Global| Jun 14 2021

Global| Jun 14 2021EMU IP Gains But Troubles Remain

Summary

Euro area industrial production rose by 0.8% in April, advancing for the second month in a row. Manufacturing output rose by 0.4% in April gaining also for the second month in a row, but it is still below its level output as of [...]

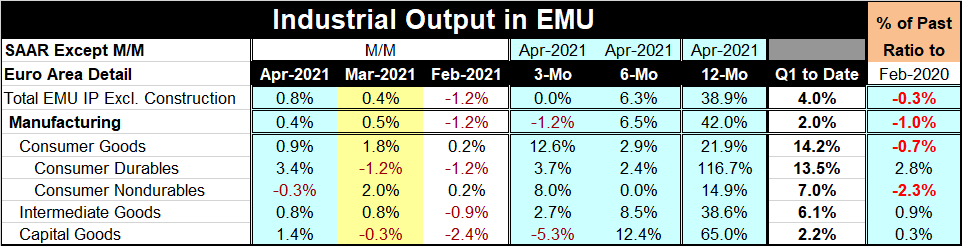

Euro area industrial production rose by 0.8% in April, advancing for the second month in a row. Manufacturing output rose by 0.4% in April gaining also for the second month in a row, but it is still below its level output as of January of this year. Both manufacturing and total output (excluding construction) are still below their February levels of output from 2020 before the virus struck. However, early in the new quarter-to-date total IP is rising at a 4% pace annualized and manufacturing output is up at a 2% rate annualized.

Euro area industrial production rose by 0.8% in April, advancing for the second month in a row. Manufacturing output rose by 0.4% in April gaining also for the second month in a row, but it is still below its level output as of January of this year. Both manufacturing and total output (excluding construction) are still below their February levels of output from 2020 before the virus struck. However, early in the new quarter-to-date total IP is rising at a 4% pace annualized and manufacturing output is up at a 2% rate annualized.

The Covid complication

These figures place Europe still in the recovery phase from Covid and in fact European nations are still dealing with Covid outbreaks as are most countries. In some places, the fight against Covid seems right now more like a rear-guard action while in other places the battle against the disease is still engaged. Because of the ongoing development and growth of virus variants that have become increasing more infectious, epidemiologists continue to worry about new outbreaks. But as infection spreads and as vaccination spreads, there are fewer and fewer places that the virus can go since immunity also spreads. The vaccines still are effective against these new strains of virus despite the increased virulence of the new strains.

However, Europe still has a lot of vaccinating to do and after strong starts in vaccinations in the U.S. have slowed; they have gone so slowly that the U.S. will end up having to discard some aging vaccines. At the G7 summit, the attendees agreed to step up and offer one billion doses to poor countries. Chile is a counterpoint to all the talk about vaccine progress. With more than 60% of its population vaccinated, it has ordered a lockdown in its capital, Santiago. Despite its substantial vaccination proportion, Chile's emergency room beds are nearly used up. Chile's experience is a warning that even as countries are making progress and opening up, disaster seems always ready to strike somewhere. The experience of Chile appears to say that true safety may only be achieved with a very high degree of vaccination.

Recovery is in progress

However, the recovery is nonetheless afoot in Europe where out of 11 only 3 show manufacturing output declines in April among select reporting EMU members. All these members show strong gains over 12 months, but that seems mostly a result of low base effects. Only four members show manufacturing output declines from February of last year. For most EMU members, output is advancing beyond its pre-Covid levels from early-2020 although few show signs of being back on their pre-Covid trends. Also the differences among manufacturing rates of growth are much higher than they were pre-Covid and those differences while down from their peak in previous months are still growing and this month they seem to have reached a new degree of monthly divergence. Of course, divergence makes it harder to run one monetary policy for the whole region.

A brief look at inflation

Monetary conditions are beginning to approach normalcy with EMU inflation now running slightly hot relative to target at a year-on year-gain of 2.0% in May. Among the 12 earliest EMU members, about half are above and half are below the EMU inflation rate. Above are Luxembourg, Belgium, Germany, Austria, Spain, Finland and the Netherlands. Below 2% are Greece, Portugal, Italy, Ireland and France. Countries' 12-month inflation rates range from 4.1% in Luxembourg to -1.2% in Greece. Comparing the second most extreme cases narrows the range to 2.5% to 0.5%. The median rate among members is Finland's 2.3%. The standard deviation of 12-month headline HICP among these 12 EMU members is higher than it has been for any annual period since mid-2010. Inflation is running hot for the first time since a brief four-month run ended in October 2018 and since January 2013 before that. Inflation has not run hot on a sustained basis for nearly eight and one-half years. What I now mean by 'hot' is 2% relative to a target of just less than 2%; inflation really is barely tepid.

IP shows some variance

Industrial production growth shows year-on-year rates across countries ranging from Spain's +162% to France's -8.5%. From February 2020, IP changes range from Ireland's 37% to Germany's -6.7%. The median gain from February 2020 is 0.9%.

Sector IP

By sector, EMU-wide IP growth rates range from 116.7% over 12 months for consumer durable goods output to 14.9% for consumer nondurable goods output. However, from February 2020, the differences are much less with highest gains at 2.8% for consumer durables and the weakest at -2.3% for consumer nondurables. All sectors are advancing in the quarter-to-date.

Summing up

On balance, EMU IP shows recovery is still in place and is broad-based and still has a way to go to be fully effected. The inflation situation, however, is transformed with inflation now much more in a normalized zone, albeit after a long period of undershooting, with growth still hampered, with Covid still in play, and with the ECB still implementing a highly stimulative monetary policy. Europe would seem to be on the edge of making some policy changes. But so far, the ECB has held to the view that stimulus is still the most appropriate policy. Central banks are making sure that they do not reverse polices too soon.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief