Global| May 14 2014

Global| May 14 2014EMU IP Shows Growth But Also Its Weak Side

Summary

Industrial production momentum in the euro area has been short-circuited in March. Industrial production excluding construction fell by 0.3%. Combined with a decline in January, the three-month growth rate logs a -0.8% annual rate. [...]

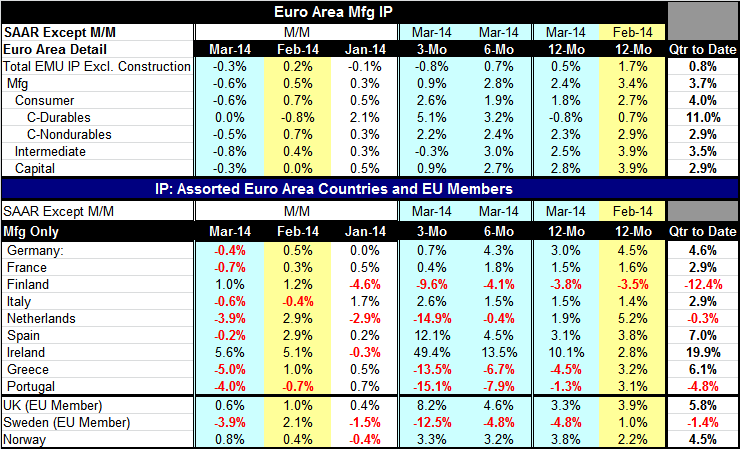

Industrial production momentum in the euro area has been short-circuited in March. Industrial production excluding construction fell by 0.3%. Combined with a decline in January, the three-month growth rate logs a -0.8% annual rate. The euro area now has a bit of a slowdown in train with 12-month production up at a 0.5% rate, six-month production up just slightly faster at a 0.7% rate and three-month production pace falling at a -0.8% rate. Despite that, industrial production on this measure will increase at a 0.8% rate for the European Monetary Union as a whole in the first quarter. Manufacturing will do even better at 3.7%.

Industrial production momentum in the euro area has been short-circuited in March. Industrial production excluding construction fell by 0.3%. Combined with a decline in January, the three-month growth rate logs a -0.8% annual rate. The euro area now has a bit of a slowdown in train with 12-month production up at a 0.5% rate, six-month production up just slightly faster at a 0.7% rate and three-month production pace falling at a -0.8% rate. Despite that, industrial production on this measure will increase at a 0.8% rate for the European Monetary Union as a whole in the first quarter. Manufacturing will do even better at 3.7%.

In dissecting the trends for the month, we see weakness across the board. There is a decline in manufacturing of 0.6%, declining consumer goods output of 0.6%, a decline in intermediate goods output of 0.8%, and a decline in capital goods output of 0.3%. Over three months, however, only intermediate goods output is declining.

By sector, the consumer sector is performing a little bit better with the growth in output up at a 2.6% pace over three months compared 1.8% over 12 months. The expansion of nondurable output is steady; the expansion of consumer durable goods output has been accelerating. Intermediate goods output has been steady over 12 months and six months at a pace of 2.5% to 3%, but it's contracting by 0.3% over three months. Capital goods output is steady at a pace just below 3% over both three and six months, but over three months has fallen off to a pace of less than 1%. Capital goods output has fallen from the ranks of the strong sectors over three months.

By country, only three of the nine EMU members listed in the table show declines in output brewing for the first quarter. In Finland output will decline at a 12.4% annual rate. In Portugal, a decline is evolving at a 4.8% annual rate. In the Netherlands, IP will decline at a 0.3% annual rate. Of the other six countries, the weakest output is from France at a 2.9% annual rate while the top side is from Ireland at a 19.9% annual rate. For the most part, the story is that in the EMU industrial output will increase in the first quarter and the increase will be a broad-based phenomenon.

Still, there are some countries with significant trend issues. In Germany, the growth rate from 12 months to six months to three months moves from 3% to 4.3% to 0.7%, respectively. Similarly, in France, the growth rates go from 1.5% to 1.8% to 0.4% as we assess trends from 12 months, to six months, to three months. In Finland, 6-month and 12-month growth rates that are near a 4% annual rate erode to decline at nearly a 10% annual rate over three months. The Netherlands show progressive deterioration from a 1.9% growth rate over 12 months, which falls to -0.4% over six months and to -14.9% over three months. Greece and Portugal also display progressively weaker growth rates with negative figures over 12 months that show deeper declines over six months and over three months. Ireland, Spain and Italy are the only three countries to show progressive acceleration for industrial output.

As is always the case in Europe there seem to be mixed trends here. Despite a widespread expansion for industrial production in the first quarter, the bulk of countries in the euro area are showing some weak to waffling industrial production trends. Only three of the countries are showing acceleration to counter the slowing trend. That's not very reassuring. This may simply turn out to be an `endpoint' problem as March turns out to be a month of unexpected weakness; since we calculate growth rates relative to March, it dims the lights for all the growth rates. We will look for that in April to see if there's a rebound that reverses these trends.

For now, the story is that while the trends in the euro area are somewhat muddied, the euro area will post positive growth rate for industrial production in the first quarter. The gains in manufacturing will be even stronger. And the manufacturing gains will be rather widespread across the euro area. Although this is somewhat reassuring, given the irregularity with the trends, it's not definitive. And since Germany, the largest country in the euro area, has turned up some uneven data recently, there's more reason for caution about the outlook.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief