Global| Sep 12 2013

Global| Sep 12 2013EMU IP Takes A Dip

Summary

Trends in industrial production output in the European Monetary Union continue to skim below the surface of unchanged. While capital goods output has flirted with year-over-year increases as has consumer goods output, zero seems to be [...]

Trends in industrial production output in the European Monetary Union continue to skim below the surface of unchanged. While capital goods output has flirted with year-over-year increases as has consumer goods output, zero seems to be a hurdle the two sectors are unable to go over on a sustained basis. Intermediate goods output continues to trim its losses but also extends its losing streak of declines.

Trends in industrial production output in the European Monetary Union continue to skim below the surface of unchanged. While capital goods output has flirted with year-over-year increases as has consumer goods output, zero seems to be a hurdle the two sectors are unable to go over on a sustained basis. Intermediate goods output continues to trim its losses but also extends its losing streak of declines.

The improvement reported in the PMI indices can be seen in the microscopic elevation of the trends for the various sectors. However, the degree of progress is very small and the rate of progress has been very slow.

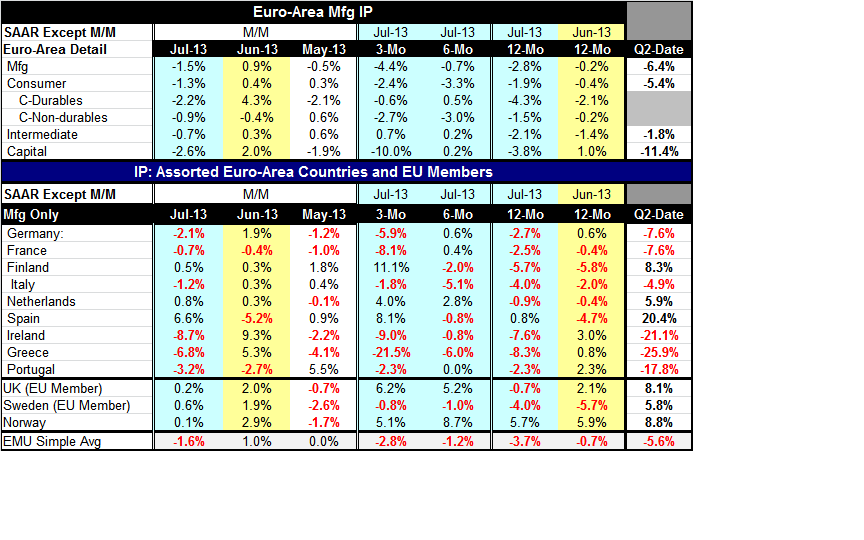

Tabular data show us that manufacturing output continues to decline sharply in July, dropping by 1.5% after rising by 0.9% in June. The June increase followed a May drop of 0.5%. Over three months the annual rate of change in industrial output is -4.4%. It's probably not the figure you'd be looking for after looking at the PMI indices for manufacturing.

Overall consumer goods output fell by 1.3% in July following two months of moderate increases. Consumer durable goods output fell by 2.2% after a relatively sharp increase in June that followed a moderately strong decline in May. Over three months consumer durables output is still falling at a 0.6% annual rate. Consumer nondurable goods output declined by 0.9% in July following a moderate decline in June and a firm increase in output for May. Nonetheless over three-months consumer nondurables output is falling at a 2.7% annual rate.

Intermediate goods output fell by 0.7% in July following two straight months of declines in May and in June. As a result the three-month annual rate for intermediate goods shows an increase of 0.7%.

A number of EMU countries, particularly Germany, are led by their capital goods sectors. In July EMU-wide capital goods output fell by 2.6%, more than offsetting the 2% gain for June which it followed a 1.9% decline in May. The net result of these oscillations is a -10% annual rate decline in the output of capital goods over three-months.

Broader trends show that overall output is declining faster over three months than it is over 12 months. The 4.4% annual rate decline over three months exceeds by a wide margin the 2.8% annual rate decline over 12 months.

Consumer goods' 2.4% annual rate of decline over three-months also exceeds their 1.9% rate of decline over 12 months, however, in this case the category shows a slight improvement from the -3.3% pace of decline over six months. Consumer durable goods show a sharp, 4.3% decline, over 12 months then post an increase of 0.5% at an annual rate over six months and then relapse to show a -0.6% rate of decline over three months. Still, that's a relative improvement. For nondurable goods, where conditions continue to be weak and possibly weakening, we find that nondurable goods output is falling at a 1.5% annual rate year-over-year but over six months output is down at a 3% annual rate over three months, then down at a 2.7% annual rate, indicating a step up in the pace of decline in the recent six-and three-month periods.

Intermediate goods, oddly are showing some improvement in output trends from a -2.1% pace over 12 months to a +0.2% pace of increase over six months to a 0.7% rate of increase over three months. I call it `odd' because both final goods classifications, consumer goods and capital goods, show declines, so it's odd to see intermediate goods on an improving trend.

The trend for capital goods is not an unambiguous deterioration, but the -10% annual rate decline over three months is more than double the 3.8% rate of decline over 12 months although, in between, over six months the category had posted a small increase.

Of the nine EMU countries reporting eight of them show year-over-year declines in industrial output. The exception is Spain that has the most volatile numbers (its twelve-month decline was 4.7% just last month, for example). Over six months five of the nine countries show declines with Portugal showing flat performance. Over six months the Netherlands leads the pack with a 2.8% annual rate of increase in industrial output compared to annual rate increases of 0.6% in Germany and 0.4% in France. Over three months, six of the nine countries show declines in industrial output, led by declines in Greece, Ireland, France and then Germany, in that order. Countries showing rebounds over three months are led by Finland with an 11.1% rate of increase, Spain with an 8.1% rate of increase, and the Netherlands with a 4% rate of growth.

On balance the picture for industrial production in the European Monetary Union remains uneven and spotty. The PMI surveys for manufacturing are a little bit clearer; their focus is on improving trends in the PMI indices even when the values are below 50. The data on actual output by country and industry remain quite weak and quite uneven, and they are accompanied by continuing weak inflation reports. While the Germans and the ECB may like weak inflation, when inflation continues at such a low level for an extended period of time it's often also a statement about weak aggregate demand and that would not be good news.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief