Global| Jun 30 2008

Global| Jun 30 2008EMU Inflation Goes Ballistic - Over 4%; Ceiling Still is 2%

Summary

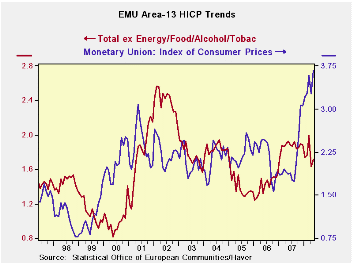

The EMU HICP is now over 4% Yr/Yr. this is not a good result for a central bank that has set a ceiling of 2% for headline inflation. It is also running at a pace of just over 4% over three-months and six-months. No detail of prices is [...]

The EMU HICP is now over 4% Yr/Yr. this is not a good result

for a central bank that has set a ceiling of 2% for headline inflation.

It is also running at a pace of just over 4% over three-months and

six-months. No detail of prices is yet available and only Germany and

Italy have released public figures for June. The good news is that

neither Italy nor Germany show accelerating trends in headline

inflation. Their sequential growth rates are either mixed or pointing

lower. But at 4% Yr/Yr Italian inflation is high and a 3.6% Yr/Yr

German inflation, usually one of the lowest in the zone, is also high.

The ECB has an emerging credibility problem that will probably

force its hand on a rate hike. But one as to wonder the usefulness of a

target that is breached so baldy it has been doubled. While critics can

pick at the Fed’s choice of the core rate to ‘monitor’ it has set out

parameters for that rate’s range that US inflation still lies within.

The core is contained even as headline inflation in the US surges over

4%. The Fed can claim victory but many don’t want to acknowledge it.

Europe has a policy credibility issue inflation has been above

the ECB’s ceiling for far too along. In the US inflation is within the

Fed’s boundaries but it is the Fed choice of boundaries that is a

matter of debate concerning policy integrity. Central banks are having

all sorts of issues maintaining their standing despite the success in

holding core inflation low.

Still the fact is…

When oil prices flare so sharply, it is impossible to cushion the

impact on inflation in the short run. The ECB thus has a credibility

problem since its sole pledge is on headline inflation. It has not

offered any cogent statement on inflation or an alternative to headline

and has not suggested anything other than that inflation as it is

remains unacceptable. Energy inflation is something special, since if

the central bank can hold its impact on core inflation at bay it will

also produce deflationary effects. No central banks gets good marks for

their public relations stance in dealing with this issue in this cycle

despite having had prior experience with energy inflation.

| Trends in EMU HICP; Flash Index | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % SAAR | ||||||

| Jun-08 | May-08 | Apr-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | 0.5% | 0.6% | 0.0% | 4.3% | 4.2% | 4.0% | 1.9% |

| Core | #N/A | 0.2% | -0.1% | 2.3% | 2.5% | 2.4% | 1.9% |

| Goods | #N/A | 0.8% | 0.6% | 11.8% | 5.3% | 4.5% | 1.4% |

| Services | #N/A | 0.4% | -0.1% | 2.6% | 3.7% | 2.5% | 2.6% |

| HICP | |||||||

| Germany | 0.5% | 0.6% | -0.4% | 2.7% | 3.2% | 3.4% | 2.0% |

| France | #N/A | 0.5% | 0.1% | 4.6% | 3.8% | 3.7% | 1.1% |

| Italy | 0.6% | 0.4% | 0.0% | 4.2% | 4.6% | 4.0% | 1.9% |

| Spain | #N/A | 0.7% | -0.1% | 4.1% | 4.3% | 4.7% | 2.4% |

| Core excl Food Energy & Alcohol | |||||||

| Germany | #N/A | 0.3% | -0.5% | 0.8% | 1.2% | 1.8% | 2.1% |

| France | #N/A | 0.1% | 0.1% | 2.4% | 2.6% | 2.4% | 1.4% |

| Italy | #N/A | 0.2% | -0.1% | 3.1% | 2.9% | 2.7% | 1.9% |

| Spain | #N/A | 0.3% | -0.1% | 2.2% | 2.7% | 3.3% | 2.5% |

| Blue shaded area data trail by one month | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief