Global| Feb 12 2015

Global| Feb 12 2015EMU IP Struggles- Are We All Roiled by Oil?

Summary

In the EMU we see a great deal of variation in output by country and now we can see the EMU by sector performance. EMU IP (industrial production) less construction is flat in December and manufacturing output is flat as well. Year- [...]

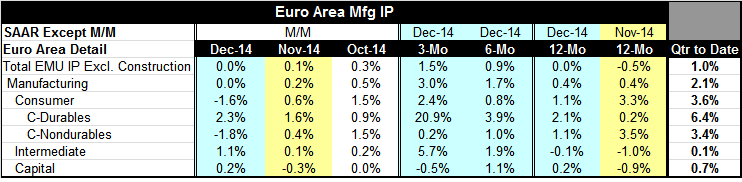

In the EMU we see a great deal of variation in output by country and now we can see the EMU by sector performance. EMU IP (industrial production) less construction is flat in December and manufacturing output is flat as well. Year-over-year output is flat while manufacturing is up by 0.4%. On balance, all is pretty flat if we consider the rolling hill of 0.4% growth over 12 months low.

In the EMU we see a great deal of variation in output by country and now we can see the EMU by sector performance. EMU IP (industrial production) less construction is flat in December and manufacturing output is flat as well. Year-over-year output is flat while manufacturing is up by 0.4%. On balance, all is pretty flat if we consider the rolling hill of 0.4% growth over 12 months low.

For December alone the consumer sector sees a decline in output with intermediate goods output higher and capital goods output ticking up by just 0.2%. In November overall IP rose by 0.1% while manufacturing gained 0.2%. Still, on three months IP growth is up at a 1.5% pace and manufacturing is up at a much more solid 3%. Consumer goods output over three months is up at a 2.4% pace, intermediate goods output is up at a strong 5.7% pace while capital goods lag, with output falling outright at a -0.5% pace. A pullback, not just a slowdown, has hit capital goods.

Twelve-month output trends are still very uneven but clearly weak. Manufacturing output is up by 0.4% led by consumer goods output rising at a 1.1% pace. But intermediate goods output is lower by 0.1% outright and capital goods growth is only at a 0.2% pace.

Forecast changes for growth vs. the reality of the future

While a number of euro area forecasts are trending up (for Germany and France just recently), challenges remain. Moody's has looked at the year ahead and despite lower oil has not ratcheted up its outlook for 2015 for global growth. In the just-completed fourth quarter, EMU output is up at a 1% pace with manufacturing up at a 2.1% pace. Consumer goods output leads all sectors, rising at a 2.6% pace in Q4 with intermediate goods output ticking up at a 0.1% pace and capital good output up at a 0.7% pace. On balance, there is growth but it is mostly still quite moderate and with prospects of moderation to continue.

The role of prices declines

In addition, we have changes from pricing stirring the pot. The just finalized data for Germany, a key EMU economy, shows its CPI and HICP falling by 0.4% on the year. Prices are steadily decelerating and falling faster from 12 months to six month and from six months to three months. The three-month HICP for Germany is falling at a 2.7% pace while its domestic gauge is falling at a 3.3% annualized pace. The German domestic measure shows ex-energy inflation positive but also on a decelerating run up by 0.9% over 12 months but only at a 0.4% pace over three months. Take energy out of the picture and inflation is still very low and decelerating.

Germany's 11 main CPI categories show a diffusion reading of 36. Inflation over three months is accelerating in only 36% of those categories. Over three months, prices are actually rising in only three of 11 categories and unchanged in one other. Inflation falling is the rule, not the exception. It's not just energy anymore.

The energy sector has many a wavering tentacle

While one can try to chalk up falling prices to oil prices and its knock-on effects, that is not to dismiss the phenomenon or its effect. And as we are seeing in the U.S. and perhaps in Germany, there are negative knock-on effects for the machinery and capital goods sectors. I notice some economists try to summarize the negative impact with a chart on oil drillers. That is only a small part of oil's negative impact. The oil industry has been a voracious user of various special industry and construction equipment. The steel industry has been making pipe for expanding pipelines and for fracking. In the U.S. as all of that is being cutback, there are job losses across sectors. It is estimated that 100,000 jobs worldwide have been lost in the oil patch after a period of seven years of the industry finding it was persistently short of filling its job needs. Do you think that won't hurt? Will more spending on retailing and in hamburger joints replace those lost jobs adequately? Yes, of course! I'm in hamburger engineering! Want pickles with that burger son?

The `sure thing' that is now surely a dead thing: whatever it takes...

Energy has been a driving sector for global growth. There were fears of a China growing and adding to demand for scarce resources. Oil prices had been driven high. Alternative oil-production schemes and gas development methods were being employed and not only were they adding to output the investment was galloping ahead, piling up and mushrooming for the future. That investment was a SURE THING. And now it is gone. The Saudis have vowed that oil will not go back up to $100/bbl again. Is that simply hyperbole? OPEC, led by the Saudis, is determined to restore its share of the oil market. If they are really so determined, then they will NOT STOP until many forms of alternative production have been shut down, to use an expression that has been popular of late, WHATEVER IT TAKES.

The Saudis: The ultimate reality show family

If you do not believe the Saudis will really be so destructive and ruthless with the global economy, remember what OPEC did in the early 1970s. The severe 1973-1975 U.S recession was followed by an eventual bust in oil prices too. You see oil has lags. Demand is inelastic in the short run, but given big incentives and time, demand and supply can make big change; the key here is `given time and large incentives.' What is different this time is that there are a lot of marginal oil/energy producers outside OPEC, many in the U.S. When you disrupt supply, you are disrupting a lot of U.S. based production and the feeder industries for it. In fact, we have no reason to doubt that the Saudis will pursue self-interest ruthlessly - even though they lost sight of self-interest when they allowed oil prices to spurt up to and above $100/bbl. That was not in Saudi best interests and the Saudis should have known it. But now they recognize the error of their ways. It will now become the error of our ways.

Destructive destruction, Mr. Schumpeter

This of course will mean some destructive destruction (as opposed to Schumpeterian creative destruction) of some aspects of the economy. It will mean some permanent roll back to the level of oil prices with enduring benefits for consumers. For some, this may undermine efforts to implement higher gas mileage standards in automobiles and such. If we roll back gasoline prices, does the Prius- does the Leaf - make any sense? They were great innovations for our coming future but are they now?

Umm, err, oh. heck, never mind

I think there is a great underestimation of the adverse consequences for the economy going forward to a permanent lower level for oil prices. Part of what the economy has been gearing up for (higher oil prices and better conservation) no longer will make as much (economic) sense. Location and transport costs no longer loom as such a big deal. Mileage on everything from cars to trucks to jet aircraft no longer matters as much. What of all that domestic U.S. oil that was being moved by trains? And the notion that Middle East is no longer so important because the U.S. is headed for energy independence? Forget that. The Middle East is back on the map. Did Obama take the opportunity to try to fill the SPR (Strategic Petroleum Reserve)? Has the Administration does anything about a policy geared by a foreign power to destroy a burgeoning U.S. industry? No. the U.S. has just rolled over for the Saudis and made nice during the period of the Kingdom's familial transition.

Winning or losing at global oil LOTTO

In the meantime, the simple fact of lower oil prices is reducing inflation and spreading that effect beyond just energy prices with knock on effects relevant to growth investment and the conduct of monetary policy just about everywhere. Sweden is the latest to make interest rates negative. The notion that this a one-off event discounts some important aspects of this transition. When we see the ongoing irregularities to growth, there is a tendency to dismiss them. That will not make them go away. There will be winners and losers on a global scale across countries as well as in industries and impacts on lending institutions. We are only beginning to see the scope of this adjustment. If the oil price reduction is permanent, there are going to be some nasty permanent surprises. The Saudis are dead set to drive some people out of business.

During this transition, it will become impossible to speak of developments in growth without understanding developments in energy prices and the knock-on impact to inflation trends as well as through economic multiplier effects on output and spending. It is a new world in the making. We are going back to the past, not back to the future: to the destructive destruction dismantling some of what we had created and doing that at a cost.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief