Global| Dec 15 2020

Global| Dec 15 2020EMU Inflation Remains Subdued and Well Below Limit; So What Is and Where Is the Risk?

Summary

EMU inflation trends The chart gives the big picture overview of trend based on year-on-year calculation conducted on headline inflation. On that basis, inflation has been well under-wraps. The ECB has not met or exceeded its [...]

EMU inflation trends

EMU inflation trends

The chart gives the big picture overview of trend based on year-on-year calculation conducted on headline inflation. On that basis, inflation has been well under-wraps. The ECB has not met or exceeded its inflation ceiling recently. The last excess was minor and short-lived in 2018. There was a one month ‘excess' in early-2017 when the HICP hit 2% year-on year. Then, there was another long stretch back 2013 without any ceiling excess. Clearly there has been undershooting much more than there has been overshooting.

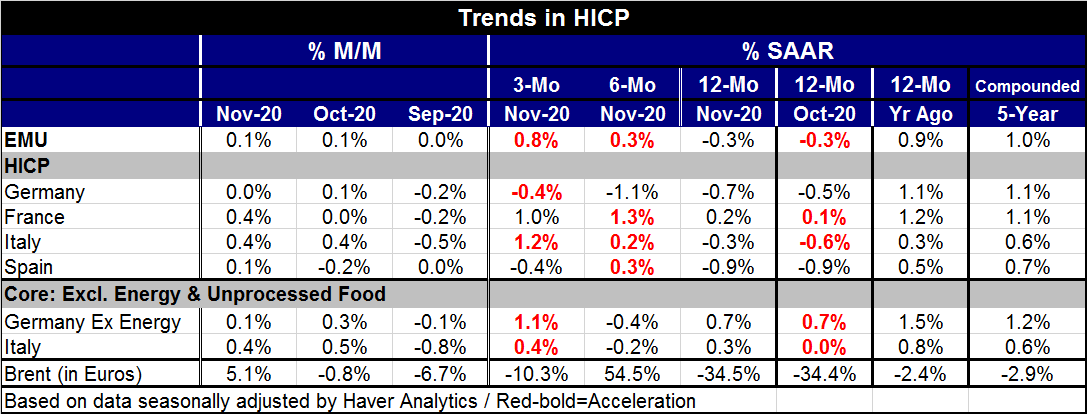

Inflation is whipped and beaten...

The table show some year-on-year results and one column of five-year calculations, the three recent months changes by country as well as sequential trends for each country and a core series for Italy and an ex-energy series for Germany. Inflation is contained on all of these approaches in all countries (the four largest EMU members) and that is an impressive result. Over three months, the highest inflation is an annualized gain of 1.2% in Italy followed by a 1% pace in France but accompanied by a decline at a 0.4% annual rate in Germany and in Spain. Over six months, the largest gain is a 1.3% rate of increase in France against a 0.3% pace in Spain, a 0.2% pace in Italy and prices falling at a 1.1% pace in Germany. Over 12 months prices are falling in all four countries. The ex-energy gain in Germany over 12 months is 0.7%; the core gain in Italy over 12 months is 0.3%. The year-on-year pace in November is lower everywhere compared to its pace one year ago in November of 2019.

Risk...where's the risk?

Think about inflation risk in this sort of environment... OK, that's long enough. The table shows the compounded results for the November HICP index relative its value of five years ago. For all of the EMU, the compounded annual gain has been 1% over five years. For Germany and France, it has been a 1.1%. For Spain, it has been 0.7%. For Italy, it has been 0.6%. Italy's inflation has averaged just a tic more than one half of one percentage point a year for the last five years! Judging from the last five years the environment, this has been a period of price stability and, beyond that, of inflation weakness. Currently global growth is being held back by the virus and by attempts to contain the virus –and that includes a depressing impact on oil prices. There is considerable slack globally and only China is showing signs of breaking out into a clear path of growth while everyone else struggles.

The ECB

At the European Central Bank, Christine Lagarde talks of doing whatever she can to sustain growth, a far cry from Mario Draghi's much more desperate ‘whatever it takes.' Policy has already been stretched and the Lagarde comment simply reflects the reality of central bankers having gotten to the bottom of their toolbox. There is ‘always something' a central bank can do; central banks themselves are coming to realize that going overboard may not only be risky for the longer term, but it isn't always helpful even in the short run.

Central bankers; different strokes for different folks

We can look at what central banks have done in these times and at how they have approached matters. The ECB is ‘ready to do more' to boost growth, but it may not be sure that it has the proper tools to do so. But the rhetoric is that of being helpful to boost growth. This significant for a central bank with only an inflation ceiling, and no responsibility (well, no formal responsibility…) to maintain growth. From the ECB there is very little angst displayed about missing its ‘target' on the low side so persistently in recent years. Contrarily in Japan there is a good deal of consternation about the bank having missed its 2% objective repeatedly. The Bank of Japan sees that as a challenge to its credibility. The ECB does not. In the ECB, the hard money countries look at the ‘just less than 2%' objective as a ceiling while other members see it as a target. Hard money ECB members are still wary of the impact of negative rates. They are much more worried about the market structure of interest rates and stimulus created by the central bank than they are mollified by its recent performance. In Japan, it is all about performance. In the U.S., the Fed has gone flexible on us. It has bemoaned its past target misses and admitted that it was too tight. It now treats the economic environment as needy in a different way and has pledged to support growth since it says that it sees no inflation risk.

Both Japan and EMU are truer to their objectives (although neither is any closer to a solution than the Fed) while the Fed plays the dangerous game of handicapping the environment and assuming where the risk is rather than committing to its policy objectives fully and equally. The Fed is now in the business of picking favorites and it has chosen to support growth. This is dangerous because over the previous eight years the Fed chose the other risk and was persistently wrong and was never willing to stand back and reassess its own errors. Will it make ‘the same sort of' mistake again?

Where IS the risk anyway?

There is at this time some analysis that I disagree with about the Fed and where the risks lie, although the argument applies globally to central banks generally and not just to the Fed. The argument is that with a vaccine circulating and beginning to work its ‘magic' the Fed and other central banks may soon find themselves in a conundrum with a policy geared to stimulus and an economy that will be free to grow faster. The implication is that the Fed may be too easy and could be caught out and need to move faster to contain things (on the upside). For now the Fed does not see rate hikes anywhere ‘on the horizon.' Still, the notion of the Fed being caught out with too much stimulus seems obvious since that is the way that the Fed is leaning and the vaccine should help to bring damaged parts of the economy back on line. On the face of it, that seems to conjure one-sided risk. If that view is right, the Fed could be forced unexpectedly –and quite contrary to its guidance- to flip policy. However, I think that is unlikely.

The future is also about the past...

What is missed by those looking for a stabilizing and growth promoting impact from the oncoming vaccines is that the vaccines will have their impact work though slowly and methodically. People will only gradually come to see the economy as safer than it has been and become willing to do things that now are either prohibited or that are not prohibited but still not widely embraced. But even more important is the legacy of damage from the virus. Some businesses have literally been destroyed. They are not coming back. They will not be employing anyone when the vaccine is implemented fully. There are households that are not getting by now that will be at risk when the eviction moratorium ends in the U.S. This is a special problem for the U.S. Right now that moratorium ends at the end of December. CDC will probably extend it. No matter. At some point, it will end and like in a game of musical chairs when the music stops, some will be positioned to succeed and some will be caught out. Will people have gotten their old jobs back or new ones? What of the accumulated rent or mortgage payment arrearages? For renters who could barely survive before, how will they make-up for past missed payments? How will they avoid future eviction with a heavier load of responsibility from the past?

Momentum is no longer in your favor

The economy in the U.S. is slowing down. Germany and the Netherlands have new movement restrictions in place. Sweden's emergency rooms are nearly full; it is asking for help as it is being castigated for not protecting the elderly as it went about in search of herd immunity (more here). Just under half of Sweden's death toll has been of nursing home residents. Europe and the U.S. are facing coronavirus outbreak problems as the vaccines begin to come on stream. It is hard to handicap how those two opposing forces will play out since the infection spread is getting worse just as the saving vaccine is being distributed and the global economy is clearly slowing. And in the case of the U.S., it has only arranged for 100mln doses, enough to vaccinate 50mln of its 330mln people.

Problems are a function of policy not the virus - policymakers ARE responsible

It is important to recognize as we look ahead and try to handicap macroeconomic policy the extent to which various government policies are holding things together. Still, an unprecedented number of people have lost their jobs and remain unemployed in the wake of policies taken by the health authorities to stop contagion. For many people, their jobs and their places of employment are shuttered for good. It is wrong to say that the virus did this. Our own policies have done this. And once we admit that we are part way to admitting our own culpability in the plight of others.

People should not lose their jobs, all their savings and their homes because the CDC shut their business and would not let them work or because some governor did that. People were largely not given a choice. Rules were set by authorities and enforced. Some of us were adversely affected. Some were not. And there seems to be little effort to drill down and find out who is falling between the cracks of the naively concocted support programs to help them. Moreover, keeping a person from being evicted, as is being done in the U.S., but continuing to tally up his or her past due rent is not really making them whole. It is giving them a whole bunch to worry about when the rules change back.

The fallout from the virus is going to last far longer than what people realize. Behavior is changing. There will be lingering fears. The service sector, especially hospitality businesses, has been eviscerated. And in the U.S., al this happens at a time of extreme political division in the population. While everyone is anxious for 2020 to end, I must say that I still do not look forward to the challenges of 2021. They will be different. But 2021 will not be an easy year.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief