Global| Oct 03 2019

Global| Oct 03 2019EMU: Inflation, Domestic Spending and Global Conditions

Summary

The good news - and there has not been enough of that these days - is that in EMU consumer spending trends are holding up nicely. Spending trends are generally neither accelerating steadily nor decelerating steadily in the EMU. But [...]

The good news - and there has not been enough of that these days - is that in EMU consumer spending trends are holding up nicely. Spending trends are generally neither accelerating steadily nor decelerating steadily in the EMU. But there is actually more of a tendency to accelerate as the three-month growth rates are above the 12-month pace, showing some spunk in the underlying trends. However, a weakening in trends over six months keeps this from being a true sequential acceleration. The adverse trend is that for the EMU and several select European economies, the growth in sales for the quarter-to-date has begun to falter despite those other generally favorable trends.

The good news - and there has not been enough of that these days - is that in EMU consumer spending trends are holding up nicely. Spending trends are generally neither accelerating steadily nor decelerating steadily in the EMU. But there is actually more of a tendency to accelerate as the three-month growth rates are above the 12-month pace, showing some spunk in the underlying trends. However, a weakening in trends over six months keeps this from being a true sequential acceleration. The adverse trend is that for the EMU and several select European economies, the growth in sales for the quarter-to-date has begun to falter despite those other generally favorable trends.

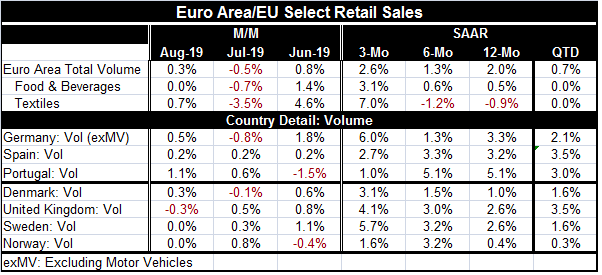

Germany, Spain and Portugal have impressive year-over-year growth rates for sales that generally hold up over three months as well. Their quarter-to-date (QTD) growth is in the 2.1% (Germany) to 3.5% (Spain) range for sales volumes. Those are good numbers. But for the EMU as a whole, the QTD growth is a weak 0.7%. For the United Kingdom, Denmark, Sweden and Norway, there is some sales acceleration in play and all have ‘acceptable’ three-month sales volume growth, but on a QTD bases there is sales weakness; the sales pace ranges from 3.5% in the U.K. to 0.3% in Norway. While the U.K. sales are impressive, the U.K. today reported out a service PMI reading below 50 that will raise new questions about growth and about the sustainability of sales moving ahead. Also Britain seems to have made no progress toward an acceptable Brexit plan despite all sorts of scheming by Boris Johnson.

Meanwhile inflation pressures tank

Meanwhile inflation pressures tank

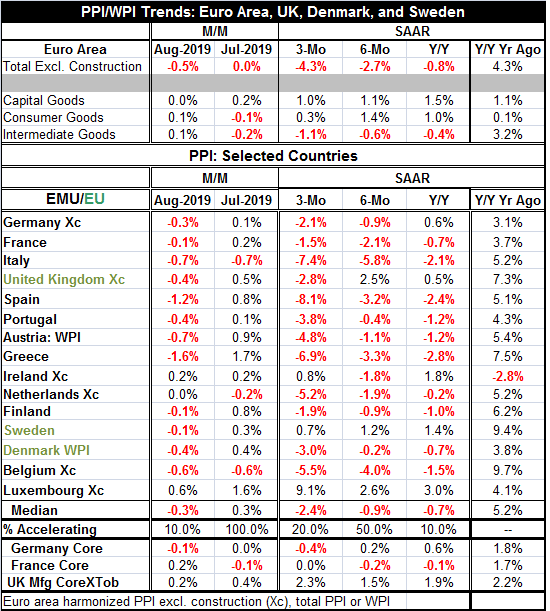

The EMU PPI data, fresh off the press, show more weak inflation trends. With so many weak economic signals having weak prices as well is quite unsettling as it makes economists fear the worst. That is why the firm retail sales data are so important and why consumer spending been so encouraging. Consumers have been able to hold the line on spending as economic activity has ramped down. But output takes labor and the risk is the further economic weakness will show its hand in the labor market as well and that will affect incomes, wages and eventually spending. For now that cascade has not been triggered.

But the weak PPI is worrisome as far the ECB hitting its price marks eventually (the target is for the HICP not for the PPI). But PPI prices do matter and those price trends are slipping over 12 months, six months and three months, showing sequential deceleration as well as ongoing price declines. The good news is that the extreme price weakness is mostly lodged in intermediate goods and is a commodity and oil price feature. Sill, consumer prices are making weak gains over three months and are up by just 1% over 12 months. Capital goods prices are nearly unaffected but if you like to split hairs, capital goods prices also are decelerating sequentially but mildly. Only the U.K. shows some firmness in core pries which are weak in Germany and in France.

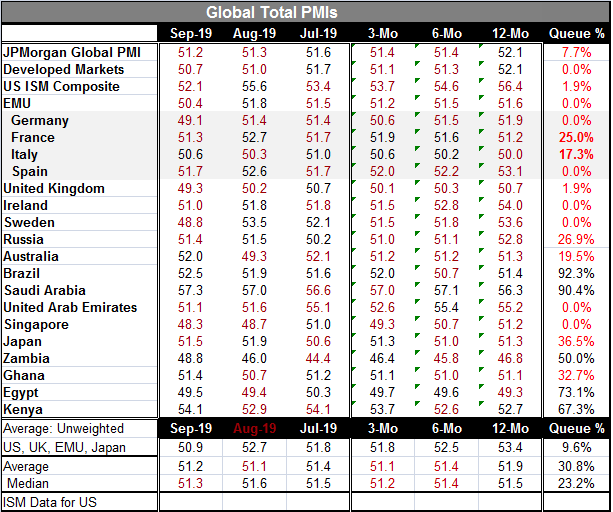

The table on Global Total or Composite PMIs shows some exceptional and widespread weakness. EMU growth is hanging on but just by a few threads as the EMU-wide composite PMI has a reading of just 50.4 in September. The EMU is on the precipice of private sector decline – not just Germany. The U.K. composite has slipped below 50 in September to join Germany. In all, six countries show PMI values below 50 in the table as of September - and these are for the composite PMIs - making that a much more worrisome result. The composite (unweighted) average has been low and has been slipping slowly. The JPMorgan Global PMI has been slipping as well and has a value of just 51.2 – it has been lower since January 2015 only 7.7% of the time. The developed economy metric is weaker and slipping faster.

The global picture darkens

Why do we study economics if we do the opposite?

If we look at policy responses, there is a lot to question. Why do we study economics if Japan with economic weakness and perpetual inflation target undershooting is going to take this moment to raise its consumption tax? Germany with private sector PMI below 50 and with EMU inflation chronically undershooting is engaged in a program of running fiscal surpluses. Italy, a country with low inflation, that austerity pummeled so hard that its real GDP is lower today than it was ten years ago is being prevented from using and fiscal stimulus. Meanwhile, the ECB barely got its stimulus plan approved and one of the German members on the executive board quit in protest. I guess in some places reality counts for nothing and ideology counts for everything.

A deteriorating environment

There can be little question but that the trade war is slowing things down everywhere. The most severe weakness is in manufacturing and it is being passed on to services. Getting a trade agreement would be a very good thing, but the U.S. is determined to get a good and enforceable deal. While China was once on the same page with the U.S., it appears that it no longer is. And many geopolitical events are mucking up the political atmosphere. Iran almost certainly was behind the Saudi oil-field attack. North Korea, poised for new talks, now has a missile it can launch from a submarine. Turkey is threatening over its border security and has hopped into bed with Russia by purchasing its weapons. China is facing severe dislocations in Hong Kong and trying to sort out what it can do. There are too many events of the edge to bet that they will all work out. Meanwhile, it is looking more and more like it is too late to avert a global recession. And central banks have little ammunition left to face a severe downturn when it comes. They still are trying to figure out what to do.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief