Global| Dec 12 2013

Global| Dec 12 2013EMU IP Sags in October

Summary

While EMU industrial production is off in October, it still has eked out a small gain over 12-months. Its gains continue to lag behind those of industrial output in the US, but both the US and EMU IP trajectories appear to be headed [...]

While EMU industrial production is off in October, it still has eked out a small gain over 12-months. Its gains continue to lag behind those of industrial output in the US, but both the US and EMU IP trajectories appear to be headed higher.

While EMU industrial production is off in October, it still has eked out a small gain over 12-months. Its gains continue to lag behind those of industrial output in the US, but both the US and EMU IP trajectories appear to be headed higher.

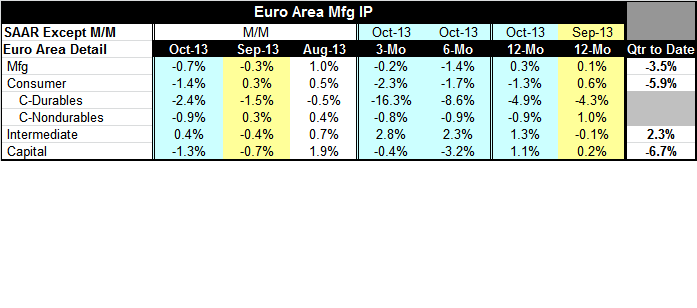

In October manufacturing IP in EMU fell by 0.7%. The largest monthly drop came in consumer durables followed by capital goods and consumer nondurables. Intermediate goods output continued to advance rising by 0.4% on the month.

Consumer goods harbor the worst trends among the main industrial production categories. Output over three months is dropping at a 2.3% annual rate, compared to a 1.7% pace of decline over 6-months and 1.3% over 12-months. Consumer durables output is dropping at an even faster pace (see Table). Meanwhile, consumer nondurables output is falling at a steady pace of just below 1% per year.

Intermediate goods output is engaged in a minor but steady acceleration rising by 1.3% over 12-months and at a 2.8% pace over 3-months.

Capital goods output has an uneven pattern as it rises by 1.1% over 12-months then contracts at a 3.2% annual rate over 6-months then recovers somewhat to fall only at a 0.4% pace over 3-months. Still capital goods output has fallen sharply in each of the last two months. It doesn't paint a very clear picture of recovery at all.

Manufacturing output in EMU has risen year-over-year for only two months in a row. Its last year-over-year rise, previous to this two-month episode, was in December 2011. The EMU manufacturing PMI has been above 50 (signaling sector expansion) since July of this year. It has held a value above 51 for the last four months.

The Markit manufacturing PMI gauges still see expansion ahead. The IP sector trend is much more equivocal. However, longer-term trends and momentum still seem to be positive. On the whole we still think that output will continue to expand in Europe. We look at the current setback as a temporary jog in a rising trend. The trend may be shallower than some had hoped. But the manufacturing PMI data do not suggest all that much strength as they have been trapped in a range of 51.10 to 51.52 for the last four months.

In the US, IP is advancing. In EMU, IP has been advancing. The global recovery still seems to be making its progress although in Europe it has been very slow and continues to be very uneven. Despite that we think it continues to move ahead. Europe continues to try to deal with its issues and the global economy continues to expand both will be positive forces for European recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief