Global| Jul 14 2014

Global| Jul 14 2014EMU IP Heads Lower

Summary

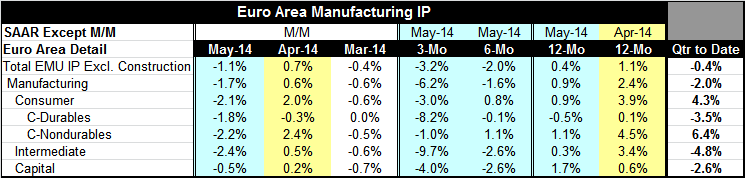

The European Monetary Union has reported its aggregate and industrial production result for May: the results show a huge decline of 1.1% in May output. Manufacturing output is down by 1.7% in May; this is the weakest one-month [...]

The European Monetary Union has reported its aggregate and industrial production result for May: the results show a huge decline of 1.1% in May output. Manufacturing output is down by 1.7% in May; this is the weakest one-month manufacturing result since September 2012.

The European Monetary Union has reported its aggregate and industrial production result for May: the results show a huge decline of 1.1% in May output. Manufacturing output is down by 1.7% in May; this is the weakest one-month manufacturing result since September 2012.

All major sectors of industrial production showed declines in May with consumer goods output falling 2.1%, intermediate goods output falling 2.4% and capital goods output falling 0.5%.

Over three months, all major categories show output falling; over six months only the category with rising output is consumer goods. Over 12 months, all major categories are showing increases.

The sequential growth rates for industrial output excluding construction show declines are getting progressively deeper with 12 month output rising 0.4%, six-month output falling at a 2% pace and three-month output falling at a 3.2% pace.

We previously reported how widespread were declines in output as EMU members are showing output declines in May across the board. A majority are showing declines in output over three months. This weakness is part of a pattern with weakness in consumer confidence and with the Markit-reported PMI indices also weak.

Although Banco Espirito Santo (BES), a private Portuguese bank based in Lisbon, has just had new management installed and markets are recovering from the scare that the bank gave them on Thursday of last week, we are reminded of financial fragility in Europe. Financial fragility is difficult enough to patch in a slow growth environment in all but impossible in a declining growth environment.

In the quarter to date, total EMU output excluding construction is falling at a 0.4% annual rate. Manufacturing output is falling at a 2% annual rate. Consumer goods output is rising at a 4.3% annual rate. Intermediate goods output is falling at a 4.8% annual rate and capital goods output is falling at a 2.6% annual rate.

These figures underpin the weak trends that we've seen with a surprising exception: that consumer goods output is showing some lift. Generally speaking, the consumer has not been the sector leading Europe in recovery. However, we are looking at the output of consumer goods, not at consumption directly. If these goods are not consumed, this could turn into an adverse inventory cycle. It's too soon to applaud for the strength in the consumer output sector. But we can hope it means something positive.

On balance, we started to raise our eyebrows with the announcement last week of weak industrial orders and output in Germany. We have continued to see reports of weakness in output with surprise weakness showing up in the UK and elsewhere. However, the declining output appears to be outsized compared to some of the weakness we've seen in the PMI indices - that backtracked but still point to growth. Although we've seen some faltering in consumer confidence, it has not been weak enough to generate concerns about growth. The next step is to look at what the European Central Bank does and how effective its policies are trying to revive growth in Europe. The recent economic data, however, suggest that the ECB is fighting more of an uphill battle than it thought.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief