Global| Mar 13 2019

Global| Mar 13 2019EMU IP Gains in January; EMU and Global Trends Still Sour

Summary

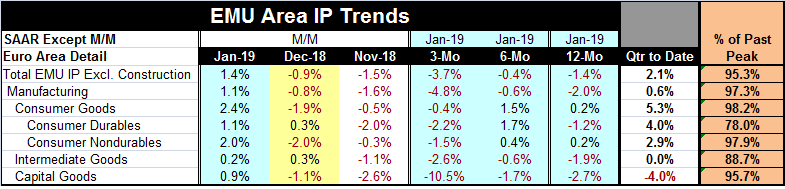

The EMU rebound in IP is touted as stronger than expected with a 1.4% rise in January, compared to an expected 1% increase. Fair enough. But as surprises go, this one does not take you anywhere since the trend lower is still well [...]

The EMU rebound in IP is touted as stronger than expected with a 1.4% rise in January, compared to an expected 1% increase. Fair enough. But as surprises go, this one does not take you anywhere since the trend lower is still well entrenched.

The EMU rebound in IP is touted as stronger than expected with a 1.4% rise in January, compared to an expected 1% increase. Fair enough. But as surprises go, this one does not take you anywhere since the trend lower is still well entrenched.

Broadly shared weakness

In the EMU in January among 11 early-reporting old-line EMU members, only Germany had reported a decline in IP (Belgium and Austria still have not reported at all). So it has been clear for some time that IP was going to make a gain in January. Still, in December seven of these 11 countries had IP drops and eight of them had declines in November with seven of those declines larger than a 1% one-month drop.

The extensive nature of the weakness is memorialized by the euro area growth rates (for headline and for manufacturing IP) showing declines over three months, six months and 12 months.

Interestingly, consumer goods output declines only over three months. But intermediate goods and capital goods output both fall on all three horizons. Capital goods output is collapsing at a 10.5% annual rate for the three-month period ended in January. What is that about?

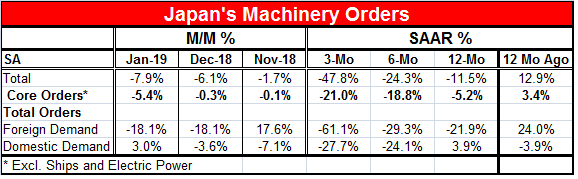

Capital goods sector weakness in Japan as well

In Japan, core machinery orders fell in January by an outsized 5.4% with the headline drop for all projects off by 7.9%. Core and total orders each are falling for three months running. Core orders also are falling monthly in four of the last five months while overall orders fall monthly in five of the last six months.

And in the U.S.?

U.S. nondefense capital goods orders excluding aircraft are falling on balance over three months and six months. While overall U.S. durable goods orders rise over three months; excluding transportations that gain switches to a decline.

The rest of Europe

In addition, industrial orders from Spain and Italy have been shrinking for a year. Spanish orders show exceptional weakness in the capital goods sector up through December. The euro area as a whole shows orders shrinking on all horizons out to a year and sales of capital goods shrinking over that entire timeline. The demand for and supply of capital goods is not accelerating.

Global weakness

The weakness for capital goods on a global scale is remarkable for an economic recovery period that has gone on so long. Late in cycle we might expect investment demand to be stimulated by tightening up capacity use. Instead, we see that capital goods output sales and orders are on declining profile even as globally unemployment rates remain exceptionally low.

Trade slows and shrinks

Trade slows and shrinks

Part of this is certainly the slowing and shrinkage of international trade. The Baltic dry goods index chronicles actual shrinkage in shipped volume. While some this traces back to the U.S. and its tougher stance on trade and its demands for fairness, the seeds of slowing were planted in many cases over a year ago. The EU is not yet embroiled in any trade war but it’s one of the fastest-slowing areas globally.

Optimism lost for many reasons

Still, part of the hit to the growth in capital goods output and industrial orders for such comes from a reduction in optimism that certainly accompanied the rising concerns about the prospect for a trade war. Uncertainty over Brexit and how that will affect U.K. trade and trade between EU countries and the U.K. also may be playing a part. There are plenty of trends afoot to explain the global slowing and on which to hang concerns about the future. And some of them are special local issues and others are things that are mixed in with some of these broader concerns such as about the potential for a trade war.

The new negotiating model

It is clear that Donald Trump has not approached the situation of trade bargaining with China in a classical way. In the past when tariff reduction was negotiated, it was multilateral. It also was piecemeal with the understanding that one ‘round’ would be completed and would be followed by another round. For example, in the recent Post-War period, we can chronicle the Kennedy round, the Tokyo round, the trade act of 1974, NAFTA and the transition from GATT to WTO in this framework. More recently, the attempt called Doha did not go so well. Trump is not negotiating on this model. Trump seeks a one-time deal to right the ship on trade with China. As such, he also wants enforcement mechanisms built in and clear objectives in order to evaluate compliance. It is not surprising given those objectives that the U.S.-China negotiation is two-sided vs. multilateral. It is also clear why the rest of the world has preferred multilateral deals; it is because they have been able to promote policies favorable to themselves and not favorable to the U.S. in a multilateral framework. But it is also clear that these hard-nosed tactics have played a role in unseating optimism on the future of growth and world trade, but it also underlines how that optimism was based on a business-as-usual format in which the U.S. would have continued to have been disadvantaged.

The role of a more self-oriented but not self-aware U.S.

Trump is determined to ‘Make America Great Again’ (MAGA-his campaign slogan). Few understand what that means. The New Progressives in the U.S. seem to think that the main problem is a shortage of demand (a concentration of wealth) and workers not being paid enough. But in fact, a persuasive case can be for the opposite point: that U.S. workers are - by world standards - still paid too much and that is why the U.S. is not competitive and part of the reason why it runs never ending current account deficits AND does not attract enough of the right kind of investment. The problem for the U.S. is getting its costs down and productivity up to match the level of the wages in the U.S. in comparison with wages in its trade partners, partners that are eating its lunch. The U.S. needs more education, more of it focused in the right areas, as well as more technology investment, the likes of which is mostly pouring into low cost venues in Asia, not in the Unites States. Trump and the New Progressives are fighting two different wars and each thinks the other is its enemy when in the fact the real enemy is a more competitive world with lower living standards than ours. No one has come up with a plan to deal with that, and THAT is not going away whether the U.S. elects Democrats or Republicans or promotes the local dog-catcher to office. China still has huge undeveloped parts of its country to tap for even more cheap labor. The slippage in the U.S. ability to create output competitively on the world stage coupled with its desire to consume and to lead the world in consumption are the inexorably clashing forces at work that no one seems to identify. A skewed income distribution is one of the ‘features’ of this system. But it is not the main problem; it is only another of its peculiar results. Something will have to give to truly make America great again in a way that is fairer and sustainable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief