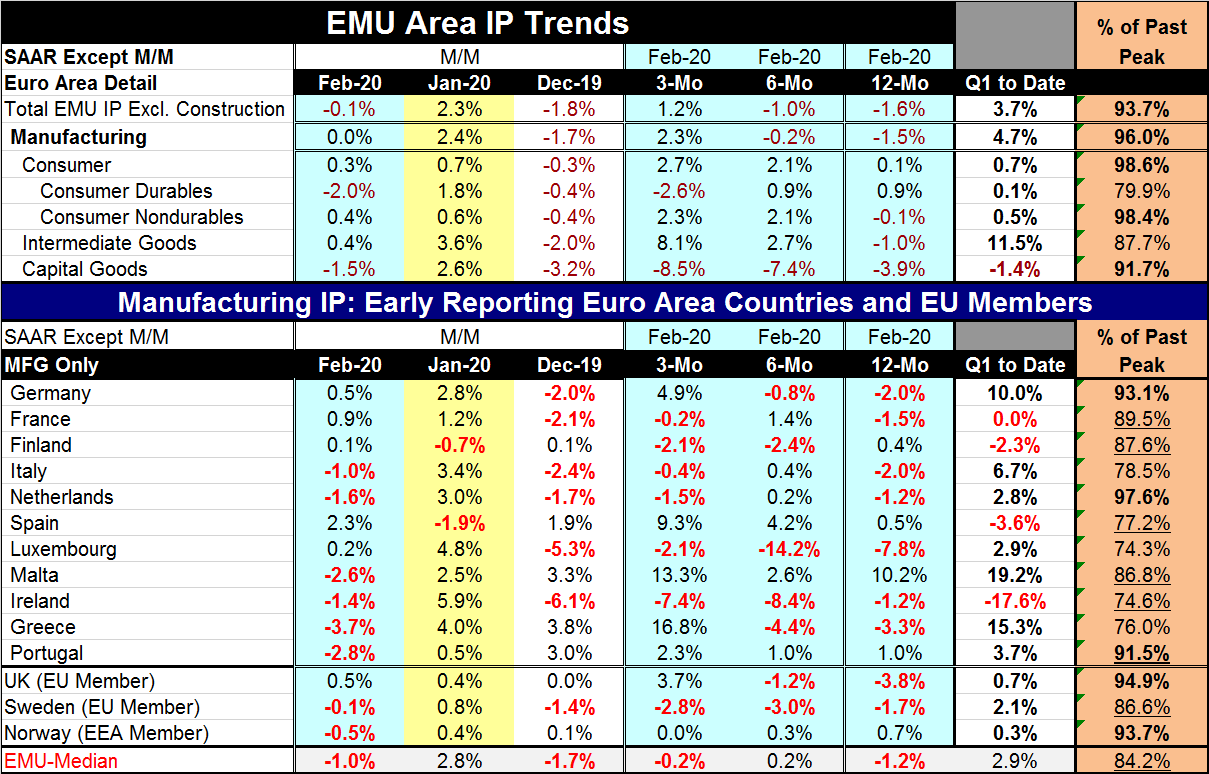

Headline EMU IP in February fell by just 0.1%, but it is locked in a progression of improving annualized rates for growth from 12-months to six-months to three-months…for now. The same is true for manufacturing output. Nondurable and intermediate goods output shows that sequential acceleration is in play. Capital goods trends demonstrate gathering weakness. Only capital goods output is falling on a quarter-to-date basis two months into the current quarter. But neither consumer subsector is very robust.

It's coming...

Scanning the rest of the table across countries, of the 11 EMU members whose results are chronicled there, six show declines in February with Finland eking out a 0.1% gain and Luxembourg at a 0.2% gain. Only Spain, France and Germany – three of the four largest EMU members - have significant increases in output in February. But we know what awaits around the corner. For example, we know that the EMU manufacturing PMI drops to 44.5 from 52.6 in March. We know that the German manufacturing PMI drops to 45.4 from 48.0. We know that the French manufacturing PMI drops to 43.2 from 49.8. We know that the Spanish PMI drops to 45.7 from 50.4. We know the Italian PMI drops precipitously to 17.4 from 52.1. And we know that the EMU services PMI takes a huge hit, dropping to 26.4 in March from 52.6 in February, a halving of its signal in one month. That weakness will spread and multiply.

IP and PMI are on the same page

So what is on its way is known to a large extent. This month the IP and PMI data were awkwardly on the same page. The IP gauge showed a weakening with output contraction while the EMU manufacturing PMI showed a month-to-month strengthening but also signaled a small output decline. So whatever mixed signal we see in the change was not there in the overriding level signal where the PMI agreed with the IP gauge that there would be (and was) a drop in activity. Except for Germany, the Markit PMIs gauges are presenting their weakest output result since January 2016. So yes, it is going to be weak but it is also being controlled.

Braking is always easier than accelerating...

Controlled…we hope it stays that way when it's time to take the foot of the brake. However, interrupting a capitalist economy creates it shown issues and there is never a guarantee that things will go back to where they were or to get there quickly. Certainly, the virus and the response to it already will have damaged the economy (it already has taken a lot of lives). We can only speculate about how else it might be changing the future. Life and behavior, human interaction, will certainly be different on the 'other side' at least for a while. But just how different it will be is hard to say. Already some experts are talking about the resumption of sporting events and the way they speak of it would be to introduce sports the way we never have seen them before. Are you ready for football (either variety)? Are you ready for football in an empty stadium, empty except for the players, coaches and officials? If you 'bend it like Beckham' and it goes in the net and no fan is there to cheer, is it just as exciting? If we are still isolating, what will they show in sponsoring beer commercials? These are the important questions…

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief