Global| Jan 15 2014

Global| Jan 15 2014EMU Inflation Hugs the Lower Bound

Summary

European Monetary Union inflation rose by 0.1% in December after rising at the same pace in November. In October inflation fell by 0.2%. Inflation in the euro zone is both subdued and decelerating. This early in the process we don't [...]

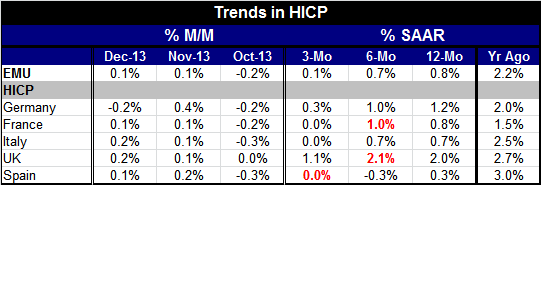

European Monetary Union inflation rose by 0.1% in December after rising at the same pace in November. In October inflation fell by 0.2%. Inflation in the euro zone is both subdued and decelerating. This early in the process we don't have updates on core inflation as the ex-food and energy measures are not yet prepared. Evidence suggests that core inflation has a bit more life than headline inflation which is been dominated by ongoing weakness in the oil patch. Nonetheless, this decelerating inflation trend is widespread in the euro zone. The zone itself shows inflation a year ago was running at a 2.2% annual rate pace over the last 12 months; that is down to 0.8% over six months; the pace is down further to 0.7%; over three months the pace is down again to a 0.1% annual rate. Inflation in the euro zone is at a crawl.

European Monetary Union inflation rose by 0.1% in December after rising at the same pace in November. In October inflation fell by 0.2%. Inflation in the euro zone is both subdued and decelerating. This early in the process we don't have updates on core inflation as the ex-food and energy measures are not yet prepared. Evidence suggests that core inflation has a bit more life than headline inflation which is been dominated by ongoing weakness in the oil patch. Nonetheless, this decelerating inflation trend is widespread in the euro zone. The zone itself shows inflation a year ago was running at a 2.2% annual rate pace over the last 12 months; that is down to 0.8% over six months; the pace is down further to 0.7%; over three months the pace is down again to a 0.1% annual rate. Inflation in the euro zone is at a crawl.

Such low-inflation does not necessarily indicate that the euro zone is headed for deflation. On the other hand, there is nothing about this decelerating inflation rate that is reassuring. Inflation is low and falling, well below the European Central Bank's goal for price stability.

Europe has a number of countries that are experiencing flat or declining population growth. It also has a number of countries struggling under austerity programs that have held back growth. Recently manufacturing sectors have been showing signs of a breakout. Services sectors have been improving but not that strongly. EMU-wide unemployment is still at a record high.

These are not exactly the characteristics of the country that we expect to be fighting off deflation. However, the very weak price action is strongly suggestive of still weak domestic demand. High unemployment is an undeniable indicator of under-performance.

On the credit side of things money supply growth had been accelerating for over a year while at the same time credit growth had been contracting. Over the past three months money growth has turned around and started to post lower growth rates while credit growth has continued to decline. While ECB President Mario Draghi has promised strong efforts to keep the euro zone on a growth path, he has limited tools and less than full member support.

Recent EMU data show that export growth is falling off. At the same time Germany continues to show very strong trade figures. The German trade surplus has surpassed the surplus of China. German officials are defending German policies and arguing that they will not be changed. However, at a time for the world economy when domestic demand is so hard to come-by, record German trade performance suggests that Germany is gobbling up more than its fair share of domestic demand around the world.

The euro zone still is united mainly through a series of trade rules that encompass the members of the European Union, the monetary policy that applies to the members of the European Monetary Union, an emergency bank bail-out plan and the mixed wills of the member nations and their people. What is missing from this list is any sort of cohesive fiscal arrangement. After all, the monetary union has been enough influence to force troubled countries in need of financial assistance to engage in draconian domestic fiscal arrangements. That has had devastating effects on growth and unemployment and welfare in several countries of the monetary union. This is a one-sided game.

Today the World Bank, while lifting slightly its estimates for growth for the world economy, bemoans the loss of stimulus in the US economy. There have been several of these very slight almost technical upward adjustments in the outlook for growth for 2014. While anyone with economic data and the ability to draw graphs can see that downward trends have largely stopped and upward trends have taken their place, the economic underpinnings of these trends are far more fragile than simple charting reveals. Europe continues to have deep-seated divisions that may yet create problems for its incipient rise. The Germany's trade affluence dominates Europe; it has not resulted in that much faster growth at home for Germany and German growth in 2013 has been set back a bit overall. Germany after all is an export-led growth economy.

Germany is the strong-man economy of Europe. That does not necessarily mean that it will have the highest growth rate. It is simply a juggernaut that continues to push ahead at its own plodding pace stuck in first or second gear under almost any circumstance. The fact that it is an export-led growth economy means that it does not spin off a lot of externalities to boost its fellow EMU members. Instead, it parasitically thrives on the revival of growth that fellow members generate.

The EMU members have yet to make peace with the German model. Germany does not embrace it's generally faster growing brethren in the euro zone with their greater dependence on debt. Germany is still a highly conservative economy in the way it's run. And it is still looking for a way to operate in the EMU with interdependence while maintaining its independence and keeping insulation from what it views as the wilder policy tilt of its fellow EMU members. Germany has hoped to use deficit rules like a Japanese lunchbox to force fellow EMU members to mind their P's and Q's but as yet there is no overarching plan that all members agree to. Europe continues to be at risk for growth and continues to minimize the conflict among its members rather than to try to resolve differences.

The very weak inflation in the monetary union suggests more strongly that the problems in Europe will become confrontational rather than that they will be eased by the lubrication of rising inflation and increasing growth. When inflation is so weak, it hampers government finances and keeps financial pressures intense since many consumer obligations are of a nominal nature and are improved somewhat when there is at least some inflation.

We can see that inflation is low and decelerating in Germany, France, Italy, the UK and Spain. These are the largest countries in the euro zone. The UK is the largest country in the European Union that is not under the yoke of the common monetary policy. While the head of the ECB tries to engage in policies that are expansive and pro-growth, we see instead that inflation is already well below ECB guidelines and moving lower. This environment is not the result of an overzealous central bank. It is the result of weak economic conditions. Europe still has a long way to go.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.