Global| Jul 17 2020

Global| Jul 17 2020EMU Inflation Remains Moderate and Growth Undernourished; Can the EU Agree to a Stimulus Deal?

Summary

EMU inflation is weak. Inflation trends are weak and over the past 5 years inflation has been consistently below its targeted pace. That explains why the ECB has engaged in all sorts of policies to try to revive growth and is still [...]

EMU inflation is weak. Inflation trends are weak and over the past 5 years inflation has been consistently below its targeted pace. That explains why the ECB has engaged in all sorts of policies to try to revive growth and is still running a policy of negative interest rates. Another reason is the lack of a coordinated fiscal effort in the EMU and the fact that many needy members are flush up against the constraint imposed by the Union’s Maastricht fiscal rules.

EMU inflation is weak. Inflation trends are weak and over the past 5 years inflation has been consistently below its targeted pace. That explains why the ECB has engaged in all sorts of policies to try to revive growth and is still running a policy of negative interest rates. Another reason is the lack of a coordinated fiscal effort in the EMU and the fact that many needy members are flush up against the constraint imposed by the Union’s Maastricht fiscal rules.

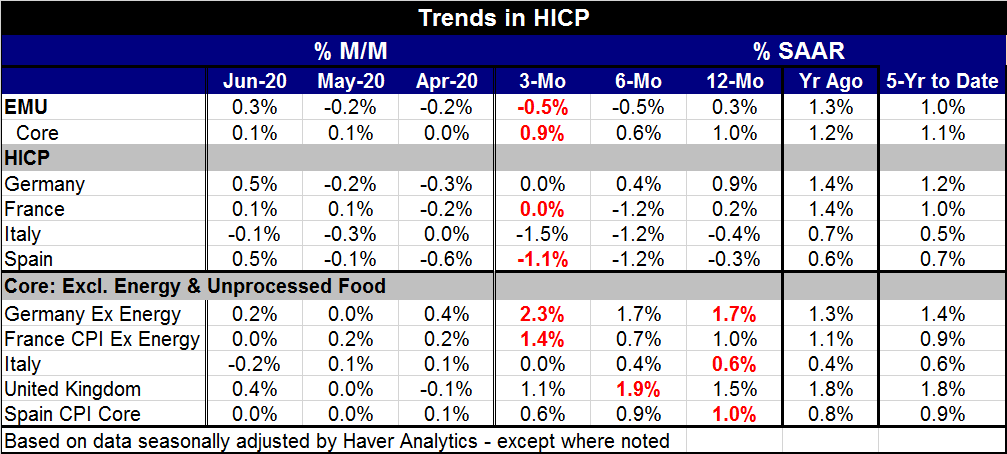

None of the four largest EMU economies show any hint of inflation accelerating. Inflation performance is and has been weak; Germany has headline inflation up by 1% over 12 months but running at a pace of zero over three months. Prices in Italy and Spain are falling over 12 months, six months and three months.

The situation for core inflation is a bit stickier, but still there is persistent undershooting and core or ‘ex-energy’ inflation is very much under control. EMU-wide core inflation is at 1% and the core is up at a 0.9% annual rate over three months. German ex-energy inflation is at 1.7% over 12 months and six months and is up at a 2.3% pace over three months. Germany is still a very low unemployment country in the EMU. French core inflation shows some heating up over three months as well with the pace at 1.4%. Still, the 12-month core rate for France and Spain is at 1%; for Italy it is at 0.6%. The Italian core trend is withering as is Spain’s.

Few are worrying about inflation now although the usual hard money EMU members are eager to get rates up to more normal level for a variety of reasons. They are sure that rates that low will eventually come to no good.

However, growth is still weak across the EMU with the ECB Survey of Professional Forecasters (SPF) underlining that today. The survey shows the expectation that EMU GDP will drop by 8.3% this year – a deeper hole than the -5.5% rate that group saw earlier in the year. In compensation, 2021 growth is seen a bit stronger at 5.7%, up from 4.3% previously. The inflation outlook for 2020 remains at 0.4%, another year of undershooting for the ECB. And for the year-ahead an inflation rate of 1% is expected, yet another year of undershooting.

All of this of course depends on handicapping the virus which no one can do but we all guess at. Opening and closing the economy based on infection status takes a toll on the economy and potentially a very large toll on the most fringe participants. The peak rate of unemployment is now pushed back by these forecasters to 2021, underscoring the ongoing economic weakness and the sluggish nature of the current economy.

EU members are currently meeting to decide on a stimulus effort and program. The negotiations have been protracted and contentious as the countries of the South argue for grants. And so far, the countries of the North that stand to do the lending have resisted. French President Emmanuel Macron and German Chancellor Angela Merkel want grants to mostly finance the fund. Four northern nations insist on loans. Over this same period, the U.S. has launched a number of support programs and in June U.S. retail sales already are rising over 12 months. The U.S. is currently giving consideration to a second round of stimulus while Europe ponders its first. Emmanuel Macron has said it is a "moment of truth" for Europe. Angela Merkel has said that the differences on the issue are very big. Dutch Prime Minister Mark Rutte, whose country is part of the so-called "Frugal Four" northern states, said he "put the chances of getting a deal this weekend at less than 50%." We shall see.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief