Global| Jun 17 2015

Global| Jun 17 2015EMU Inflation Makes First Rise in Six Months; Divergence Is Still an Issue

Summary

EMU inflation has a year-over-year gain for the first time in six months. With the effect of falling oil out of the way, inflation is again headed higher. But what will that mean for the euro area? One thing history and the financial [...]

EMU inflation has a year-over-year gain for the first time in six months. With the effect of falling oil out of the way, inflation is again headed higher. But what will that mean for the euro area? One thing history and the financial crisis has taught us is that you learn next to nothing about inflation in the euro area by looking at the region's overall rate. Inflation diverge has been the important driving force of this financial crisis. Trying to get the price levels back into reasonable alignment is harder than putting toothpaste back into the tube.

EMU inflation has a year-over-year gain for the first time in six months. With the effect of falling oil out of the way, inflation is again headed higher. But what will that mean for the euro area? One thing history and the financial crisis has taught us is that you learn next to nothing about inflation in the euro area by looking at the region's overall rate. Inflation diverge has been the important driving force of this financial crisis. Trying to get the price levels back into reasonable alignment is harder than putting toothpaste back into the tube.

In most modern economies, there is one-way price flexibility. Prices move up much more easily and with less duress than they move down. When prices have to move down by a significant amount for a significant period of time, great turmoil is created. And this is the nature of the European crisis and of Greece in particular.

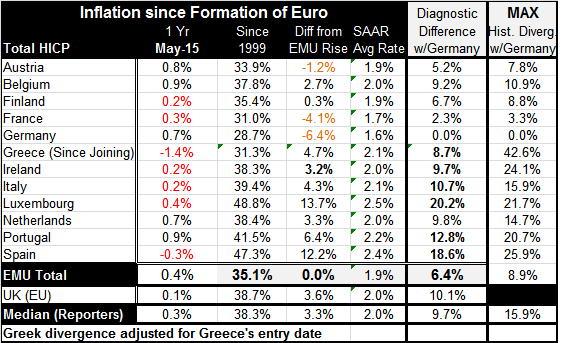

The table shows what inflation has done in the original EMU member countries and in Greece since the EMU was formed. The column `Diff from EMU Rise' is instructive as it shows that only THREE of 12 countries have run an inflation rate below the (weighted) average for the EMU as whole. This is because the low inflation countries tend to the large countries. A second consequence is that peripheral countries can run higher inflation rates without much consequence for the region's overall inflation performance. And that is not a good thing. It means that the EMU can be laboring under the illusion that inflation in the euro area is just fine while some members can have developed serious inflation problems. And this is exactly what happened in the run up to the EMU crisis.

The second column to the right shows each country's divergence with Germany, the region's persistent low inflation country. The far right column shows the maximum historic difference between Germany's price level and each member's price level. At one point, Greece had let its price level rise over 40% above that of Germany. In contrast, austerity has brought that divergence down to 8.7% from over 40%. Greece has come a long way in a short period of time but not without a lot of pain. The key question is whether Greece is prepared to continue this progress or at least to maintain it.

Indeed, price level divergence now is worse than in Greece in Luxembourg (a financial center), Spain, Portugal and Italy. But Luxembourg is a special case as a financial center and the other countries have not seen the divergence Greece did that ravaged its economy. Turning to the far left column of data, we see the most recent year-over-year inflation performance. Seven countries are running lower inflation rates than Germany over the past year. That is unusual.

Inflation differential data show us that Spain and Greece are still making strong inflation progress. Portugal, however, is not. As the euro area begins to flirt with leaving the crises behind, as it will when Greece's situation is sorted out, we will again look to see if inflation divergence is going to be a problem. Even the quickest peak at the table suggests it will be.

In the period of financial distress, the ECB obtained tools to help out some member countries more than others through targeted bond purchases. But there has been no change in monetary policy to allow monetary policy to be stricter in any region compared to any other. Thus, as the EMU progresses to a better growth phase, there is no mechanism to control inflation differences at the local level. The only tool for regional application in the EU is the budget deficit and debt criteria. And these tools have proved difficult to wield in Europe. Inflation divergence has begun to grow again; as Europe recovers, this will be the biggest problem for it to gain control of in order to assure future stability.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.