Global| Mar 12 2010

Global| Mar 12 2010EMU IP Sees Light Of Day- Posts Yr/Yr Growth

Summary

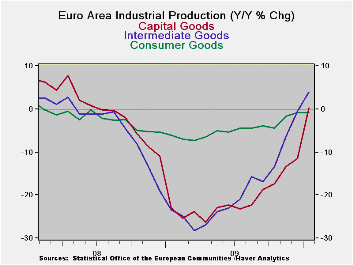

In a shocker of a report EMU IP ratcheted up much more than expected in January and the December reading got a boost due to revision as well. As a result industrial output now is growing 1.5% Yr/Yr in all of EMU. It is the first Yr/Yr [...]

In a shocker of a report EMU IP ratcheted up much more than expected in January and the December reading got a boost due to revision as well. As a result industrial output now is growing 1.5% Yr/Yr in all of EMU. It is the first Yr/Yr rise in output since April of 2008. That leaves the index for output still some 17.2% below its cycle peak. While the Yr/Yr gain is good news and boosts output five percentage points, up from its cycle low, clearly there is a long way to go for Europe to get back where it was. Yr/Yr gains are a necessary, but not a sufficient condition for full recovery.

This is just another way of trying to find perspective. While the current IP rise is good news it represents only a baby step of progress. There are still many resources left idled by recession and the recession/ financial crisis already has dragged on for a long time – over two years in the case of the US. Clearly with such a large output gap in place (industrial output 17% off from its cycle peak) some resources could spend four years being idled (roughly two in recession and two in recovery) before they are used again. That is a stunning prospect. It also helps to explain why the recovery could well be stronger than what people are expecting. The economy’s ability to grow fast for an extended period of time is simply being underestimated. If EMU’s IP grew 8% per year for two years running it would still not quite be back to the past cycle peak and over that period, presumably, capacity itself would grow.

In Europe the broad social welfare net provides a deeper cushion for more people compared to the assistance offered in the US. Arguably it makes the US recession more painful and that prods the economy and its workers more sharply to find a solution more quickly.

Tax cuts and incentives may help. But these sorts of things must be very carefully crafted or they just wind up being give-aways with no real stimulus.

It’s a good thing Europe is growing more briskly since this problem in Greece is going to notch up the head winds for Europe to some extent. Already it has unleashed a firestorm of protests within Greece, produced cries for trading reforms especially on credit default swaps and it has brought out some of the under the surface tensions in EMU as German Finance Minister Wolfgang Schaeuble called for “prohibitive” sanctions including expulsion from the euro region as the ultimate penalty for countries that repeatedly flout debt rules. This is chilling stuff and a full 180 degrees from Sarkozy saying if Greece goes bankrupt, Europe will have failed. Europe remains quite heterogeneous. Perhaps that is what European nations have most in common.

The brighter more robust economic backdrop is a breath of fresh air. More to the point it signals a stronger economic tail wind than what we thought we had before. It can help so stave off the effects of the harsher political head winds that suddenly have emerged. All this underscores the nature of recovery data, that they can run hot and cold, seemingly for no reason whatsoever. And in the wake of recession, along with recovery, there often there is other fallout and the pitfalls that such events bring.

That is why this recession is a real recession, not the recession-lite of 1990 or of 2001. In those episodes the central banks eased the pain early and essentially excesses have been piling up ever since. It takes a good recession to purge the system of its hidden abuses, or abusers, like Bernie Madoff. Had markets continued to rise, Bernie would have escaped detection along with others like him and his scam would have gotten bigger and more damaging. Recessions have a role in economics and although they are bad, they are cleansing. The key is to pick up the pieces and do better next time. If we do the next cycle will less painful. Can we do it?

| Euro-Area MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Jan 10 |

Dec 09 |

Jan 10 |

Dec 09 |

Jan 10 |

Dec 09 |

|||

| Euro-Area Detail | Jan 10 |

Dec 09 |

Nov 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-4 |

| MFG | 1.8% | 0.2% | 1.4% | 14.1% | 6.2% | 9.6% | 6.5% | 1.5% | -4.4% | 14.9% |

| Consumer | -0.1% | 0.4% | 1.3% | 6.8% | 2.7% | 0.8% | 1.4% | -0.8% | -0.8% | 3.8% |

| C-Durables | 2.0% | -0.8% | 1.7% | 11.8% | 4.4% | 10.7% | 8.2% | -2.5% | -6.5% | -- |

| C-Non-durables | -0.3% | 0.6% | 0.9% | 5.1% | 0.8% | -0.2% | 1.1% | -0.3% | -0.2% | -- |

| Intermediate | 1.4% | -1.4% | 0.6% | 2.4% | 1.6% | 5.7% | 7.9% | 4.0% | -0.5% | 3.9% |

| -0.3% | -0.2% | 1.5% | 3.8% | 2.6% | 7.3% | 5.5% | 0.2% | -11.6% | 0.1% | |

| Main Euro-Area Countries and UK IP in MFG | ||||||||||

| Mo/Mo | Jan 10 |

Dec 09 |

Jan 10 |

Dec 09 |

Jan 10 |

Dec 09 |

||||

| MFG Only | Jan 10 |

Dec 09 |

Nov 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q:4 Date |

| Germany: | 0.9% | -1.2% | 0.9% | 2.5% | -8.3% | 9.3% | 5.2% | 3.6% | -5.7% | 1.4% |

| France: IPxConstruct'n |

1.6% | -0.2% | 0.8% | 8.8% | 1.8% | 6.0% | 5.1% | 3.5% | -1.8% | 2.6% |

| Italy | 2.8% | 0.2% | 0.9% | 17.0% | 9.4% | 12.1% | 9.2% | 0.0% | -5.5% | 3.6% |

| Spain | -3.0% | -0.6% | -0.1% | -14.1% | -4.7% | -6.6% | 1.2% | -1.6% | -2.4% | -11.2% |

| UK: EU member | -0.8% | 0.9% | 0.1% | 0.9% | 4.1% | -0.4% | 2.0% | 0.2% | -2.0% | 4.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief