Global| Mar 15 2019

Global| Mar 15 2019EMU Inflation Trends Are Still Weak

Summary

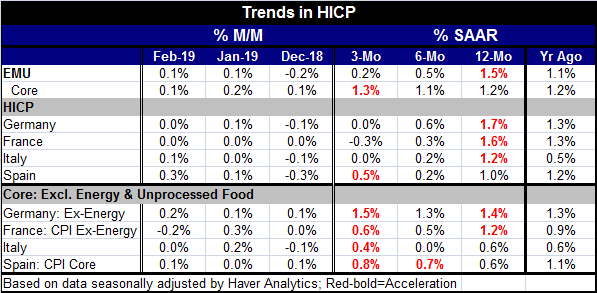

Headline: The EMU HICP for February gained 0.1%, the same as in January, after a 0.2% decline in December. These price trends signal that moderation remains the name of the game. Inflation is decelerating from an already modest 1.5% [...]

Headline: The EMU HICP for February gained 0.1%, the same as in January, after a 0.2% decline in December. These price trends signal that moderation remains the name of the game. Inflation is decelerating from an already modest 1.5% over 12 months to an annualized pace of 0.5% over six months and further to a 0.2% annualized rate over three months.

Headline: The EMU HICP for February gained 0.1%, the same as in January, after a 0.2% decline in December. These price trends signal that moderation remains the name of the game. Inflation is decelerating from an already modest 1.5% over 12 months to an annualized pace of 0.5% over six months and further to a 0.2% annualized rate over three months.

Core or ex-energy: The core rate shows low, but more stable, trends in price-gains as the core is less affected by the weakness and gyrations in energy prices. The core HICP is up by 1.2% over 12 months and at a 1.1% pace over six months. But the core pace also ticks up to a 1.3% annual rate of change over three months.

Inflation and trends in the largest four EMU economies

Viewing inflation through the four lenses of the four largest EMU economies, one still gets a picture of moderation and of widespread moderation as well.

Headline inflation: Headline inflation steps down progressively from 12-months to six-months to three-months in Germany, France and Italy. In Spain, the headline HICP rises by 1% over 12 months, the weakest of rise among the four largest economies; it gains at a 0.2% annual rate over six months, tied for the low pace on that horizon. Spanish inflation accelerates to an annual rate of 0.5% over three months, the largest gain over three months among the Big Four economics. Still, Spain’s inflation and path remains low and its ‘acceleration’ quite modest.

Core or ex-energy inflation: Among the four largest economies, the core (or ex-energy) inflation rate remains tempered but shows some upward pressure over three months compared to six months in each of these member states. For Germany, the ex-energy pace is stuck right at or just below a pace of 1.5%. In France, ex-energy inflation is at its strongest over 12 months at a pace of 1.2%; then it settles into an annual rate gain of 0.5% and 0.6% over six months and three months, respectively. That’s the smallest uptick in inflation possible. In Italy, core inflation rises by 0.6% over 12 months; it is dead flat at zero over six months, then turns up to log a 0.4% annual rate gain over three months. Only Spain shows steady – yet very minor- inflation acceleration with the core rate rising from 0.6% over 12 months to 0.7% over six months to 0.8% over three months. Spain and Germany show slightly higher three-month gains than 12-month gains while Italy and France show the opposite trend.

Year-on-year trends

The chart shows that year-on-year inflation has made two ‘assaults’ on the 2% pace since 2016. One failed immediately and in the most recent period inflation did manage to surpass 2% for a few months but then also collapsed below the 2% mark eroding to where we find it ‘today.’ This month, after an ongoing deceleration, year-over-year trends are starting to flatten out at current levels.

Impact on policy

The ECB itself has reversed course and started to see more downside price risk. Globally, central banks are cutting their growth forecasts as oil prices have struggled to hold steady. The weaker economic environment is a big part of the new concern about price stability that we have heard from the ECB and in Japan and is a reason why the U.S. has gone to a neutral policy, abandoning its former policy of relentless quarterly rate hikes. But where policy goes next is still a matter for debate. Some say the next move in the U.S. will be to stimulus while others see the Fed on an extended pause, but hiking rates later in the year. Arguably, the ECB made a move it hopes will be short lived since it has set its new round of lending to start in September- hardly an ‘of the moment’ act of stimulus. Central bankers are still playing their cautious not-so-sure-what-to-do game which is all the more dangerous because its very hesitancy delivers less stimulus in the event that stimulus is really needed.

Data trend update…still weakening...downside risk

Economic reports in the U.S. today include a national production index for February which showed a manufacturing IP contraction and a regional manufacturing report from the NY Federal Reserve district bank that ebbed and has lingered below its median reading signaling weakness. In Japan recent orders weakness and in Europe a number of weak industrial reports underpin the notion of global slowing. But it is not just output weakness, but also demand weakness has cropped up. European vehicle registrations decreased for the sixth month running. Dutch retail sales hit a 10-month low in their growth pace. All of this has given rise to anxiety among policy makers. Among other eco-signals today, Indonesian exports fell more than expected as world trade concerns are well in play. News reports that the U.S. and China are not on the verge of having their leaders meet soon as we once thought. In Canada, home sales fell. In China, officials said today that monetary policy still has steps it can take to promote growth. The rhetoric from the central bankers points clearly where they think the risks now lie and that is still to the downside even as they take steps and also prevaricate.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief