Global| Jan 06 2009

Global| Jan 06 2009EMU Inflation: Now You See It; Now You Don't!

Summary

The EMU inflation rate fell sharply in December more sharply than have been expected. Headline inflation –the measure that the ECB sets a ceiling for -- is now below that ceiling of 2% at a Yr/Yr rate of 1.6%. A Yr/Yr rise of 1.8% had [...]

The EMU inflation rate fell sharply in December more sharply

than have been expected. Headline inflation –the measure that the ECB

sets a ceiling for -- is now below that ceiling of 2% at a Yr/Yr rate

of 1.6%. A Yr/Yr rise of 1.8% had been expected. Core (ex food and

energy inflation) has long been on a milder path than that of headline

inflation. But the ECB sets a ceiling for the headline alone. Still,

the headline pace is now more in line with the core where the pace

Yr/Yr is 2.2% (lagged by one month since the December Core is not yet

available- so the real up-to-date core rate is probably even lower).

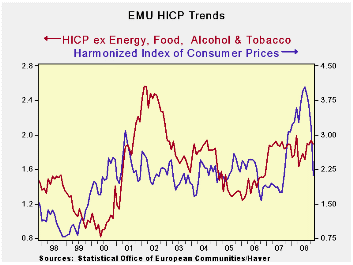

Core inflation, even through November, shows the six- and three-month

rates of inflation are dropping fast. That is true for headline

inflation as well, as the chart above amply demonstrates.

In short, the ECB now has a set of consistent signals about

inflation. Inflation is now inside its preferred boundaries and

falling. It faces an inflation pace that is well below its ceiling. It

faces a weakening economy. Clearly this inflation result allows for the

ECB policy to be much bolder and for its rhetoric to be much less

circumspect. Even stodgy old central bankers should see the message

clear and strong as indicating that economic weakness is more

pronounced than expected, pushing down prices and not just allowing,

but calling for more aggressive fiscal and monetary policy actions. The

euro weakened in the wake of this report on precisely those sorts of

conclusions by market participants.

| Trends in EMU HICP; Flash Index | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Dec-08 | Nov-08 | Oct-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | -0.3% | -0.3% | 0.0% | -2.5% | -0.9% | 1.6% | 3.1% |

| Core | #N/A | 0.1% | 0.2% | 1.6% | 2.0% | 2.2% | 2.3% |

| Goods | #N/A | -0.8% | 0.0% | 0.1% | -1.7% | 1.8% | 3.4% |

| Services | #N/A | -0.1% | 0.1% | -2.7% | 1.5% | 2.6% | 2.5% |

| HICP | |||||||

| Germany | -0.5% | -0.1% | -0.3% | -3.3% | -0.9% | 1.1% | 3.1% |

| France | #N/A | -0.4% | 0.1% | -1.4% | 0.0% | 1.9% | 2.6% |

| Italy | -0.1% | -0.5% | 0.3% | -1.1% | 0.0% | 2.3% | 2.8% |

| Spain | #N/A | -0.4% | -0.3% | -2.4% | 0.5% | 2.4% | 4.1% |

| Core:xFE&A | |||||||

| Germany | #N/A | 0.1% | -0.1% | 0.0% | 1.3% | 1.3% | 2.4% |

| Italy | #N/A | 0.0% | 0.5% | 1.9% | 2.7% | 2.8% | 2.2% |

| UK | #N/A | 0.2% | 0.0% | 0.8% | 2.3% | 2.5% | 1.8% |

| Spain | #N/A | 0.1% | 0.1% | 1.5% | 2.6% | 2.7% | 3.3% |

| Blue shaded area data trail by one month | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief